|

|

|

|

|||||

|

|

|

Oracle ORCL is scheduled to report its second-quarter fiscal 2026 results on Dec. 10.

For the second quarter of fiscal 2026, total revenues are expected to grow from 12% to 14% in constant currency (cc) and are expected to grow from 14% to 16% in dollar terms at current exchange rates.

The Zacks Consensus Estimate for revenues is currently pegged at $16.15 billion, suggesting growth of 14.84% from the year-ago quarter’s reported figure.

Non-GAAP earnings per share are expected to be in the range of $1.58-$1.62 in cc (representing 8-10% growth) and between $1.61 and $1.65 in USD (representing 10-12% growth).

The consensus mark for earnings is pegged at $1.63 per share, unchanged over the past 30 days. The figure indicates 10.88% growth from the year-ago period.

In the last reported quarter, Oracle delivered an earnings surprise of 0.00%. Markedly, the company’s earnings missed the Zacks Consensus Estimate in two of the trailing four quarters, while beating the same once and matching the same once, the average being 0.58%.

Our proven model does not conclusively predict an earnings beat for Oracle this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Oracle has an Earnings ESP of 0.00% and a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Oracle Corporation price-eps-surprise | Oracle Corporation Quote

Investors should consider holding the stock or waiting for a more favorable entry point ahead of the second quarter of fiscal 2026 results as the company navigates its aggressive AI infrastructure expansion amid market concerns over execution and leverage.

The quarter witnessed transformative developments that are likely to shape results. Oracle's landmark $300 billion, five-year cloud computing agreement with OpenAI, announced in September, positioned the company as a critical AI infrastructure provider. This contract significantly contributed to the 359% year-over-year surge in remaining performance obligations to $455 billion reported in the fiscal first quarter.

At Oracle AI World in October, the company unveiled Oracle AI Database 26ai and OCI Zettascale10, the largest AI supercomputer in the cloud, featuring hundreds of thousands of NVIDIA GPUs with 16 zettaFLOPS of peak performance. The partnership with Google Cloud was expanded, offering Gemini 2.5 models through the OCI Generative AI service. Additionally, Oracle introduced the AI Agent Marketplace with more than 600 AI agents bundled into Fusion Applications at no extra cost.

These strategic initiatives underscore Oracle's commitment to AI-driven cloud growth, though execution challenges and elevated capital expenditures projected at $35 billion for fiscal 2026 warrant cautious positioning ahead of earnings. Software revenue declines persist as cloud transitions continue. Increased debt levels exceeding $105 billion following an $18 billion bond issuance raised concerns about financial leverage.

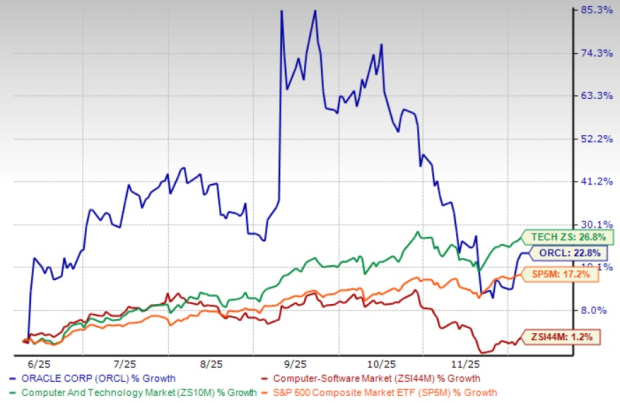

Shares of ORCL have gained 22.8% in the past six-month period compared with the Zacks Computer and Technology sector’s 26.8% return.

While Oracle has a strong foothold in the database management and ERP software markets, its competitors are making significant inroads in the cloud space. In terms of competitive positioning, Amazon AMZN maintains a strong lead in the market, though Microsoft MSFT and Alphabet GOOGL-owned Google continue to achieve higher growth rates. Amazon Web Services (“AWS”), Google Cloud and Microsoft combined had a 62% share of the global enterprise cloud infrastructure services market in third-quarter 2025, according to new data from Synergy Research Group.

It is also important to consider whether the stock's current valuation accurately reflects the company's long-term growth potential and ability to navigate the competitive landscape.

The stock currently trades at a price-to-earnings ratio of 29.31 times, above the Zacks Computer-Software industry average of 29.28 times and substantially elevated compared to Oracle's own five-year median of 22.38 times.

Oracle faces significant headwinds despite strong AI infrastructure momentum. The company trades at premium valuations while carrying more than $105 billion in debt following recent bond issuances. Capital expenditure requirements approaching $35 billion annually strain cash flows, with the fiscal first quarter generating negative free cash flow. Intense competition from hyperscalers AWS, Azure, and Google Cloud threatens market share expansion, while the $300 billion OpenAI contract won't materialize into revenues until 2027. Software revenue declines persist as cloud transitions continue. Elevated leverage, execution risks, and rich valuations suggest investors should await better entry points ahead of the second quarter of fiscal 2026 results.

Oracle's AI infrastructure transformation shows promise, but premium valuation amid execution risks suggests caution. Investors should consider waiting for better entry points ahead of the second-quarter fiscal 2026 results, particularly given intensifying competition from established hyperscalers and persistent balance sheet concerns.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 |

Dow Jones Futures: Market Triggers Sell Signal; Apple Earnings, Iran News, Fed Meeting In Focus

AMZN MSFT

Investor's Business Daily

|

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

What to watch next week: Big Tech earnings, the Fed, and Consumer Confidence

GOOGL MSFT

Yahoo Finance Video

|

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite