|

|

|

|

|||||

|

|

|

Cimpress plc CMPR is poised to gain from solid momentum across its Vista, National Pen and Upload & Print segments. An increase in demand for product categories like promotional products, apparel and gifts, signage and packaging and labels is aiding the Vista segment. Growth across all major markets is also supporting the segment’s results. Lower advertising spends and increases in tariff-related pricing are driving the National Pen segment. In the same period, the Upload & Print segment’s revenues were supported by increasing order rates and new customer growth.

Cimpress’ scale allows small businesses to access high-quality products and printing services that may otherwise be out of reach. Its product portfolio has expanded to cover a wide range of marketing needs, while PrintBrothers’ businesses continue to adopt technologies from the company’s mass customization platform. Also, Cimpress is restructuring its operations by consolidating product development teams that were previously engaged in overlapping activities. These measures are expected to enhance customer value and drive long-term business efficiency.

The company’s emphasis on customer service, backed by efficient operations, strong supply-chain management and continuous product innovation, positions it well for growth. Despite cost inflation, pricing actions are expected to drive its performance in the quarters ahead. The company also targets to maintain crucial growth investments while working toward its net leverage target of 2.5x trailing-12-month EBITDA.

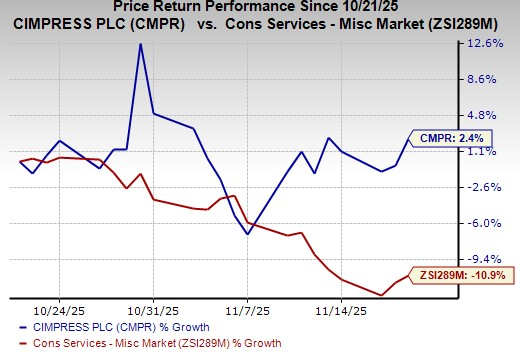

In the past month, this Zacks Rank #3 (Hold) company’s shares gained 2.4% against the industry’s 10.9% decline.

However, escalating costs and expenses have been a concern for CMPR over time. In the first three months of fiscal 2026 (ended September 2025), the cost of revenues increased 8.9% on a year-over-year basis due to increasing internal variable manufacturing and shipping costs. The metric, as a percentage of net revenues, increased 80 basis points to 53.3%. Also, general and administrative expenses rose 4% year over year in the same period due to higher long-term incentive compensation and cash compensation costs.

The company is persistently bearing the brunt of input cost inflation. In the first quarter of fiscal 2026, Cimpress’ gross profit margin decreased approximately 100 basis points to 48%. Escalation in costs, if not controlled, can severely affect margins and profitability in the quarters ahead.

Cimpress operates across diverse regions, which exposes it to certain political, environmental and geopolitical issues. Moreover, it remains vulnerable to currency translation risks, which may affect its performance in the quarters ahead. A stronger U.S. dollar may depress the company's overseas business results in the near term.

Some better-ranked companies are discussed below.

Crane Company CR currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

CR delivered a trailing four-quarter average earnings surprise of 9.3%. In the past 60 days, the Zacks Consensus Estimate for Crane’s 2025 earnings has increased 2.9%.

Ferguson Enterprises Inc. FERG currently carries a Zacks Rank of 2. FERG delivered a trailing four-quarter average earnings surprise of 7.7%.

In the past 60 days, the Zacks Consensus Estimate for Ferguson’s fiscal 2026 earnings has increased 1.3%.

Parker-Hannifin Corporation PH presently carries a Zacks Rank of 2. PH delivered a trailing four-quarter average earnings surprise of 6.2%.

In the past 60 days, the consensus estimate for Parker-Hannifin’s fiscal 2026 earnings has increased 3.2%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite