|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Over the past six months, Costco’s shares (currently trading at $921.09) have posted a disappointing 12.7% loss, well below the S&P 500’s 14.1% gain. This may have investors wondering how to approach the situation.

Given the weaker price action, is this a buying opportunity for COST? Find out in our full research report, it’s free for active Edge members.

Designed to be a one-stop shop for the suburban consumer, Costco (NASDAQ:COST) is a membership-only retail chain that sells groceries, apparel, toys, and household items, often in bulk quantities.

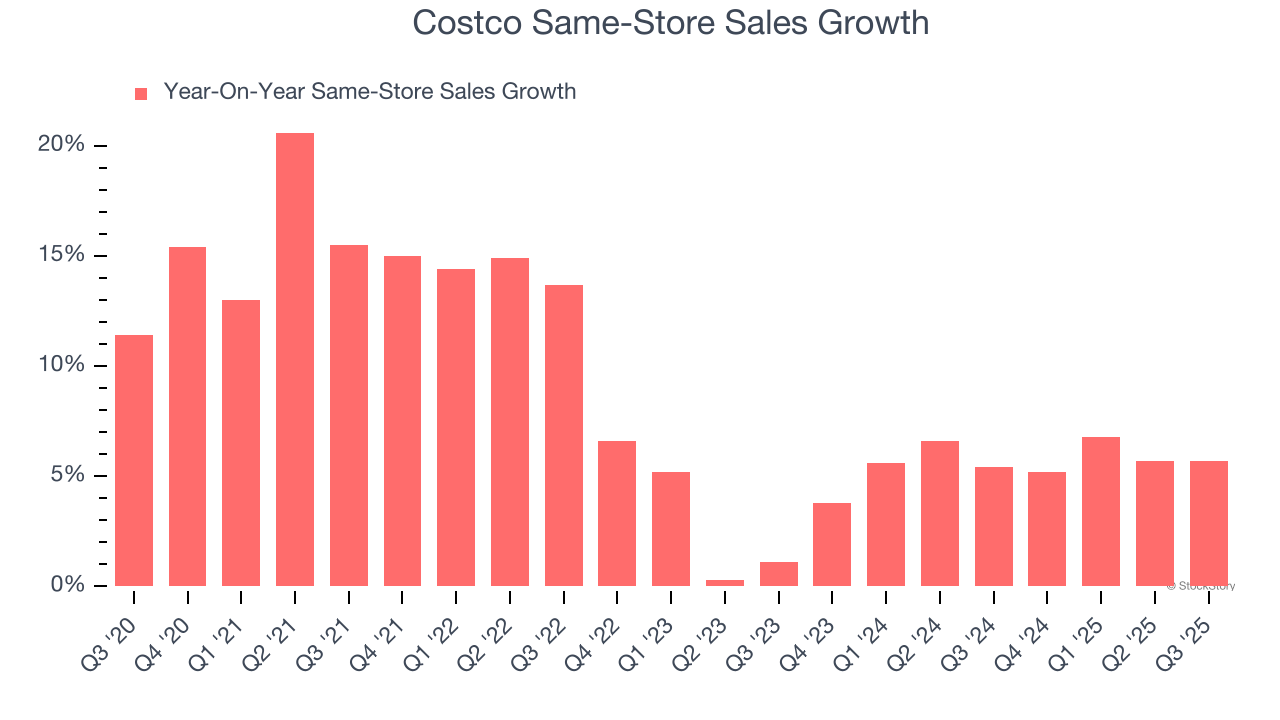

Same-store sales is a key performance indicator used to measure organic growth at brick-and-mortar shops for at least a year.

Costco has been one of the most successful retailers over the last two years thanks to skyrocketing demand within its existing locations. On average, the company has posted exceptional year-on-year same-store sales growth of 5.6%.

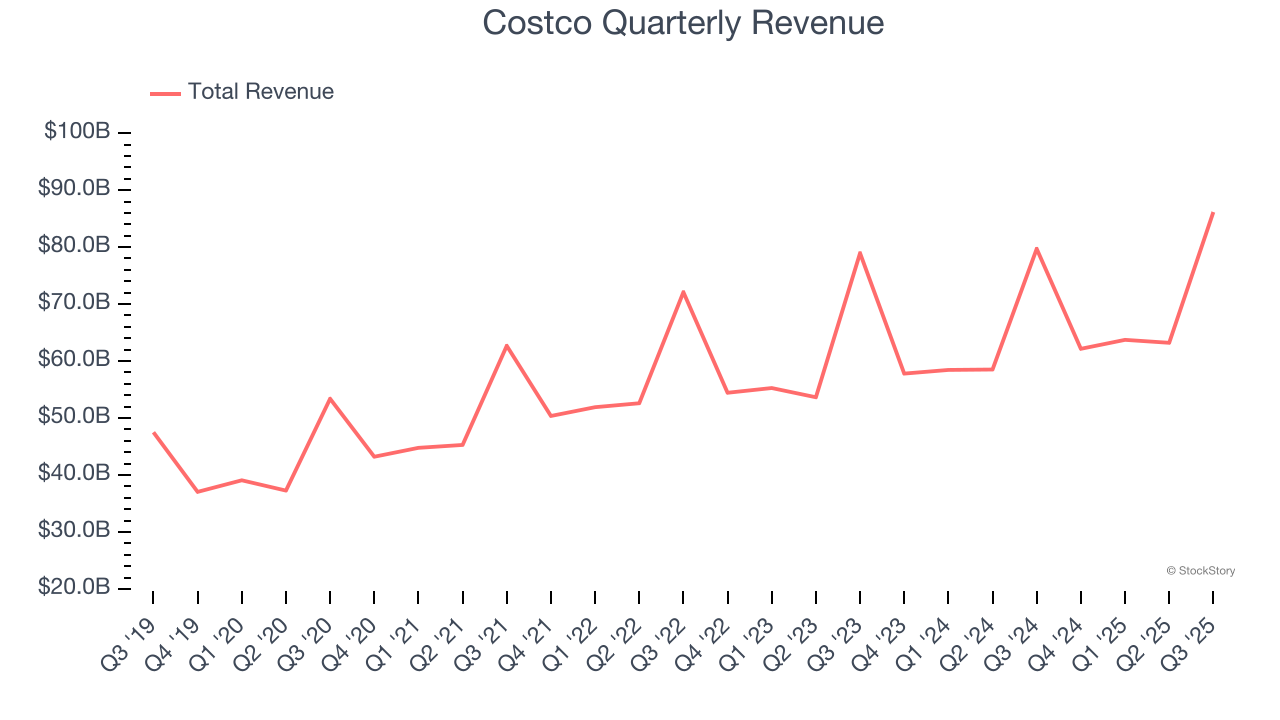

With $275.2 billion in revenue over the past 12 months, Costco is a behemoth in the consumer retail sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because there are only a finite number of places to build new stores, making it harder to find incremental growth. To expand meaningfully, Costco likely needs to tweak its prices or enter new markets.

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Costco’s sales grew at a tepid 6.6% compounded annual growth rate over the last three years. This wasn’t a great result compared to the rest of the consumer retail sector, but there are still things to like about Costco.

Costco’s positive characteristics outweigh the negatives. With the recent decline, the stock trades at 45.6× forward P/E (or $921.09 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free for active Edge members .

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| 20 min | |

| 2 hours | |

| 3 hours |

Supreme Court Strikes Down Tariffs, But Trump Adds 10% Tax (Live Coverage)

COST

Investor's Business Daily

|

| 4 hours |

Retail Giant's Bullish Trend Offers This Option Trade For Costco Stock

COST

Investor's Business Daily

|

| 5 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours |

The Latest: Supreme Court strikes down Trumps tariffs, upending central plank of economic agenda

COST

Associated Press Finance

|

| 6 hours |

The Latest: Trump addresses press after Supreme Court strikes down his sweeping tariffs

COST

Associated Press Finance

|

| 6 hours |

The Latest: Trump says hell sign an executive order to enact a 10% global tariff

COST

Associated Press Finance

|

| 6 hours | |

| 6 hours | |

| 6 hours | |

| 8 hours | |

| 14 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite