|

|

|

|

|||||

|

|

|

Footwear retailer Shoe Carnival (NASDAQ:SCVL) announced better-than-expected revenue in Q3 CY2025, but sales fell by 3.2% year on year to $297.2 million. The company expects the full year’s revenue to be around $1.14 billion, close to analysts’ estimates. Its GAAP profit of $0.53 per share was in line with analysts’ consensus estimates.

Is now the time to buy Shoe Carnival? Find out by accessing our full research report, it’s free for active Edge members.

“Third quarter results exceeded expectations. Shoe Station is winning - up over 5 percent in sales with 260 basis point margin expansion. We’re consolidating to one brand because the performance gap is undeniable. Over time, this unlocks $20 million in savings and $100 million in working capital to fund growth from our debt-free balance sheet,” said Mark Worden, President and Chief Executive Officer.

Known for its playful atmosphere that features carnival elements, Shoe Carnival (NASDAQ:SCVL) is a retailer that sells footwear from mainstream brands for the entire family.

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $1.14 billion in revenue over the past 12 months, Shoe Carnival is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Shoe Carnival’s 1.7% annualized revenue growth over the last six years (we compare to 2019 to normalize for COVID-19 impacts) was sluggish.

This quarter, Shoe Carnival’s revenue fell by 3.2% year on year to $297.2 million but beat Wall Street’s estimates by 0.7%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a slight deceleration versus the last six years. This projection is underwhelming and implies its products will face some demand challenges.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

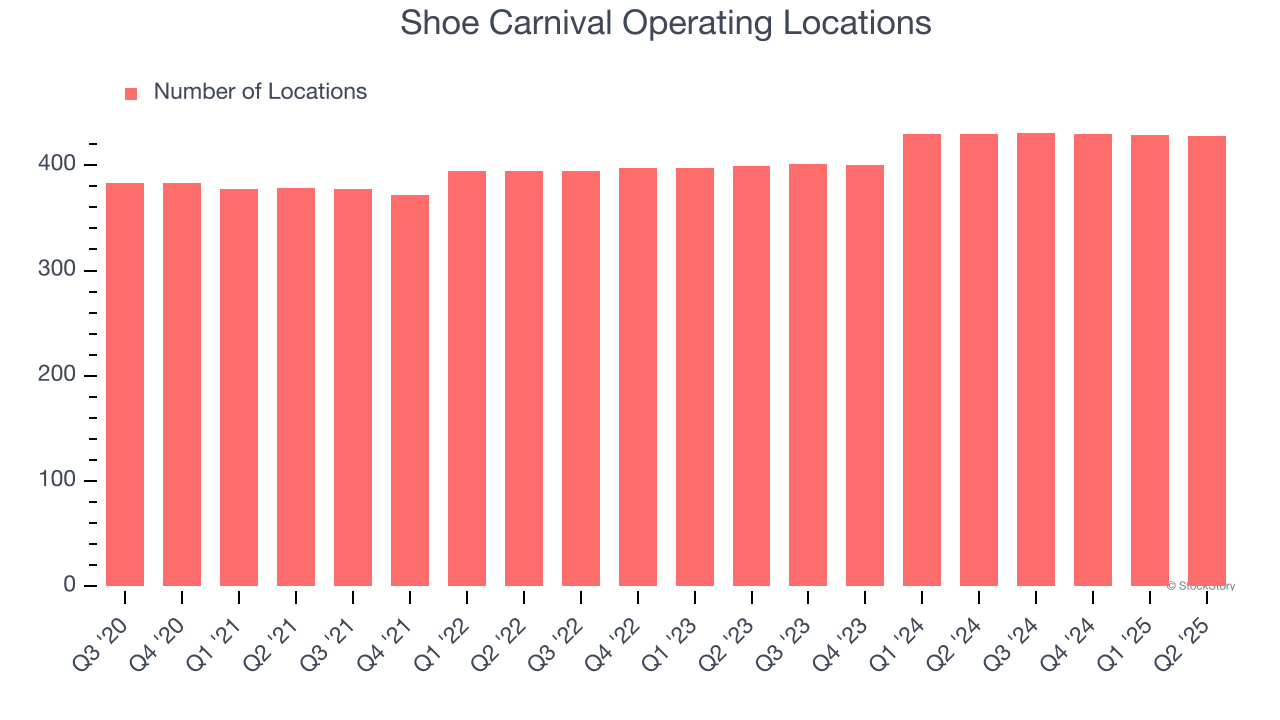

A retailer’s store count often determines how much revenue it can generate.

Over the last two years, Shoe Carnival opened new stores at a rapid clip by averaging 4.4% annual growth, among the fastest in the consumer retail sector. This gives it a chance to scale into a mid-sized business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Note that Shoe Carnival reports its store count intermittently, so some data points are missing in the chart below.

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Shoe Carnival’s demand has been shrinking over the last two years as its same-store sales have averaged 5.4% annual declines. This performance is concerning - it shows Shoe Carnival artificially boosts its revenue by building new stores. We’d like to see a company’s same-store sales rise before it takes on the costly, capital-intensive endeavor of expanding its store base.

In the latest quarter, Shoe Carnival’s same-store sales fell by 2.7% year on year. This decrease was an improvement from its historical levels. It’s always great to see a business’s demand trends improve.

We liked that Shoe Carnival exceeded analysts’ revenue expectations this quarter despite a decline in same-store sales. We were also glad its full-year EPS guidance trumped Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $16.69 immediately after reporting.

Is Shoe Carnival an attractive investment opportunity at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jun-11 | |

| Jun-11 | |

| Jun-11 | |

| Jun-02 | |

| May-26 |

Shoe Carnival ditches rebanner strategy

Retail Dive

|

| May-21 | |

| May-21 | |

| May-21 |

Shoe Carnival Shares Rise After Q1 Report

Footwear News

|

| May-21 | |

| May-21 |

Shoe Carnival: Fiscal Q1 Earnings Snapshot

Associated Press

|

| May-21 |

Shoe Carnival Reports First Quarter 2026 Results

Business Wire

|

| May-07 | |

| Mar-27 | |

| Mar-27 |

Shoe Carnival scales back rebrand

Retail Dive

|

| Mar-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite