|

|

|

|

|||||

|

|

|

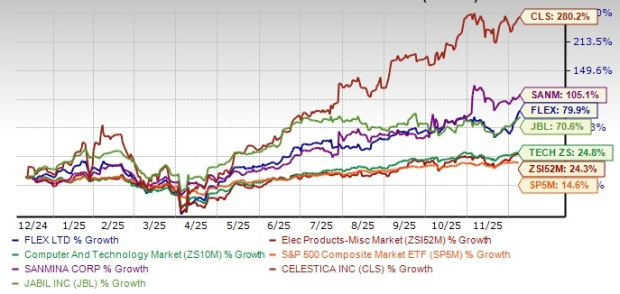

Flex Ltd. FLEX is having a breakout year, with the stock surging an impressive 79.9% in the past year. The stock hit a new 52-week high of $70.37 yesterday before closing at $68.50. The rally is buoyed by strong execution and a pivot toward higher-value, technology-intensive businesses.

The gains are better than outperforming the Zacks Electronics - Miscellaneous Products industry, the Zacks Computer and Technology sector and the S&P 500 composite’s growth of 24.3%, 24.8% and 14.6%, respectively.

Given this backdrop, the question for investors is straightforward: after a sharp rally, does Flex still offer compelling long-term upside?

Let us take a closer look at FLEX’s fundamentals, growth drivers, competitive advantages and potential risks, and assess whether it is still a buy?

Flex is positioned well for multi-year growth, supported by clear structural tailwinds and disciplined operational execution. In the second quarter of fiscal 2026, revenues increased 4% year over year to $6.8 billion.

Flex’s data center business is now its most powerful growth engine. Management emphasized that AI is driving one of the biggest infrastructure build-outs, and Flex is positioned at the center of it. Flex’s grid-to-chip approach is compelling as it integrates the product portfolio with advanced manufacturing capabilities and global scale.

It is working with leading technology companies to plan, build and deliver the power, cooling and systems infrastructure. This will facilitate swifter and more reliable data center deployments at scale.

A major catalyst in this acceleration is Flex’s introduction of a new AI infrastructure platform. Designed as a pre-engineered, scalable approach that integrates power, cooling and compute, the platform helps data center operators deploy up to 30% faster and lowers execution risk. Flex also deepened its relationship with NVIDIA by partnering on next-gen 800-volt DC AI factories, which offer higher energy efficiency, reduced cooling costs and higher reliability.

Recently, Flex announced a partnership with LG Electronics to co-develop integrated modular cooling systems designed to tackle the growing thermal challenges of AI-driven data centers.

With revenues expected to rise at least 35% this year, this segment is delivering not just rapid expansion but also significant mix benefits.

Though Power and cloud markets are the main focus right now, Flex’s diversified portfolio continues to support stability and incremental upside. The Health Solutions segment is witnessing “steady” medical device demand, with expectations for improved momentum in medical equipment. Optical switch and SATCOM demand are driving revenues from the Communications and enterprise segment.

Flex’s margin performance is also impressive. Non-GAAP gross margin expanded 80 basis points (bps) to 9.3% in the reported quarter. Non-GAAP operating margin expanded 55 bps to 6%.

Though the Automotive business remains soft, Flex noted relative stabilization and highlighted compute deals with new logos in software-defined vehicles in the fiscal first half.

The company posted a record $1.1 billion in free cash flow in fiscal 2025 and generated $305 million in adjusted free cash flow in the second quarter of fiscal 2026.

Management remains confident of achieving more than 80% free cash flow conversion for fiscal 2026. This strong cash generation supports share repurchases, M&A and continued investment in organic growth, strengthening Flex’s financial position and long-term growth.

In fiscal 2025, Flex repurchased stock worth $1.3 billion. In the second quarter of fiscal 2026, it repurchased $297 million worth of stock.

With 4% revenue growth in the first half and stronger demand expected in Power and Cloud in the fiscal fourth quarter, Flex has revised its fiscal 2026 revenue guidance to $26.7-$27.3 billion. It expects an adjusted operating margin of 6.2% to 6.3%. Flex now expects adjusted EPS of $3.09 to $3.17 for the fiscal year.

The company has incorporated the impact of tariffs into its revenue guidance, noting that tariffs remain largely a pass-through. Despite challenges from the Ukraine facility shutdown and unfavorable forex movement, the company remains confident in its growth outlook.

For the third quarter of fiscal 2026, Flex expects revenues to be between $6.65 billion and $6.95 billion.

Just not Flex, but other players in the electronics manufacturing services industry like Jabil JBL, Sanmina Corporation SANM and Celestica CLS are benefiting from the AI boom, sending the stocks soaring.

Jabil, Sanmina and Celestica have gained 70.6%, 105.1% and 280.2%, respectively.

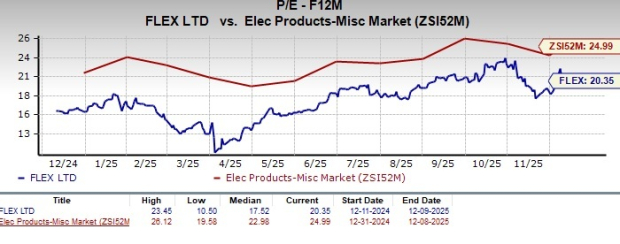

The stock trades at a forward 12-month price-to-earnings (P/E) ratio of 20.35, below the industry’s average of 24.99.

In comparison, Jabil, Sanmina and Celestica are trading at multiples of 19.64X, 16.45X and 42.36X, respectively.

With strong cash flow, disciplined execution, expanding margins and durability of its AI-driven growth story, Flex continues to offer attractive upside despite the stock’s substantial appreciation.

At present, FLEX carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite