|

|

|

|

|||||

|

|

|

Over the past six months, Jamf has been a great trade, beating the S&P 500 by 11.7%. Its stock price has climbed to $12.90, representing a healthy 23.2% increase. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Jamf, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

Despite the momentum, we're cautious about Jamf. Here are three reasons why JAMF doesn't excite us and a stock we'd rather own.

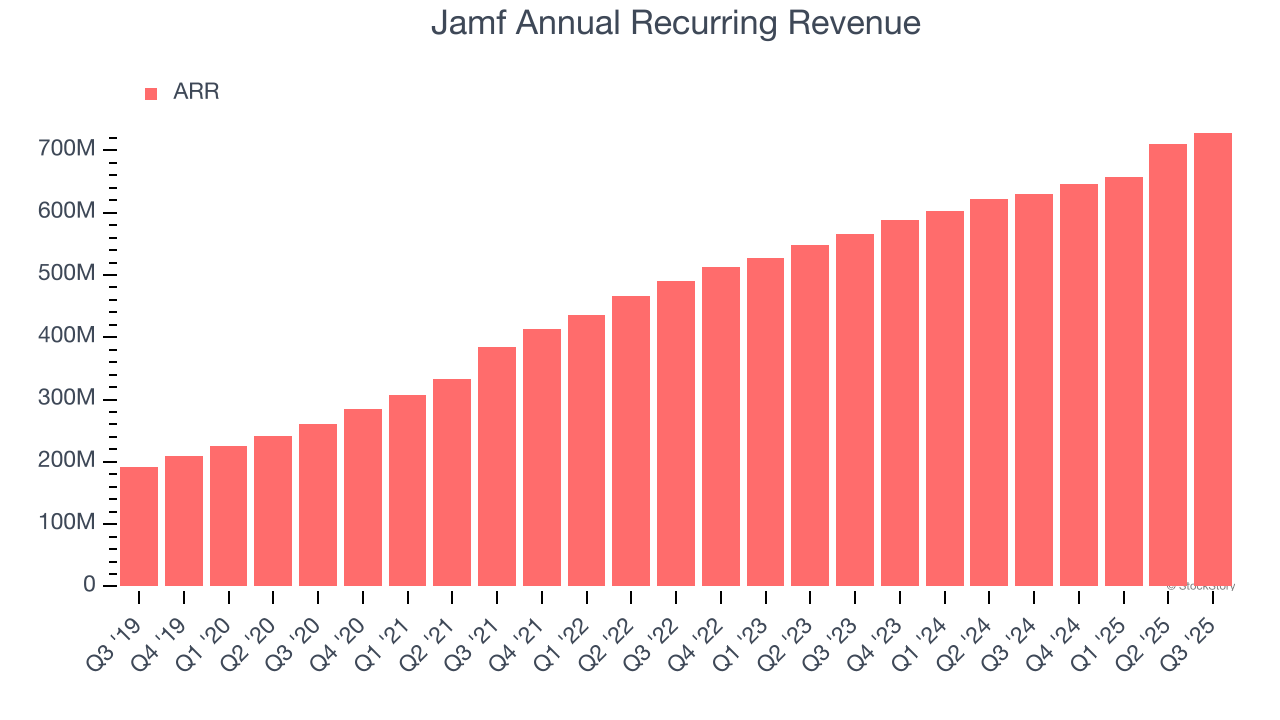

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Jamf’s ARR came in at $728.6 million in Q3, and over the last four quarters, its year-on-year growth averaged 12.2%. This performance was underwhelming and suggests that increasing competition is causing challenges in securing longer-term commitments.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Jamf’s revenue to rise by 9.6%, a deceleration versus its 22.5% annualized growth for the past five years. This projection doesn't excite us and implies its products and services will face some demand challenges.

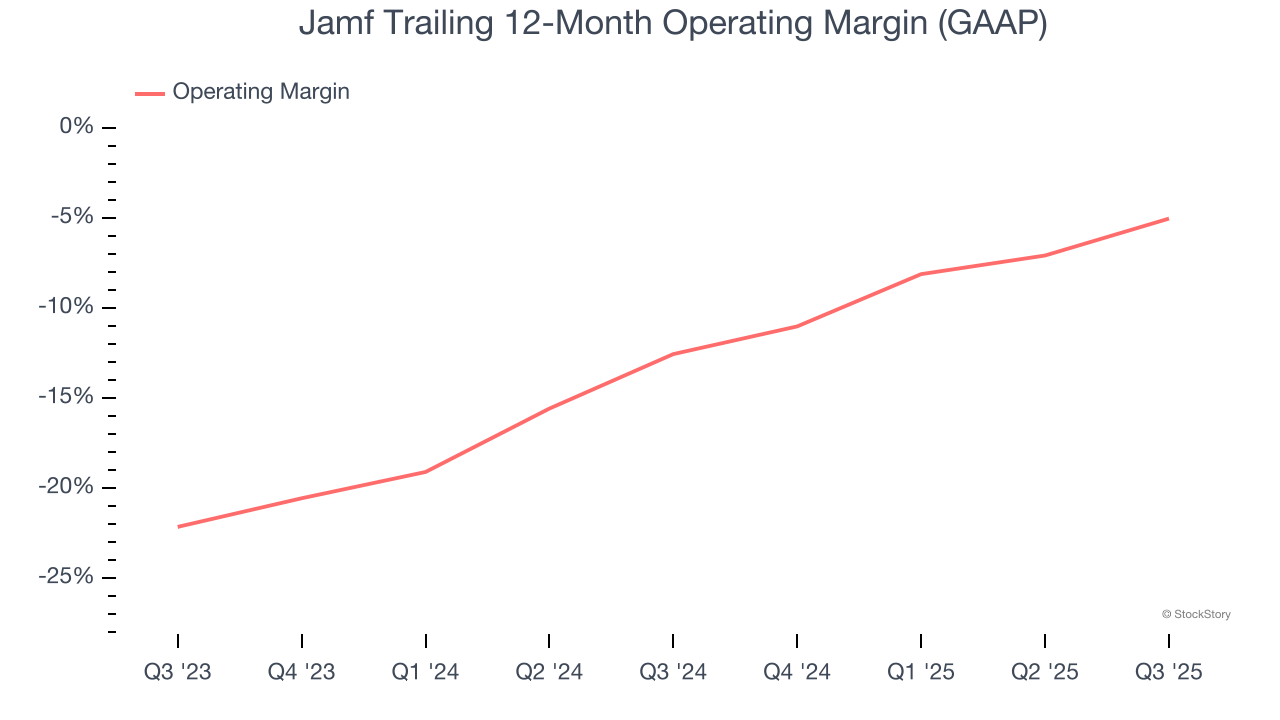

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Jamf’s expensive cost structure has contributed to an average operating margin of negative 5% over the last year. Unprofitable, high-growth software companies require extra attention because they spend heaps of money to capture market share. As seen in its fast historical revenue growth, this strategy seems to have worked so far, but it’s unclear what would happen if Jamf reeled back its investments. Wall Street seems to think it will face some obstacles, and we tend to agree.

Jamf isn’t a terrible business, but it isn’t one of our picks. With its shares topping the market in recent months, the stock trades at 2.3× forward price-to-sales (or $12.90 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere. Let us point you toward the most entrenched endpoint security platform on the market.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jan-30 |

Francisco Partners Completes Acquisition of Jamf

Business Wire

|

| Jan-23 | |

| Jan-18 | |

| Jan-15 | |

| Jan-12 |

Jamf names David Helfer as Chief Revenue Officer

Business Wire

|

| Jan-12 |

Jamf debuts #RetailRunsOniOS World Tour at NRF 2026

Business Wire

|

| Jan-09 | |

| Jan-09 | |

| Jan-08 | |

| Jan-07 | |

| Jan-06 | |

| Jan-05 |

3 Stocks Under $50 We Think Twice About

StockStory

|

| Dec-23 | |

| Dec-15 | |

| Dec-14 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite