|

|

|

|

|||||

|

|

|

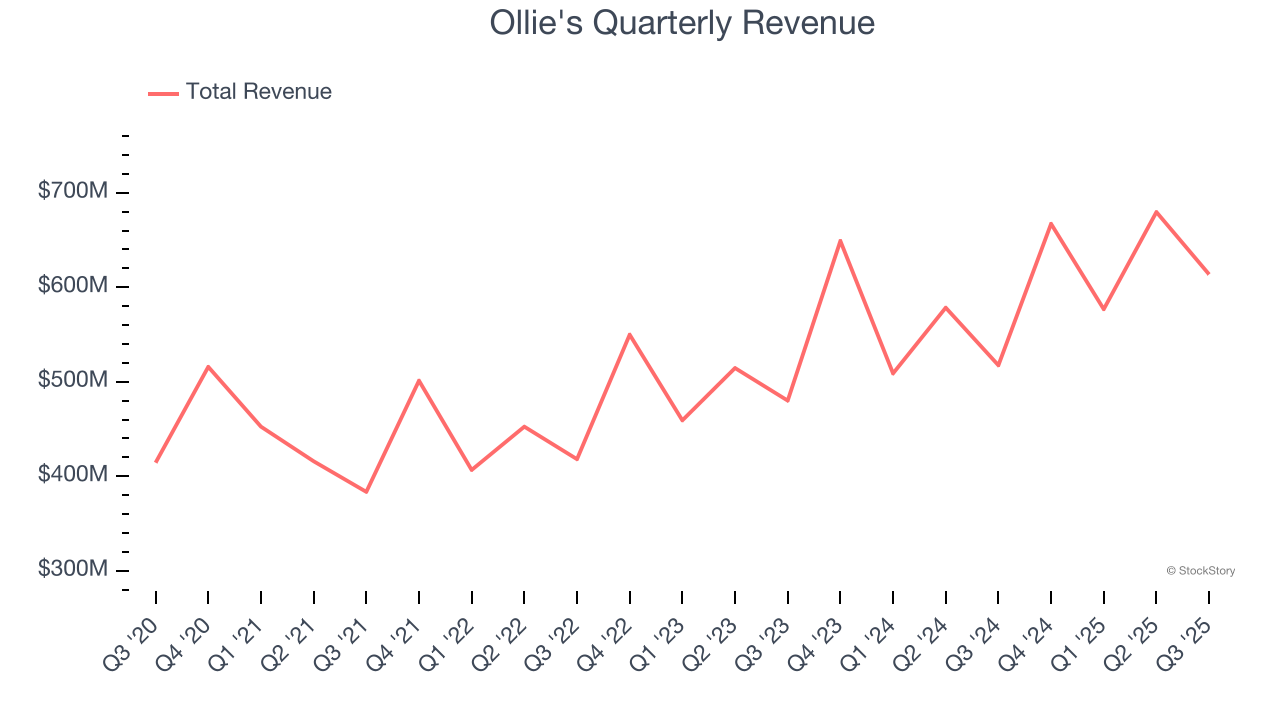

Discount retail company Ollie’s Bargain Outlet (NASDAQ:OLLI) met Wall Streets revenue expectations in Q3 CY2025, with sales up 18.6% year on year to $613.6 million. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $2.65 billion at the midpoint. Its non-GAAP profit of $0.75 per share was 2.4% above analysts’ consensus estimates.

Is now the time to buy Ollie's? Find out by accessing our full research report, it’s free for active Edge members.

“Thanks to the extraordinary execution of our team, we delivered another strong performance in the third quarter. We opened a record number of stores, continued to accelerate membership growth of our Ollie’s Army loyalty program, widened our price gaps to the fancy stores, and delivered industry-leading sales growth, all while driving significant improvement on the bottom-line,” said Eric van der Valk, President and Chief Executive Officer.

Often located in suburban or semi-rural shopping centers, Ollie’s Bargain Outlet (NASDAQ:OLLI) is a discount retailer that acquires excess inventory then sells at meaningful discounts.

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $2.54 billion in revenue over the past 12 months, Ollie's is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers. On the bright side, it can grow faster because it has more white space to build new stores.

As you can see below, Ollie's grew its sales at a solid 12.6% compounded annual growth rate over the last three years (we compare to 2019 to normalize for COVID-19 impacts) as it opened new stores and increased sales at existing, established locations.

This quarter, Ollie’s year-on-year revenue growth was 18.6%, and its $613.6 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 14% over the next 12 months, similar to its three-year rate. This projection is eye-popping and implies its newer products will fuel better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Ollie's operated 645 locations in the latest quarter. It has opened new stores at a rapid clip over the last two years, averaging 11.5% annual growth, much faster than the broader consumer retail sector. This gives it a chance to scale into a mid-sized business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

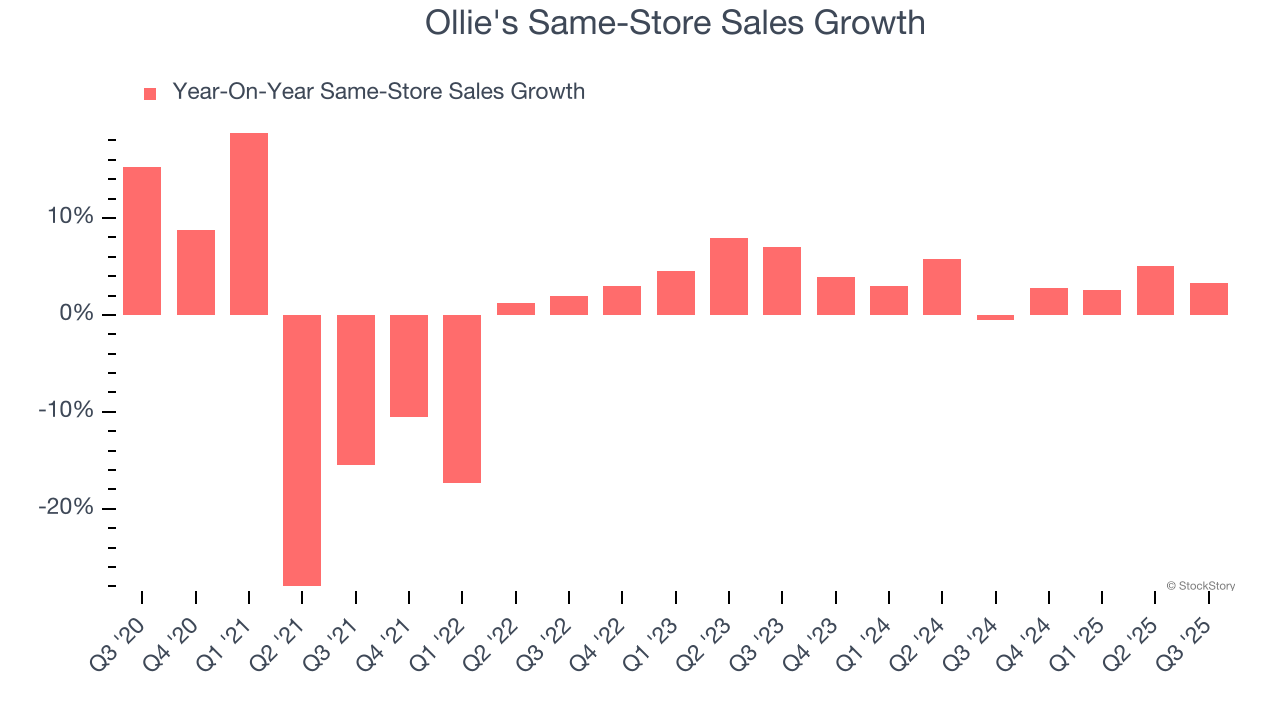

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Ollie’s demand has been spectacular for a retailer over the last two years. On average, the company has increased its same-store sales by an impressive 3.2% per year. This performance along with its meaningful buildout of new stores suggest it’s playing some aggressive offense.

In the latest quarter, Ollie’s same-store sales rose 3.3% year on year. This performance was more or less in line with its historical levels.

It was good to see Ollie's narrowly top analysts’ EBITDA expectations this quarter. We were also happy its gross margin narrowly outperformed Wall Street’s estimates.Zooming out, we think this was a decent quarter. The market seemed to be hoping for more, and the stock traded down 6.8% to $110.68 immediately following the results.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jul-08 | |

| Jul-08 | |

| Jun-04 | |

| Jun-03 | |

| Jun-03 | |

| Jun-03 | |

| Jun-03 | |

| Jun-03 | |

| Jun-03 | |

| Jun-03 | |

| Jun-03 | |

| Jun-01 | |

| May-14 | |

| Apr-02 | |

| Apr-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite