|

|

|

|

|||||

|

|

|

AstraZeneca AZN and Merck MRK are both major global pharmaceutical companies with diversified drug portfolios. While Merck is a U.S.-based company, AstraZeneca’s headquarters are in Cambridge, UK.

Both companies enjoy a strong leadership position in oncology. Oncology drives more than 60% of Merck’s total revenues, with its blockbuster cancer drug Keytruda contributing more than 50% of the company’s pharmaceutical sales.

For AstraZeneca, oncology sales now comprise around 43% of total revenues and rose 16% in the first nine months of 2025.

AstraZeneca also has a solid presence in immunology, rare diseases, vaccines, as well as cardiovascular and respiratory, while Merck markets products in vaccines, neuroscience, diabetes, virology and animal health.

Interestingly, Merck and AstraZeneca have a collaboration for PARP inhibitor therapy, Lynparza.

Both companies face pressures from declining legacy brands and rising competition across markets. But which one is a better investment option today? Let’s take a closer look at their fundamentals, growth prospects and challenges to make an informed choice.

Merck boasts more than six blockbuster drugs in its portfolio, with Keytruda being the key top-line driver. Keytruda has played an instrumental role in driving Merck’s steady revenue growth in the past few years. Keytruda recorded sales of $23.3 billion in the first nine months of 2025, up 8% year over year. Keytruda’s sales are gaining from rapid uptake across earlier-stage indications, mainly early-stage non-small cell lung cancer.

Merck’s subcutaneous formulation of Keytruda, known as Keytruda Qlex, was approved by the FDA in September 2025. Keytruda Qlex can offer substantially quicker administration time than intravenous infusion of Keytruda.

MRK’s phase III pipeline has almost tripled since 2021, supported by in-house pipeline progress as well as the addition of candidates through M&A deals. This has positioned Merck to launch around 20 new vaccines and drugs over the next few years, with many having blockbuster potential. These include Merck’s new 21-valent pneumococcal conjugate vaccine, Capvaxive, and pulmonary arterial hypertension drug, Winrevair. Both these products have witnessed a strong launch and have the potential to generate significant revenues over the long term.

The $10 billion acquisition of Verona in 2025 added Ohtuvayre, a novel, first-in-class maintenance treatment for chronic obstructive pulmonary disease, with multibillion-dollar commercial potential. Earlier this month, Merck announced a definitive agreement to acquire Cidara Therapeutics CDTX for approximately $9.2 billion.

The acquisition will add CDTX’s lead pipeline candidate, CD388, a first-in-class long-acting, strain-agnostic antiviral agent, currently being evaluated in late-stage studies for the prevention of seasonal influenza in individuals at higher risk of complications.

Merck’s Animal Health business is also a key contributor to its top-line growth, as the company is recording above-market growth.

However, sales of Gardasil, which is Merck’s second-largest product, are declining due to weak performance in China, resulting from sluggish demand trends amid an economic slowdown. Sales of some other Merck vaccines, like Proquad, M-M-R II, Varivax, Rotateq and Pneumovax 23, have also declined so far in 2025. Merck is also seeing weakness in the diabetes franchise and the generic erosion of some drugs.

Merck is heavily reliant on Keytruda. Though Keytruda may be Merck’s biggest strength and a solid reason to own the stock, it can also be argued that the company is excessively dependent on the drug, and it should look for ways to diversify its product lineup.

There are rising concerns about the firm’s ability to grow its non-oncology business ahead of the upcoming loss of exclusivity of Keytruda in 2028.

Also, competitive pressure might increase for Keytruda in the near future from dual PD-1/VEGF inhibitors like Summit Therapeutics’ SMMT ivonescimab that inhibit both the PD-1 pathway and the VEGF pathway at once. They are designed to overcome the limitations of single-target therapies like Keytruda.

AstraZeneca has several blockbuster medicines in its portfolio with sales exceeding $1 billion, including Tagrisso, Fasenra, Farxiga, Imfinzi, Lynparza, Calquence and Ultomiris. These drugs are driving the company’s top line, backed by increasing demand trends. Almost every new product that has been launched in recent years has done well.

Newer drugs like Wainua, Airsupra, Saphnelo, Datroway (partnered with Daiichi Sankyo) and Truqap are also contributing to top-line growth in 2025, more than offsetting the loss of exclusivity of some mature brands like Brilinta, Pulmicort and Soliris. The rare disease business also improved in the third quarter.

Backed by its new products and pipeline drugs, AstraZeneca believes it can post industry-leading top-line growth in the 2025-2030 period. AstraZeneca expects to generate $80 billion in total revenues by 2030. By the said time frame, AstraZeneca plans to launch 20 new medicines, with nine new medicines already launched/approved. It believes that many of these new medicines will have the potential to generate more than $5 billion in peak-year revenues. The company is also on track to achieve a mid-30s percentage core operating margin by 2026.

In October, AstraZeneca signed a drug pricing agreement with the Trump administration. The firm has offered to cut prescription drug prices and align prices with those in other developed countries. AstraZeneca also agreed to boost domestic investments in exchange for a three-year exemption from tariffs on pharmaceutical imports. In July, it announced plans to invest $50 billion in U.S. manufacturing and R&D by 2030.

AstraZeneca faces its share of challenges, like the impact of Part D redesign on U.S. oncology sales and ongoing investigations at its China subsidiary. Generic/biosimilar competition in the United States and Europe is hurting sales of key drugs like Brilinta and Soliris in 2025. Generic versions of Brilinta were launched in the United States in 2025. Biosimilar versions of Soliris were launched in the United States in March 2025.

AstraZeneca expects fourth-quarter revenues of Farxiga and Lynparza to be affected by volume-based procurement (VBP)-associated stock compensation costs and year-end hospital budget capping in China. VBP policy is an initiative by the Chinese government to lower the prices of pharmaceuticals and medical devices by awarding large contracts to the lowest bidder. Tender order variability in emerging markets is also expected to hurt fourth-quarter revenues.

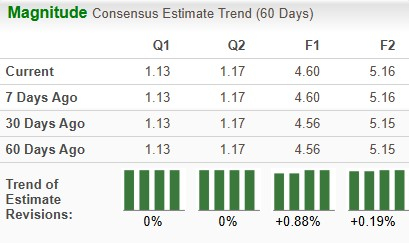

The Zacks Consensus Estimate for AZN’s 2025 sales and EPS implies a year-over-year increase of 8.7% and 11.9%, respectively. EPS estimates for 2025 have risen from $4.56 per share to $4.60 per share over the past 30 days, while those for 2026 have risen from $5.15 to $5.16 per share over the same timeframe.

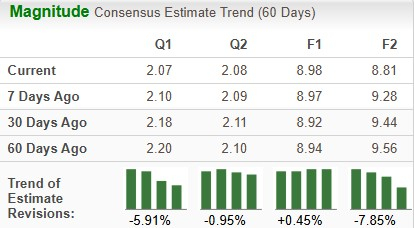

The Zacks Consensus Estimate for MRK’s 2025 sales and EPS implies a year-over-year increase of 1.0% and 17.4%, respectively. EPS estimates for 2025 have risen from $8.92 per share to $8.98 per share over the past 30 days, while those for 2026 have declined from $9.44 to $8.81 per share over the same timeframe.

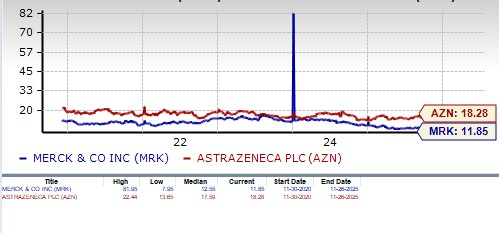

Year to date, AstraZeneca’s stock has risen 42.5% compared with the industry’s increase of 19.1%. Merck’s stock has risen 5.2%.

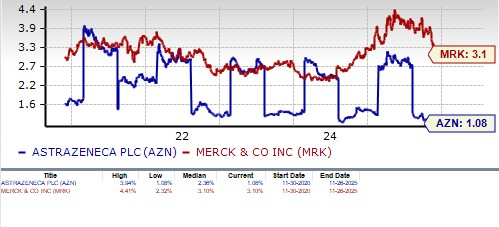

MRK looks more attractive than AstraZeneca from a valuation standpoint. Going by the price/earnings ratio, AstraZeneca’s shares currently trade at 18.28 forward earnings, higher than 17.47 for the industry and its 5-year mean of 17.59. Merck’s shares currently trade at 11.85 forward earnings, significantly lower than the industry as well as the stock’s 5-year mean of 12.55.

AstraZeneca’s dividend yield is 1.08/% while Merck’s is higher at 3.1%.

Merck and AstraZeneca have a Zacks Rank #3 (Hold) each, which makes choosing one stock a difficult task. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Merck has one of the world’s best-selling drugs in its portfolio, generating billions of dollars in revenues. Though Keytruda will lose patent exclusivity in 2028, its sales are expected to remain strong until then. Merck’s new products, Capvaxive and Winrevair, are witnessing strong launches and have the potential to generate significant revenues over the long term.

Over the last couple of years, it has been acquiring new products like Ohtuvayre, which can be long-term growth drivers and help fill the potential revenue gap created by Keytruda’s upcoming LOE.

However, Merck faces several challenges, including persistent challenges for Gardasil in China, potential competition for Keytruda and rising competitive and generic pressure for some of its drugs. All these factors have raised doubts about Merck’s ability to navigate the Keytruda LOE period successfully.

On the other hand, AstraZeneca has clearer growth targets ($80 billion in revenues by 2030).

AstraZeneca is a safer bet than Merck, as it has demonstrated more efficient profitability, and its upside potential appears to be higher. Merck’s upcoming LOE for Keytruda and the volatility in stock price tilt us in favor of AstraZeneca, despite Merck’s discounted valuation and better dividend yield. AZN’s stock price performance and estimate movement have been better than Merck’s.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 5 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 8 hours | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite