|

|

|

|

|||||

|

|

|

Let’s dig into the relative performance of Sea (NYSE:SE) and its peers as we unravel the now-completed Q3 online marketplace earnings season.

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

The 13 online marketplace stocks we track reported a strong Q3. As a group, revenues beat analysts’ consensus estimates by 2.4% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 10.9% since the latest earnings results.

Founded in 2009 and a publicly traded company since 2017, Sea (NYSE:SE) started as a gaming platform and has since expanded to offer a variety of services such as e-commerce, digital payments, and financial services across Southeast Asia.

Sea reported revenues of $5.99 billion, up 36.5% year on year. This print exceeded analysts’ expectations by 6.1%. Overall, it was a very strong quarter for the company with impressive growth in its users.

“After a very strong first half of the year, our momentum has continued into the third quarter. Our focus remains the same: continuing to deliver high and profitable growth across all three of our businesses. With e-commerce and digital finance penetration in our markets still low but increasing, strong growth lays the best foundation to maximize our long-term profitability,” said Forrest Li, Sea’s Chairman and Chief Executive Officer.

Sea pulled off the biggest analyst estimates beat of the whole group. The company reported 65.9 million users, up 31.3% year on year. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 16.8% since reporting and currently trades at $128.92.

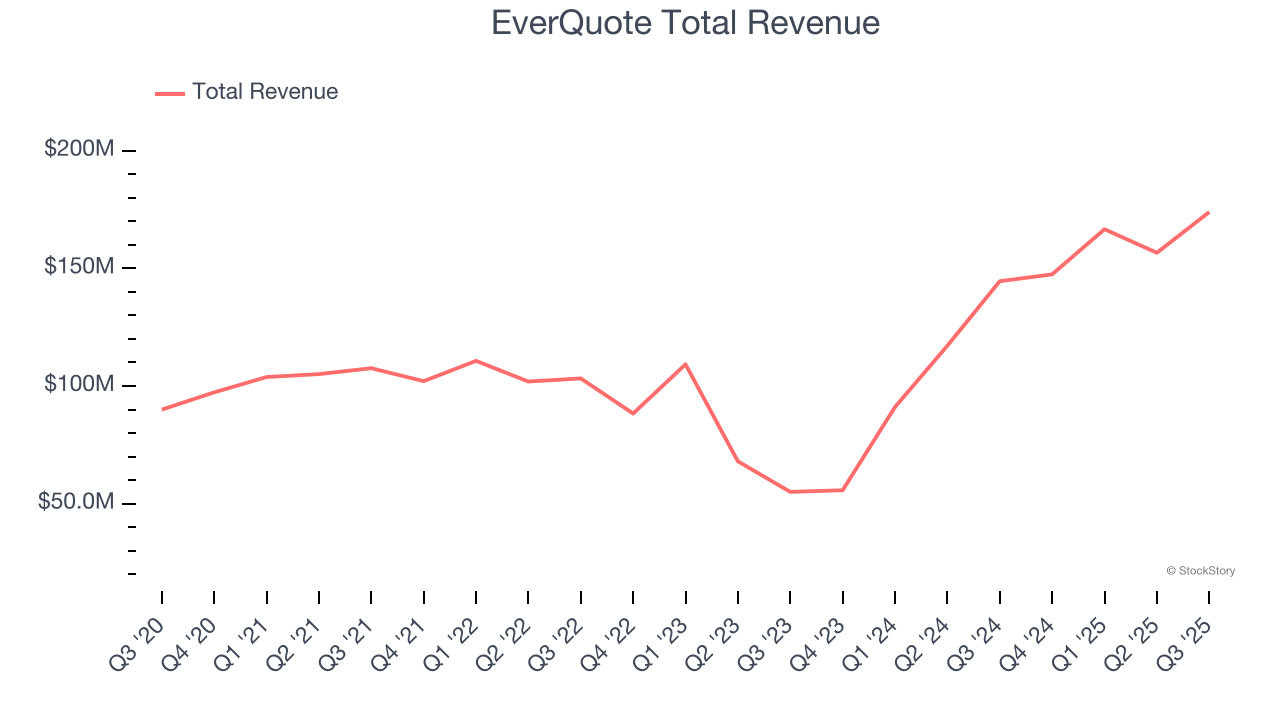

Aiming to simplify a once complicated process, EverQuote (NASDAQ:EVER) is an online insurance marketplace where consumers can compare and purchase various types of insurance from different providers

EverQuote reported revenues of $173.9 million, up 20.3% year on year, outperforming analysts’ expectations by 4.3%. The business had an exceptional quarter with a solid beat of analysts’ EBITDA estimates and revenue guidance for next quarter exceeding analysts’ expectations.

The market seems happy with the results as the stock is up 6% since reporting. It currently trades at $23.75.

Is now the time to buy EverQuote? Access our full analysis of the earnings results here, it’s free for active Edge members.

Founded in 2014, ACV Auctions (NASDAQ:ACVA) is an online auction marketplace for car dealers and wholesalers to buy and sell used cars.

ACV Auctions reported revenues of $199.6 million, up 16.5% year on year, in line with analysts’ expectations. It was a disappointing quarter as it posted full-year revenue and EBITDA guidance missing analysts’ expectations.

ACV Auctions delivered the weakest performance against analyst estimates in the group. The company reported 218,065 units sold, up 9.9% year on year. As expected, the stock is down 18% since the results and currently trades at $6.68.

Read our full analysis of ACV Auctions’s results here.

Originally started as a joint venture between several media companies including The Washington Post and The New York Times, Cars.com (NYSE:CARS) is a digital marketplace that connects new and used car buyers and sellers.

Cars.com reported revenues of $181.6 million, up 1.1% year on year. This result was in line with analysts’ expectations. Aside from that, it was a mixed quarter as its performance in some other areas of the business was disappointing.

The company reported 19,526 active buyers, up 1.4% year on year. The stock is up 6.6% since reporting and currently trades at $11.09.

Read our full, actionable report on Cars.com here, it’s free for active Edge members.

Originally featuring a library that included many of founder Jon Oringer’s photos, Shutterstock (NYSE:SSTK) is now a digital platform where customers can license and use hundreds of millions of pieces of content.

Shutterstock reported revenues of $260.1 million, up 3.8% year on year. This number beat analysts’ expectations by 1.6%. Overall, it was an exceptional quarter as it also logged a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ number of paid downloads estimates.

The company reported 111.7 million service requests, down 0.5% year on year. The stock is down 7.1% since reporting and currently trades at $20.18.

Read our full, actionable report on Shutterstock here, it’s free for active Edge members.

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-22 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite