|

|

|

|

|||||

|

|

|

Rigetti Computing RGTI has come under renewed pressure, with shares dipping 14.6% over the past month as investors react to a mix of technological progress and concerning execution setbacks. The company’s latest quarter delivered weaker revenues, sharply compressed margins and a notable miss on DARPA Phase B selection, developments that have added fresh uncertainty to a story already struggling to show commercial momentum. While Rigetti continues to outline an ambitious roadmap toward larger, higher-fidelity systems, the near-term results underscore just how difficult it remains for the company to translate engineering milestones into predictable financial performance.

At the same time, Rigetti is pushing ahead on several fronts, announcing new system sales, expanding R&D partnerships and reaffirming its multi-year hardware targets through 2027. These moves highlight that the company is still securing validation from government, academic and industry partners, even as its revenue base remains volatile and heavily contract-dependent. With the stock’s recent pullback and a growing divide between long-term promise and near-term execution, investors are now weighing whether Rigetti’s latest updates strengthen the case for patience or amplify the risks of staying invested.

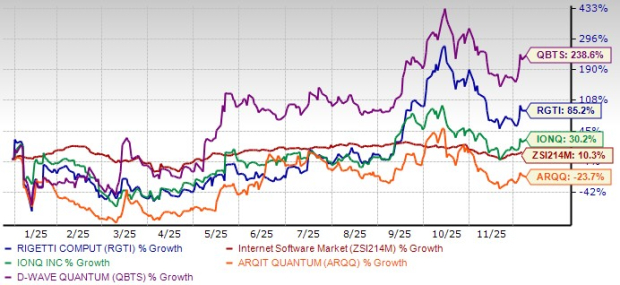

Rigetti’s recent pullback comes as competition in quantum computing accelerates. IonQ IONQ continues to advance its trapped-ion systems and expand commercial and government partnerships. Arqit Quantum ARQQ is pushing its quantum-safe encryption platform deeper into defense and telecom markets, carving out a security-focused niche. D-Wave Quantum QBTS is leaning into its annealing technology, targeting enterprise customers with practical optimization solutions. In this crowded environment, Rigetti’s chiplet-based roadmap and growing ecosystem partnerships remain differentiated, but the stock’s slide reflects rising investor caution around its near-term execution.

RGTI shares are up 85.2% year to date (YTD), placing the stock solidly ahead of most quantum peers but still far behind the category leader. QBTS has surged an exceptional 238.6%, reflecting far stronger investor momentum, and IONQ has risen 30.2%. In contrast, ARQQ has plunged 23.7%. The broader Zacks Internet – Software industry has gained 10.3% over the same period.

This divergence highlights that while Rigetti has delivered meaningful YTD gains, investors have rewarded competitors like QBTS far more aggressively, underscoring the market’s selective confidence and the elevated execution expectations placed on Rigetti as it advances its 2026–2027 roadmap.

Steady Contract Wins and Deepening Government Relationships: Despite near-term volatility, Rigetti continues to win meaningful government and research contracts that reinforce its role in foundational quantum development. The company secured a three-year, $5.8 million AFRL contract focused on superconducting quantum networking, a key step toward future networked quantum systems. This was accompanied by $5.7 million in purchase orders for two upgradable 9-qubit Novera on-premises systems, providing additional visibility into future revenue. While these programs won’t yield large-scale recurring enterprise revenue in the near term, they validate Rigetti’s technical capabilities and help support demand as U.S. federal quantum funding, including the reinstated National Quantum Initiative, begins to normalize.

Growing Global and Academic Ecosystem Momentum: Rigetti is strengthening its long-term positioning through international and academic collaborations that extend its footprint beyond near-term revenue cycles. The new MOU with India’s C-DAC ties Rigetti to a rapidly expanding, government-backed quantum ecosystem and opens doors for hybrid computing and co-development opportunities.

Montana State University has also installed a 9-qubit Novera system, marking the first academic on-premises Rigetti deployment and creating a pipeline for research partnerships and future upgrades. Combined with Rigetti’s integration into NVIDIA’s NVQLink hybrid platform, these alliances expand the company’s global relevance and reinforce strategic resilience as it works toward longer-term commercialization milestones.

Visible Progress on the Quantum Hardware Roadmap: On the technology side, Rigetti continues to push forward with its chiplet-based architecture, supported by strong performance data from its current 36-qubit system, which has demonstrated high two-qubit fidelity and solid gate speeds.

The company reiterated that it remains on track to unveil a 100+ qubit system with 99.5% median fidelity by the end of 2025, a key proving point for the scalability of its modular design. Rigetti then plans to deliver a 150+ qubit system with 99.7% fidelity in 2026, followed by a 1,000+ qubit system with 99.8% fidelity in 2027, enabled by a shift to larger 36-qubit chiplets.

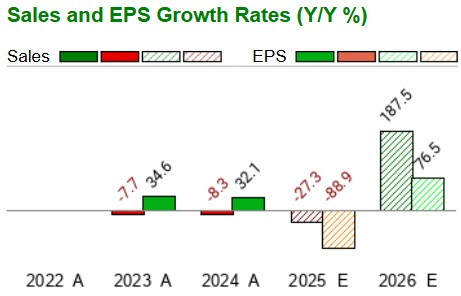

In 2025, Rigetti is expected to experience a 23.8% decline in revenues. On the profitability front, earnings per share are expected to remain negative, declining 88.9% year over year.

Weak Revenue Base, Margin Pressure, and Slow Commercial Uptake: Rigetti’s core challenge remains turning technical progress into steady, repeatable revenue, a weakness underscored by its third-quarter results. Revenues came in at $1.9 million, down 18% year over year, pressured by the lapse of National Quantum Initiative funding and the inconsistent timing of government contracts.

Gross margin fell to 21% from 51%, reflecting a lower-margin contract mix, while operating expenses rose to $21 million due to higher R&D spending, wage increases and stock-based compensation. With declining revenues, rising costs and tightening margins, Rigetti is still heavily reliant on government and research-driven projects rather than scalable commercial adoption.

Rigetti’s stock is not so cheap, as suggested by the Value Score of F.

RGTI is currently trading at a price-to-book (P/B) ratio of 24.72X, which is higher than the industry average of 6X.

Rigetti remains a compelling but high-risk player in the quantum computing landscape, offering a long-term technology story that continues to advance but a financial profile that has yet to stabilize. The company’s accelerating hardware roadmap, deepening government and academic partnerships, and growing involvement in hybrid quantum–AI ecosystems provide a credible foundation for future relevance. However, weak third-quarter revenues, sharp margin compression, rising operating costs and the setback in DARPA Phase B selection highlight the execution uncertainties that still define the near term.

With a Zacks Rank #3 (Hold), Rigetti appears better suited for investors willing to take a wait-and-see approach. The next leg of the RGTI story will hinge on whether the company can convert its 2025–2027 hardware milestones into enterprise adoption, higher-margin system deployments and more predictable revenue streams. For existing shareholders, maintaining a patient stance, rather than adding aggressively, may be the most balanced strategy as the company works to prove that its technological progress can translate into durable, recurring growth. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours |

Quantum Computing Stocks: D-Wave, AT&T Expand Quantum Agreement

QBTS +20.36%

Investor's Business Daily

|

| 7 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite