|

|

|

|

|||||

|

|

|

Dollar Tree, Inc. DLTR is likely to register a decline in its top and bottom lines when it reports third-quarter fiscal 2025 results on Dec. 3, before market open. The Zacks Consensus Estimate for revenues is pegged at $4.74 billion, indicating a drop of 37.3% from the prior-year quarter’s figure.

The consensus estimate for earnings is pegged at $1.09 per share, indicating a decrease of 2.7% from the year-ago period’s figure. The consensus mark has remained stable in the past 30 days.

Dollar Tree, Inc. price-consensus-eps-surprise-chart | Dollar Tree, Inc. Quote

DLTR has a trailing four-quarter negative earnings surprise of 27.5%, on average. In the last reported quarter, the Chesapeake, VA-based company’s earnings surpassed the Zacks Consensus Estimate by 102.6%.

Trends to Watch Before Dollar Tree’s Q3 Release

Dollar Tree’s third-quarter fiscal 2025 performance is expected to reflect the environment of uncertainty that management emphasized on the latest earnings call. Despite strong discretionary and consumable performance in the fiscal second quarter, management has been taking a cautious stance given the volatile macro backdrop and increased financial pressure on lower-income consumers who continue to face elevated living costs across categories.

A major factor weighing on the fiscal third-quarter results will be the timing of tariff impacts. While the fiscal second quarter benefited from some mitigation actions realized earlier than expected, management stated that a larger share of tariff pressure will shift into the fiscal third quarter. Tariffs from China remain at 30%, and sourcing nations such as Vietnam, India and Bangladesh now carry meaningfully higher rates than expected earlier in the year.

Dollar Tree continues to rely on its five mitigation levers, supplier negotiations, product re-specification, changes in sourcing origin, SKU rationalization and multi-price flexibility, but the timing shift means cost pressures will be more pronounced in the upcoming quarter.

SG&A expenses are also likely to have remained elevated in the fiscal third quarter. On the last quarter’s earnings call, management cited higher store labor related to pricing rollout and re-stickering, wage increases, depreciation from remodels and conversions and ongoing maintenance investments. General liability claim costs continue to rise across the industry, adding another layer of SG&A pressure. While the company is seeing payroll leverage and certain cost offsets, management still expects meaningful SG&A deleverage for fiscal 2025, which will contribute to third-quarter margin pressure.

On the last reported quarter’s earnings call, for the third quarter of fiscal 2025, Dollar Tree envisions adjusted EPS to be similar to the third quarter of fiscal 2024 EPS of $1.12.

On the positive front, Dollar Tree entered the fiscal third quarter with solid operating momentum. The expanded multi-price assortment, continued strength from higher-income customers and a healthy balance between traffic and ticket continue to support comp growth. Strong performance from store conversions, new openings, improved distribution center flow and the early traction of the Uber Eats partnership should provide incremental support to third-quarter fiscal 2025 revenues.

Our proven model conclusively predicts an earnings beat for Dollar Tree this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat, which is exactly the case here. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

Dollar Tree has an Earnings ESP of +0.30% and currently carries a Zacks Rank of 3.

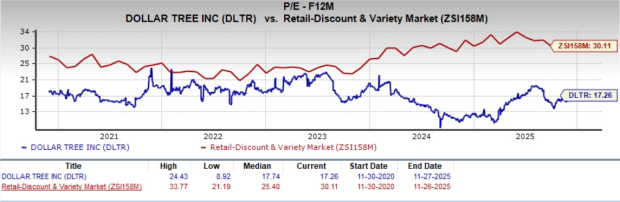

From a valuation perspective, Dollar Tree shares present an attractive opportunity, trading at a discount relative to historical and industry benchmarks. With a forward 12-month price-to-earnings ratio of 17.26X, below the five-year median of 17.74X and the Retail-Discount Stores industry’s average of 30.11X, the company’s shares offer compelling value for investors seeking exposure to the sector.

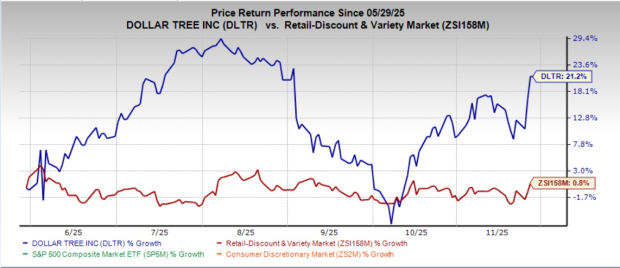

Recent market movements show that Dollar Tree’s shares have gained 21.2% in the past six months against the industry’s 0.8% decline.

Here are some companies, which according to our model, have the right combination of elements to post an earnings beat this season:

Ulta Beauty, Inc. ULTA has an Earnings ESP of +1.20% and a Zacks Rank of 2 at present. The consensus estimate for Ulta Beauty’s third-quarter fiscal 2025 earnings is pegged at $4.48 per share, implying a decline of 13% from the year-ago quarter. You can see the complete list of today’s Zacks #1 Rank stocks here.

For Ulta Beauty’s quarterly revenues, the consensus mark is pegged at $2.7 billion, which indicates an increase of 7.3% from the year-ago quarter. ULTA delivered a trailing four-quarter earnings surprise of 16.3%, on average.

Five Below, Inc. FIVE currently has an Earnings ESP of +74.71% and a Zacks Rank of 2. FIVE is likely to register a top-line increase when it reports third-quarter fiscal 2025 results. The Zacks Consensus Estimate for its quarterly revenues is pegged at $969.9 million, indicating a 15% rise from the figure reported in the prior-year quarter.

The consensus estimate for Five Below’s earnings is pegged at 22 cents per share, implying a 47.6% decline from the year-ago quarter. FIVE delivered a trailing four-quarter earnings surprise of 50.5%, on average.

American Eagle Outfitters, Inc. AEO has an Earnings ESP of +1.55% and a Zacks Rank of 2 at present. The Zacks Consensus Estimate for revenues is pegged at $1.32 billion, implying 2.33% growth from the year-ago quarter.

The consensus estimate for American Eagle earnings is pegged at 43 cents per share, implying a 10.4% decline from the year-ago quarter. FIVE delivered a trailing four-quarter earnings surprise of 30.3%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| 5 hours |

Stock Of The Day Adds To 350% Surge On Earnings But Sees 'Challenging' Road Ahead

FIVE +10.68%

Investor's Business Daily

|

| 5 hours | |

| 6 hours |

New bank capital requirements, Five Below surges over Q4 holiday results

FIVE +10.68%

Yahoo Finance Video

|

| 8 hours | |

| 10 hours | |

| 10 hours | |

| 11 hours | |

| 12 hours |

Five Below Comparable Sales Accelerate, Shares Rally On Q4 Beat

FIVE +10.68%

Investor's Business Daily

|

| 14 hours | |

| 16 hours | |

| Mar-18 | |

| Mar-18 | |

| Mar-18 |

Five Below Posts Higher Fourth-Quarter Profit as Sales Grow

FIVE +10.68% FIVE

The Wall Street Journal

|

| Mar-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite