|

|

|

|

|||||

|

|

|

Walmart Inc.’s WMT International unit stood out as the company’s strongest engine of growth in the third quarter of fiscal 2026, offering a clear window into how its global momentum is taking shape as the next year approaches.

Net sales in the Walmart International segment witnessed 11.4% growth in constant currency to $33.7 billion, supported by broad-based strength across Flipkart, China and Walmex. Adjusted operating income also moved higher by 16.9%, reaching $1.4 billion, reflecting better e-commerce economics and a healthier business mix. Segment e-commerce sales advanced 26% in the quarter, driven by marketplace activities, and store-fulfilled pickup and delivery services, with a higher proportion of digital sales across markets.

The growth was backed by a combination of improvements that came together at the right time. Flipkart benefited from the Big Billion Days event shifting into the quarter, which helped push e-commerce volume sharply higher. That momentum also flowed into advertising, where Flipkart led a substantial lift in international ad revenues.

China added its solid contribution, with sales climbing to $6.1 billion, up 21.8% in constant currency. Digital penetration in China reached roughly half of sales, supported by extremely fast fulfillment speeds that aim to deliver most orders within about an hour.

Taken together, WMT’s third-quarter results show its International segment benefiting from scalable digital growth, rising advertising contributions and improving fulfillment productivity. Whether these same levers can deliver similar lift through fiscal 2026 will depend on timing, mix and one-off items that shaped this quarter’s performance.

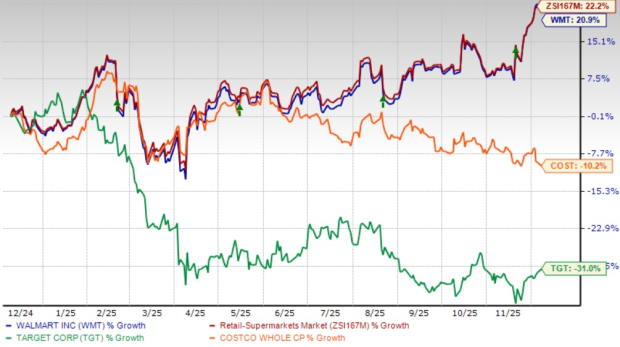

Walmart, which competes with Costco Wholesale Corporation COST and Target Corporation TGT, has seen its shares rally 20.9% in the past year compared with the industry’s growth of 22.2%. Shares of Costco have declined 10.2%, while Target tumbled 31% in the aforementioned period.

From a valuation standpoint, Walmart's forward 12-month price-to-earnings ratio stands at 39.83, higher than the industry’s 36.1. WMT carries a Value Score of C. Walmart is trading at a premium to Target (with a forward 12-month P/E ratio of 12.03) but at a discount to Costco (43.71).

The Zacks Consensus Estimate for Walmart’s current financial-year sales and earnings per share implies year-over-year growth of 4.5% and 4.8%, respectively.

Walmart currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite