|

|

|

|

|||||

|

|

|

Adobe’s ADBE fourth-quarter fiscal 2025 results reflected the benefits of the ongoing AI push that has been helping in advancing the company’s footprint among business, creative and marketing professionals. Adobe achieved more than 15% year-over-year growth in total monthly active users across solutions, including Acrobat, Creative Cloud, Express and Firefly in fiscal 2025. Adobe now targets annualized recurring revenue growth of 10.2% for fiscal 2026, driven by an innovative AI-powered portfolio, expanding adoption of enterprises and a large market opportunity.

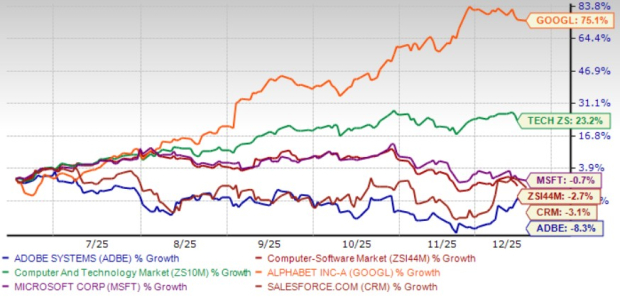

Nevertheless, Adobe suffers from stiff competition in the AI space from the likes of Microsoft MSFT, OpenAI, Alphabet GOOGL, Salesforce CRM, Midjourney, Canva and others. Microsoft’s Intelligent Cloud revenues are benefiting from growth in Azure AI services and a rise in the AI Copilot business. Alphabet’s focus on infusing AI heavily across its offerings, including Search and Google Cloud, has been a major growth driver. Salesforce’s strategy of continuous expansion of generative AI offerings is helping it tap growth opportunities. Adobe shares have dropped 8.3% in the past six months, underperforming Microsoft, Alphabet and Salesforce. While Alphabet shares have jumped 75.1%, Microsoft and Salesforce fell 0.7% and 3.1%, respectively. So, how should investors approach the Adobe stock? Let’s find out.

Adobe is benefiting from strong demand for AI-powered Creative Cloud Pro and Acrobat, as well as AI-first products, Firefly and Acrobat AI Assistant. An expanding partner base and integrations with leading AI ecosystems, including Amazon Web Services, Azure, Google Gemini, Microsoft CoPilot, OpenAI and others, are driving Adobe’s prospects.

Through the new conversational and agentic interfaces in Adobe Reader, Acrobat and Express, Adobe is offering improved experiences to business professionals and consumer groups. Adobe Express enhanced its features in the fiscal fourth quarter with the introduction of an AI Assistant capable of generative content creation and complex editing. Firefly models and applications like Photoshop, Illustrator and Premiere that integrate third-party models are gaining traction among Creators and Creative professionals. New solutions like Premiere mobile with YouTube integration and Photoshop mobile are helping creators develop content anywhere.

Adobe has been focusing on strengthening its footprint among marketing professionals through the Adobe Experience platform and apps that power customer engagement and loyalty. GenStudio is strengthening Adobe’s footprint among marketers. Adobe Experience Manager (AEM) and agentic web solutions, including LLM Optimizer, Sites Optimizer and Brand Concierge, are delivering brand visibility and discovery. The Semrush acquisition will enhance Adobe’s expanding portfolio of AI-driven customer experience solutions, including AEM, Adobe Analytics and Adobe Brand Concierge.

For the first quarter of fiscal 2026, Adobe expects revenues between $6.25 billion and $6.3 billion, while non-GAAP earnings are expected in the $5.85-$5.90 per share range.

Adobe now expects fiscal 2026 revenues between $25.9 billion and $26.1 billion. Fiscal 2026 non-GAAP earnings are now expected between $23.30 per share and $23.50 per share.

The Zacks Consensus Estimate for fiscal first quarter earnings is pegged at $5.73 per share, up 6 cents over the past 30 days, indicating 12.8% growth from the figure reported in the year-ago quarter. The consensus mark for revenues is currently pegged at $6.29 billion, suggesting 10% growth from the figure reported in the year-ago quarter.

Adobe Inc. price-consensus-chart | Adobe Inc. Quote

For fiscal 2026, the Zacks Consensus Estimate for revenues is currently pegged at $25.95 billion, suggesting 9.2% growth from fiscal 2025’s reported figure. The Zacks Consensus Estimate for earnings is pegged at $23.50 per share, down 7 cents over the past 30 days. The figure indicates 12.2% growth from fiscal 2025’s reported figure.

Meanwhile, Adobe has a Value Score of C, which suggests a stretched valuation. In terms of price/book, Adobe is trading at 12.65X higher than the broader sector’s 10.55X, Microsoft’s 9.72X, Alphabet’s 9.61X and Salesforce’s 3.97X.

Adobe’s focus on improving monetization of its AI-powered solutions is a positive for investors already holding the stock. However, a stretched valuation and stiff competition make the stock a risky bet in the near term.

ADBE currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 35 min | |

| 47 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite