|

|

|

|

|||||

|

|

|

Simon Property Group SPG owns a diversified portfolio of premium retail assets in some of the key markets across the United States and globally. Solid retail real estate demand is likely to drive healthy demand for its properties, aiding leasing activity, occupancy levels and rent growth.

A focus on supporting omnichannel retailing and developing mixed-use assets is encouraging. Also, accretive buyouts and redevelopment efforts augur well for long-term growth. A healthy balance sheet is likely to aid growth endeavors.

However, growing e-commerce adoption and high debt burden raise concerns for Simon. Macroeconomic uncertainty can result in strain on retailers' balance sheets, leading to bankruptcies.

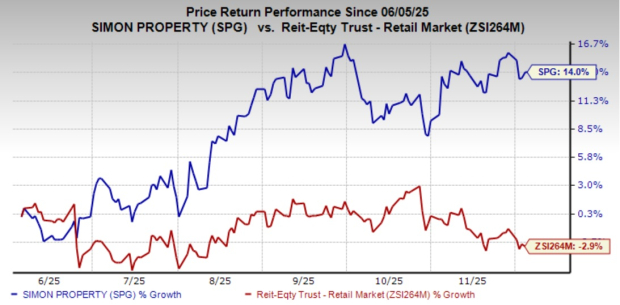

Shares of this retail REIT, carrying a Zacks Rank #3 (Hold), have gained 14.0% against the industry’s decline of 2.9% in the past six months. Analysts seem bullish on this stock, with the Zacks Consensus Estimate for its 2025 FFO per share being revised more than 1% upward to $12.65 over the past month.

Moreover, solid dividend payouts are the biggest enticements for REIT investors, and Simon Property is committed to boosting shareholder wealth. The retail REIT has increased its dividend 14 times in the past five years, and its payout has grown 11.09% over the same period. This spate of dividend increases brings additional relief to investors and reaffirms confidence in this retail landlord.

Simon Property enjoys a wide exposure to retail assets across the United States. In an improving leasing environment, the retail REIT is poised to benefit from its superior assets at premium locations. During the first nine months of 2025, it signed 819 new leases and 1,383 renewal leases (excluding mall anchors and majors, new development, redevelopment and leases with terms of one year or less) with a fixed minimum rent across its U.S. Malls and Premium Outlets portfolio. This comprised roughly 8.3 million square feet, of which 6.4 million square feet were related to consolidated properties.

Given the favorable retail real estate environment, this leasing momentum is expected to continue in the upcoming quarters. As of Sept. 30, 2025, the ending occupancy for the U.S. Malls and Premium Outlets portfolio was 96.4%, up 20 basis points from 96.2% as of Sept. 30, 2024. We expect the company’s 2025 total revenues to increase 3.9% on a year-over-year basis. We project the 2025 year-end occupancy for the U.S. Malls and Premium Outlets portfolio to be 96.1%.

Simon Property’s adoption of an omnichannel strategy and successful tie-ups with premium retailers have paid off well in recent years. Particularly, the company’s online retail platform, woven with an omnichannel strategy, augurs well for its long-term growth. Also, the mixed-use development option has gained immense popularity in recent years as it helps catch the attention of people who prefer to live, work, play and shop in the same area. In 2025, Simon Property expected to begin the development of four to five mixed-use destinations with an estimated expenditure of $400-$500 million.

The company has been restructuring its portfolio, aiming at premium acquisitions and transformative redevelopments. For the past several years, the company has been investing billions to transform its properties, focused on creating value and driving footfall at the properties. In November 2025, Simon Property Group acquired Phillips Place, an open-air retail center spanning nearly 134,000 square feet of space, in the heart of the SouthPark neighborhood of Charlotte, NC. In October 2025, Simon Property acquired the remainder 12% interest in the Taubman Realty Group. The high-quality asset buyout will be value accretive, yielding growth for the company.

Simon Property is making efforts to bolster its financial flexibility. This enabled the company to exit the third quarter of 2025 with $9.5 billion of liquidity. As of Sept. 30, 2025, Simon Property’s total secured debt to total assets was 16%, while the fixed-charge coverage ratio was 4.7, ahead of the required level. Moreover, the company enjoys a corporate investment-grade credit rating of A (stable outlook) from Standard and Poor's and a senior unsecured rating of A3 (stable outlook) from Moody’s. With solid balance sheet strength and available capital resources, it remains well-poised to tide over any mayhem and bank on growth opportunities.

Mall traffic has rebounded significantly post-pandemic. However, given the convenience of online shopping, it is likely to continue to be a popular choice among customers. This is likely to adversely impact the market share for brick-and-mortar stores and affect retail REITs, including Simon Property.

Moreover, macroeconomic uncertainty, along with the potential effects of fiscal policies such as tariffs, presents risks to the retail real estate market and can result in strain on retailers' balance sheets, leading to bankruptcies.

Some better-ranked stocks from the retail REIT sector are Phillips Edison & Company, Inc. PECO and Curbline Properties Corp. CURB. Phillips Edison and Curbline Properties each carry a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Phillips Edison’s 2025 FFO per share has been raised marginally over the past two months to $2.58 and calls for a 6.2% year-over-year increase.

The consensus estimate for Curbline Properties’ 2025 FFO per share has been revised upward marginally to $1.04 over the past two months and suggests a year-over-year rise of 31.7%.

Note: Anything related to earnings presented in this write-up represents FFO, a widely used metric to gauge the performance of REITs.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-05 | |

| Aug-05 | |

| Aug-03 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-14 | |

| Jul-06 | |

| Jul-01 | |

| Jul-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite