|

|

|

|

|||||

|

|

|

Inogen, Inc. INGN is well-poised for growth in the coming quarters, courtesy of high prospects in the portable oxygen concentrator (POC) space. The optimism, led by solid fourth-quarter 2024 performance and a strong product portfolio, seems justified. However, issues like stiff competition and forex volatility are major downsides.

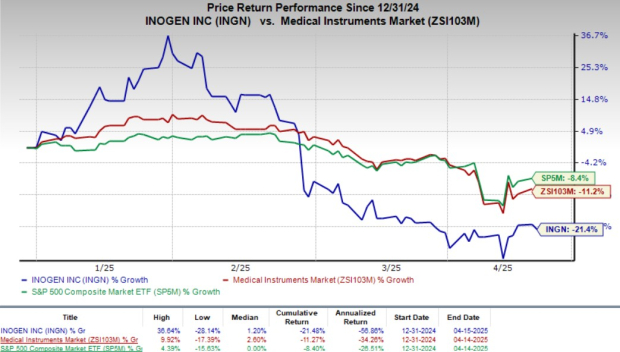

The Zacks Rank #3 (Hold) company’s shares have lost 21.4% so far this year compared with an 11.2% decline of the industry. The S&P 500 has decreased 8.4% during the same time frame.

The renowned provider of POCs has a market capitalization of $205.9 million. The company projects 7.2% earnings growth for 2025 and expects to witness continued improvements in its business going forward. Inogen’s P/S ratio of 0.6X compared with the industry’s 2.6X makes its valuation attractive.

Let us delve deeper.

Huge Prospects in the POC Space: We remain confident in the advantages of portable oxygen concentrators (POCs) over traditional oxygen delivery methods. Inogen specializes in the development, manufacturing, and marketing of innovative POCs designed to deliver long-term supplemental oxygen therapy for patients with chronic respiratory conditions.

The company continues to demonstrate strong momentum in the POC market during the fourth-quarter, highlighted by over 20% year-over-year growth in its business-to-business (B2B) channel for the third consecutive quarter. This performance reflects growing recognition of Inogen’s solutions, particularly for their quality, ease of maintenance and extended service life. Per a report by Markets And Markets, the POCs market was valued at $15.05 billion in 2024 and is anticipated to reach $22.63 billion by 2029 at a CAGR of 8.5%.

Product Portfolio: We are encouraged by Inogen’s expanding product portfolio and its potential to drive future growth. In October 2024, the company launched Rove 4 — the lightest POC currently available in the market. The device delivers up to 840 milliliters of medical-grade oxygen per minute and offers a battery life of up to 5 hours and 45 minutes. Early adoption trends are promising, particularly in supporting earlier disease detection and potential patient upgrades.

Inogen anticipates that the Rove 4 will meaningfully contribute to revenue growth in 2025. Additionally, in December 2024, the company received FDA clearance to market Simeox in the United States, expanding its ability to meet the diverse needs of patients with chronic respiratory conditions.

Further strengthening its global presence, Inogen announced a strategic collaboration with Yuwell in January 2025. Yuwell is a leading global provider of home healthcare medical devices. The partnership is expected to expand Inogen’s product offerings through the U.S. and international distribution of select respiratory devices, support innovation via joint R&D initiatives and facilitate the company’s entry in the Chinese market.

Strong Q4 Results: Inogen delivered solid fourth-quarter results in February, reporting a 5.5% year-over-year increase in quarterly revenues. For full-year 2024, revenues reached $335.7 million, reflecting 6.4% growth over 2023. Adjusted gross profit for the fourth quarter rose 25.4% year over year to $39.3 million, with adjusted gross margin improving 777 basis points to 49.1%.

According to management, the revenue growth was primarily driven by increased demand and the addition of new customers across both domestic and international business-to-business channels. These gains were partially offset by softer performance in direct-to-consumer sales and rental revenues.

Seasonality Impact: The first quarter of 2025 is expected to reflect typical seasonal softness, particularly within the direct-to-consumer (DTC) channel. Management anticipates challenges in lead generation and heightened advertising headwinds during the period. Additionally, the DTC segment faced revenue pressure due to a leaner, more streamlined sales team — a factor that’s likely to have further impacted Inogen’s first-quarter performance.

Forex Volatility: International markets contribute a significant portion to Inogen’s overall revenues. However, management expects overseas sales to remain volatile in the near term, largely due to the varying size and timing of distributor orders. Additionally, unfavorable foreign exchange trends are projected to weigh on revenue growth, as the strengthening U.S. dollar continues to pressure conversions from the euro and other currencies. In the fourth quarter of 2024, adverse currency movements negatively impacted international sales by 330 basis points.

Inogen, Inc price | Inogen, Inc Quote

Inogen has been witnessing a positive estimate revision trend for 2025. In the past 60 days, the Zacks Consensus Estimate for its loss per share has narrowed 4.7% to $1.41.

The Zacks Consensus Estimate for 2025 revenues is pegged at $352.8 million, suggesting a 5.1% improvement from the year-ago reported number.

Some better-ranked stocks from the broader medical space are AngioDynamics ANGO, Veeva Systems VEEV and Masimo MASI, all sporting a Zacks Rank #1 (Strong Buy) at present.

AngioDynamics reported third-quarter fiscal 2025 adjusted earnings per share (EPS) of 3 cents against the Zacks Consensus Estimate of a loss of 13 cents. Revenues of $72 million beat the Zacks Consensus Estimate by 2%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

ANGO has an estimated fiscal 2026 earnings growth rate of 27.8% compared with the S&P 500 Composite’s 10.5%. The company beat on earnings in each of the trailing four quarters, the average surprise being 70.9%.

Veeva Systems posted fourth-quarter fiscal 2025 adjusted EPS of $1.75, which outpaced the Zacks Consensus Estimate by 10.1%. Revenues of $720.9 million surpassed the Zacks Consensus Estimate by 3.2%.

VEEV has an estimated long-term earnings growth rate of 26.6% compared with the industry’s 20.8%. The company’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 7.9%.

Masimo reported a fourth-quarter 2024 adjusted EPS of $1.80, which surpassed the Zacks Consensus Estimate by 20.8%. Revenues of $600.7 million topped the Zacks Consensus Estimate by 0.8%.

MASI has an estimated earnings yield of 3.5% for fiscal 2025 compared with the industry’s 3.6%. The company’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 14.4%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Jul-28 | |

| Jul-23 | |

| Jul-19 | |

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jun-30 | |

| Jun-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite