|

|

|

|

|||||

|

|

|

Salesforce CRM is scheduled to release third-quarter fiscal 2026 results on Dec. 3.

For the fiscal third quarter, the company expects total revenues between $10.24 billion and $10.29 billion (midpoint at $10.265 billion). The Zacks Consensus Estimate for third-quarter revenues is pegged at $10.26 billion, which indicates an increase of 8.7% from the year-ago quarter’s reported figure.

CRM anticipates non-GAAP earnings per share in the band of $2.84-$2.86 for the third quarter. The consensus mark for non-GAAP earnings has remained unchanged at $2.85 over the past 60 days, which calls for an 18.3% jump from the year-ago quarter’s level.

Salesforce’s earnings beat the Zacks Consensus Estimate in three of the trailing four quarters and missed in one, the average surprise being 3.2%.

Salesforce Inc. price-eps-surprise | Salesforce Inc. Quote

Our proven model does not conclusively predict an earnings beat for Salesforce this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is not the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

Salesforce has an Earnings ESP of 0.00% and a Zacks Rank #3 at present. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Salesforce appears well-positioned to report strong third-quarter results, driven by its strategic focus on digital transformation and cloud solutions. With businesses globally undergoing digital overhauls, Salesforce's commitment to aligning its product offerings with customer needs is likely to have boosted its revenues for the quarter.

The growing demand for generative AI-enabled cloud solutions has been a major catalyst for Salesforce. By embedding generative AI tools across its products, the company not only enhances customer engagement but also strengthens its competitive position in the customer relationship management space. This forward-thinking approach might have significantly contributed to its top-line growth during the to-be-reported quarter.

Salesforce’s ability to deepen relationships with leading brands across industries and expand its reach in key geographic markets remains a cornerstone of its growth strategy. The company’s increasing footprint in the public sector is likely to have provided a further boost, unlocking new growth opportunities during the third quarter.

The acquisitions of Waii, Convergence.ai and Zoomin have been pivotal in enhancing Salesforce's capabilities and diversifying its revenue base. These additions are likely to have driven higher subscription revenues, particularly across its core cloud services. Salesforce’s key cloud offerings, including Sales, Service, Platform & Other, Marketing & Commerce and Data, are expected to have delivered robust growth.

Third-quarter revenue estimates for Sales, Service, Platform & Other, Marketing & Commerce and Integration & Analytics cloud services are pegged at $2.3 billion, $2.49 billion, $2.07 billion, $1.4 billion and $1.44 billion, respectively. We expect revenues of approximately $9.7 billion and $560.1 million for the Subscription and Support segment and the Professional Services division, respectively.

The ongoing cost restructuring initiative is likely to have boosted Salesforce’s profitability in the third quarter. The company’s second-quarter fiscal 2026 non-GAAP operating margin expanded 60 basis points to 34.3%, mainly driven by the benefits of cost restructuring initiatives, which include the trimming of the workforce and a reduction in office spaces.

Year to date, Salesforce shares have plunged 31.7%, underperforming the Zacks Computer – Software industry’s rise of 6.6%. Compared to its peers, CRM stock has also underperformed other enterprise software makers, including SAP SE SAP, Oracle ORCL and Microsoft MSFT. Year to date, shares of Oracle and Microsoft have gained 20.5% and 15.3%, respectively. Shares of SAP have declined 2.5% over the same time frame.

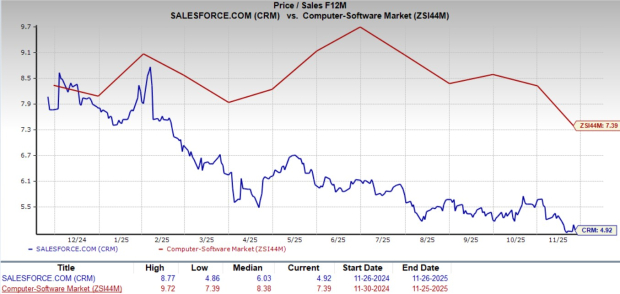

Now, let’s look at the value Salesforce offers investors at the current levels. CRM stock is trading at a discount with a forward 12-month P/S of 4.92X compared with the industry’s 7.39X.

CRM stock also trades at a discounted multiple compared with SAP, Oracle and Microsoft. At present, SAP, Oracle and Microsoft have P/S multiples of 6.25, 7.81 and 11.53, respectively.

Salesforce is the undisputed leader in the customer relationship management industry, consistently outpacing rivals like Microsoft, Oracle and SAP. Gartner’s annual rankings reaffirm its top position year after year. Its ability to maintain this dominance stems from its expansive product suite, seamless integrations and innovative approach to enterprise solutions.

Strategic acquisitions have played a crucial role in strengthening its market position. The $27.7-billion acquisition of Slack in 2021 significantly enhanced its collaboration capabilities, making Salesforce a comprehensive enterprise software provider. The $1.9-billion acquisition of Own Company in 2024 bolstered its data protection and AI capabilities, a move that aligns with growing enterprise priorities around security and automation. The most recently completed acquisition of Informatica is anticipated to strengthen Salesforce's ability to provide advanced, AI-driven analytics and automation across its product suite.

Salesforce’s AI initiatives further cement its leadership. Since introducing Einstein GPT in March 2023, the company has expanded its AI-driven functionalities across its entire ecosystem. This technology enhances automation, streamlines workflows and improves customer interactions, giving Salesforce a significant advantage as AI adoption accelerates across industries.

Nonetheless, Salesforce’s near-term prospects might be hurt by softening IT spending. Enterprises are postponing their large IT spending plans due to a weakening global economy amid ongoing macroeconomic and geopolitical issues. This does not bode well for Salesforce’s prospects in the near term.

The company’s leadership in customer relationship management and aggressive AI expansion creates a solid foundation for sustained growth. Its ability to deliver earnings growth despite ongoing macroeconomic uncertainties makes the stock worth holding.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 35 min | |

| Jul-29 | |

| Jul-29 |

Even $64 Billion in Quarterly Profit Is a Disappointment for Chip Investors

MSFT MSFT +8.83% AH

The Wall Street Journal

|

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite