|

|

|

|

|||||

|

|

|

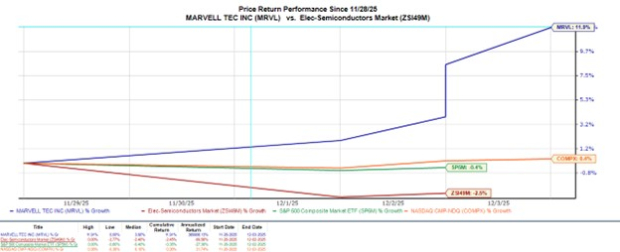

As one of the promising players in the AI landscape, Marvell Technology MRVL is making headlines after exceeding its Q3 expectations on Tuesday evening and announcing the acquisition of private semiconductor startup Celestial AI.

Marvell also provided upbeat guidance, with MRVL spiking as much as +9% in Wednesday’s trading session and trading over $100 a share for the first time in nine months.

That said, let’s see if it's time to buy stock in the innovative chipmaker, with MRVL having a 52-week high of $127.

Subject to regulatory approvals and customary closing conditions, the acquisition of Celestial AI is expected to be completed in the first half of 2026. The acquisition is valued at $3.25 billion in cash and stock, with the potential to rise to $5.5 billion if revenue milestones are met.

Celestial AI is focused on advanced photonic interconnect technology, using light to connect chips and memory in data centers, which would help Marvell to compete more directly with Broadcom AVGO and Nvidia NVDA in regard to next-gen AI infrastructure.

Acquiring Celestial AI would also strengthen Marvell’s role in the generative AI race, where hyperscalers are demanding faster, energy-efficient systems.

Posting record Q3 sales of $2.07 billion, Marvell exceeded estimates of $2.06 billion with its top line stretching 37% from $1.51 billion in the comparative quarter. More impressive, Q3 EPS of $0.76 topped expectations of $0.75 and soared 77% from $0.43 per share a year ago.

Further fueling investor sentiment is that Marvell projects stronger revenue and earnings for the next quarter and fiscal year, providing a guidance range that met and will potentially exceed Wall Street's forecast.

Fourth quarter sales were guided at around $2.2 billion ±5%, with Zacks estimates currently at $2.15 billion or 18% growth. Marvell expects Q3 EPS at $0.79 ± $0.05, with the current Zacks Consensus of $0.78 equating to 30% growth.

Driven by strong demand in data center products, Marvell sees full-year revenue growth exceeding 40%, which aligns with consensus estimates of $8.12 billion or 41% growth. Even better is that Marvell expects data center revenue growth to be higher next year, reflecting accelerating AI demand.

Considering its intriguing AI prospects, Marvell’s stock is trading at a reasonable 32X forward earnings multiple.

Trading roughly on par with its Zacks Electronics-Semiconductors industry average, MRVL has moved closer to the broader market’s forward P/E multiple of 26X and is offering a distinct discount to its 5-year median of 53X with a high of 151X during this period.

Following a favorable Q3 report, Marvell Technology's stock sports a Zacks Rank #2 (Buy). Correlating with such, earnings estimate revisions had already moved slightly higher in the last 30 days for Marvell’s current fiscal 2026 and FY27. This trend is likely to continue in the coming weeks, with Marvell’s appealing EPS growth starting to level what is now a far more reasonable P/E valuation than in the past.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 31 min | |

| 1 hour | |

| 3 hours | |

| 12 hours | |

| 12 hours | |

| Jul-18 | |

| Jul-18 | |

| Jul-18 | |

| Jul-18 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite