|

|

|

|

|||||

|

|

|

Hewlett Packard Enterprise HPE and Cisco Systems CSCO are prominent players in the networking space. After acquiring Juniper Networks, HPE has emerged as a direct competitor to Cisco, with both companies now overlapping across most major segments of the networking market.

Furthermore, with the recent boom in the networking space with the advent of AI and high performance computing, the question remains: Which stock has more upside potential? Let us break down their fundamentals, growth prospects, market challenges and valuation to determine which offers a more compelling investment case.

HPE’s networking business includes wired and wireless local area networks, data center switching, software-defined wide-area-networks, cellular network software, network security and the HPE Aruba Networking. HPE provides comprehensive solutions for AIOps, enterprise connectivity, SASE and next-generation firewalls, data center and AI-native networking.

The acquisition of Juniper Networks on July 2, 2025 deepened its networking portfolio with new capabilities like cloud-native and AI-driven networks. The acquisition of Juniper Networks has also enabled HPE to cater beyond campus and branch networking by incorporating routers, data-center networking, and firewalls from Juniper Networks.

HPE made this strategic acquisition of Juniper Networks, partly to shift its networking mix toward high margin businesses. HPE’s Networking operating profit was $360 million, up 43% year over year in the third quarter of fiscal 2025. The margins benefited from both Juniper Networks acquisition and Intelligent Edge improvements, while Intelligent Edge itself delivered an operating margin of 22.7%.

However, the gain in HPE’s networking business is offset by low margin traditional server, high capex AI server and hardware-focused portfolio which comprises the major portion of HPE’s revenue sources. HPE expects its fiscal 2025 non-GAAP net earnings per share in the range $1.78-$1.90. The Zacks Consensus Estimate for fiscal 2025 earnings has been pegged at $1.90 per share, indicating a year-over-year decline of 4.52%.

Cisco Systems is the undisputed king of the networking space with its offerings covering a full-stack portfolio of switching, routing, wireless, servers, software, and SaaS services designed to support on-prem, cloud-managed, and hybrid systems. The company with its deep expertise supports the networking requirements of campus, branch, mobile, and data center networks.

Cisco Systems networking revenues are on a path to recovery as reflected in the first quarter of fiscal 2026. The revenues from Networking were $7.77 billion, up 15% on a year-over-year basis driven by robust demand for AI infrastructure and campus networking solutions.

As the refresh cycle for 4K and 6K switches support ends soon CSCO’s next-generation solutions, including smart switches, secure routers and Wi-Fi 7 wireless products are expected to gain traction benefiting Cisco’s campus networking business.

Cisco experienced a fifth consecutive quarter of double-digit growth, driven by hyperscale infrastructure, enterprise routing, campus switching, wireless, industrial IoT and servers. The networking product orders grew in the high teens in the first quarter of fiscal 2026 and is expected to grow throughout fiscal 2026.

These factors are likely to support Cisco’s top and bottom-line growth. The Zacks Consensus Estimate for fiscal 2026 revenues has been pegged at $60.8 billion, indicating year-over-year growth of 7.3%. The Zacks Consensus Estimate for fiscal 2026 earnings has been pegged at $4.09 per share, indicating a year-over-year decline of 7.4%.

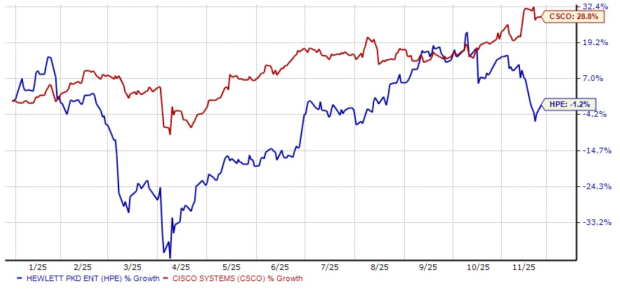

Year to date, HPE shares have lost 1.2% against the 28.8% rise in CSCO shares.

On the valuation front, HPE trades at a forward 12-month P/S multiple of 0.68X, significantly lower than Cisco’s 4.93X.

Both HPE and CSCO are benefiting from the rise in demand for the advanced networking systems used in AI and high performance computing. However, HPE faces margin compression in server business, which is a concern for the investors.

HPE currently carries Zacks Rank #5 (Strong Sell), while CSCO carries a Zacks Rank #3 (Hold), which makes it a clear winner among the two.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| 8 hours | |

| 8 hours | |

| 8 hours | |

| 10 hours | |

| 11 hours | |

| 11 hours | |

| 12 hours | |

| 12 hours | |

| 13 hours | |

| Aug-09 | |

| Aug-09 | |

| Aug-08 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite