|

|

|

|

|||||

|

|

|

Credo Technology Group Holding Ltd (CRDO) ended the first quarter of fiscal 2026 strongly, with revenue growth of 274% and a fortified balance sheet, boasting a cash position of $479.6 million. Management has signaled confidence that this financial flexibility will continue to fuel the next leg of growth, while maintaining a considerable cash buffer.

This cash strength is strategically valuable as Credo deepens its role in the hyperscale ecosystem. Customer ramps are intensifying. In the fiscal first quarter, three hyperscalers each contributed more than 10% of revenues, with a material revenue contribution also coming from a fourth hyperscaler. It expects revenues from the additional hyperscaler to increase throughout fiscal 2026.

Increasing funds offer Credo meaningful internal funding capacity to invest in system-level platform expansion and new product initiatives. In the past few months, the company has unveiled new products like Bluebird DSP, Weaver memory fanout gearbox and ZeroFlap optical transceiver to capture market share.

Credo Technology Group Holding Ltd. price-consensus-eps-surprise-chart | Credo Technology Group Holding Ltd. Quote

Also, a strong balance sheet is likely to fuel M&A activity, which can supplement organic growth. Acquisitions accelerate access to the latest technologies and provide valuable tools and market access that accelerate and amplify organic growth. CRDO acquired Hyperlume privately held developer of miniature light-emitting diode (microLED) technology-based optical interconnects for chip-to-chip communication. With this buyout, CRDO expects to boost its next-generation connectivity solutions as AI, cloud and hyperscale data centers place unprecedented demands on data infrastructure deployments.

For fiscal 2026, CRDO anticipates mid-single-digit sequential revenue growth, resulting in a roughly 120% year-over-year increase. Credo expects non-GAAP operating expenses to rise less than 50% year over year in fiscal 2026. Non-GAAP net margin is projected to be around 40% both in the upcoming quarters and for fiscal 2026.

For a company riding the AI infrastructure wave, this liquidity is a potential accelerator to seize revenue opportunities.

However, challenges remain. Increasing market competition and macroeconomic uncertainties amid tariff troubles may impact CRDO’s growth trajectory. Credo competes with semiconductor giants like Broadcom (AVGO) and Marvell Technology (MRVL). Higher working capital needs can impact cash flows. The company delivered $54.2 million in operating cash flow during the fiscal first quarter, down slightly from the fourth quarter due to higher working capital.

Amid all, this depends on management’s execution to utilize its financial firepower judiciously to boost innovation and secure strategic wins while deftly managing risks and challenges.

Broadcom is one of the giants in the semiconductor space. As of Aug. 3, 2025, cash and cash equivalents were $10.7 billion, giving enough flexibility to AVGO to execute M&A, boost R&D, and expand manufacturing capacity amid the AI boom. AVGO sees massive opportunities in the AI space as its three hyperscaler customers have started to develop their own XPUs. Broadcom generated $7.17 billion in cash flow from operations, while free cash flow was $7 billion in the last reported quarter.

However, AVGO’s acquisition-driven growth strategy (mainly the VMware acquisition) had led to a hefty debt on its balance sheet. Long-term debt was $62.8 billion at the end of last quarter. Notably, ample free cash flow generation offers a cushion for servicing/reducing its debt.

Marvell had about $1.22 billion in cash and cash equivalents at the end of the last reported quarter. The company is using its cash pile to capture AI-driven opportunities in cloud and data center infrastructure through scaling of the R&D investment. The offloading of the automotive Ethernet business resulted in proceeds of $2.5 billion. MRVL plans to use the proceeds to boost buybacks and invest in technology capabilities.

The company’s data center segment has emerged as the biggest contributor with 74% contribution to total revenues. Revenues jumped 69% year over year to strong growth across AI-driven demand for custom XPU and XPU-attached products, as well as the electro-optics interconnect portfolio. Like AVGO, Marvell too has a highly leveraged balance sheet with a long-term debt of $3.97 billion as of Aug. 2, 2025.

Shares of CRDO have lost 1.8% in the past month against the Electronics-Semiconductors industry’s growth of 1.9%.

In terms of the forward 12-month Price/Sales ratio, CRDO is trading at 20.81, higher than the Electronic-Semiconductors sector’s multiple of 7.56.

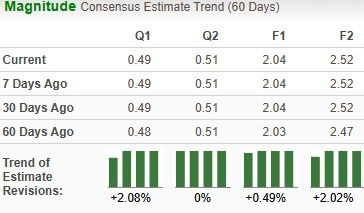

The Zacks Consensus Estimate for CRDO’s earnings for fiscal 2026 has been marginally revised upwards over the past 60 days.

CRDO currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 27 min | |

| 2 hours | |

| 3 hours | |

| 8 hours | |

| Jul-19 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite