|

|

|

|

|||||

|

|

|

Founded in 1998 and based in Vancouver, Canada, Lululemon Athletica Inc. (LULU) is a yoga-inspired athletic apparel company that designs, manufactures, and distributes athletic apparel and accessories for women, men, and children. The company offers a wide variety of fitness pants, shorts, tops, and jackets designed for athletic pursuits, such as yoga training, and running. Lululemon sells its products primarily through brick-and-mortar retail stores, which are fixtures in most North American malls. However, the company is expanding through e-commerce, license and supply agreements, and retail locations worldwide.

As Lululemon’s earnings report approaches, here’s what you need to know:

· When: LULU will report EPS on Thursday, December 11th, after the market closes.

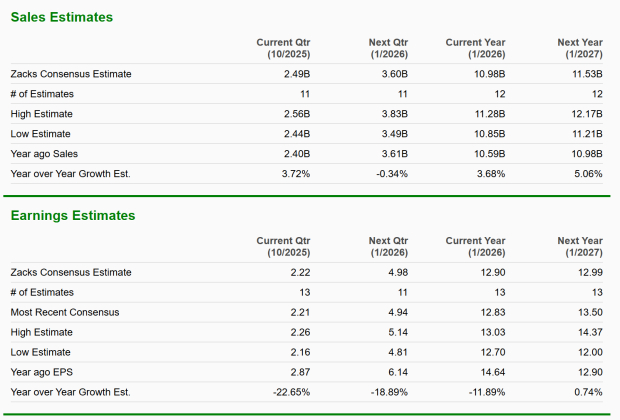

· Wall Street Expectations: Analyst expectations are low for Lulu. Zacks Consensus Analyst Estimates expect sales growth of 3.72% and negative year-over-year EPS growth.

· Expected Move: The options market is currently pricing in a move of +/- 13% following its Q3 EPS announcement.

After being a top-tier market performer over the past decade, LULU shares have finally suffered a significant correction. Year-to-date, LULU shares are down 50%, underperforming the market and its peers by a wide margin. Below are LULU’s three biggest challenges:

1. Tariff Hit: With manufacturing operations across Asia, LULU is among the companies most affected by tariffs. Tariffs and the removal of the de minimis exemption are squeezing LULU’s margins, driving a $240 million hit in fiscal 2025 and a $320 million drag in fiscal 2026, despite mitigation efforts.

2. Competition Intensifies: Imitation is the sincerest form of flattery. However, in Lulu’s case, it’s impacting earnings. Several new, digitally native brands such as Alo Yoga, Rhone, and Vuori are challenging Lulu’s brand. Meanwhile, established lifestyle brands like Nike (NKE) are improving their “athleisure” offerings.

3. North America Business Slows: Although Lulu is expanding internationally, its largest business, North America, is contracting. Lulu customers are skittish amid higher interest rates and inflation fears.

Unfortunately, these headwinds are unlikely to subside any time soon. However, the real question for Q3 EPS will be, “With the stock down 50% YTD, is the bad news already priced in?”

Bottom Line

Lululemon’s upcoming EPS report arrives at a critical moment. Once a premium growth standout, the retailer now sits in the middle of margin pressure, fierce competition, and slowing demand. With expectations already low and a stock that has corrected dramatically, the next EPS reaction may hinge on whether its poor results are priced in.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 hours | |

| 7 hours | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite