|

|

|

|

|||||

|

|

|

Chewy, Inc.’s CHWY Autoship program is evolving as a key long-term growth driver, as reflected in its third-quarter fiscal 2025 results, which demonstrate the program's strong performance. Autoship generated $2.61 billion in sales, which accounted for 84% of total net sales. Autoship sales increased approximately 13.6% year over year, which surpassed the company’s overall net sales growth of 8.3%.

Management also noted that a strong Autoship baseline, with sponsored ads growth and a favorable category mix, supported gross margin expansion of 50 basis points year over year to 29.8% in the third quarter. Adjusted EBITDA increased 30% year over year to $180.9 million. The company ended the third quarter with 21.2 million active customers, which increased 5% year over year, with Net sales per active customer reaching $595, an increase of nearly 5% from the previous year.

Autoship also brings operational advantages that extend beyond top-line stability. With subscription-driven demand visibility, Chewy can better forecast inventory, optimize fulfillment center utilization and manage shipping density.

Additionally, Chewy’s paid membership program, Chewy+, continues to exceed expectations. Members enrolled in Chewy+ are demonstrating higher purchase frequency, deeper participation across product categories, increased usage of the mobile app, and greater adoption of Autoship compared with nonmembers. Following its initial rollout at $49 annually with a 30-day free trial, Chewy increased the membership fee to $79 toward the end of October. Early performance indicators suggest that demand has remained resilient despite the price increase, with conversion rates from trial to paid membership continuing to trend favorably. Gross margins from paid Chewy+ members are already in line with the company’s overall margin profile.

Autoship’s rising penetration, margin accretion, and integration with Chewy+ and health offerings reinforce its role as Chewy’s core growth engine. With improving customer quality, higher lifetime value and disciplined marketing, Autoship-driven flywheels position Chewy for durable, profitable long-term growth.

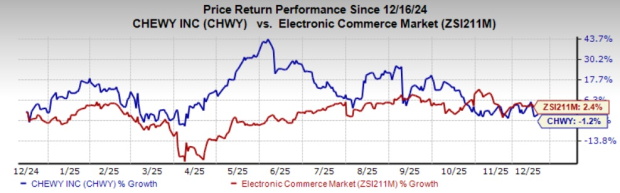

CHWY’s shares have lost 1.2% year to date against the industry’s rise of 2.4%. CHWY carries a Zacks Rank #3 (Hold).

From a valuation standpoint, CHWY trades at a forward price-to-earnings ratio of 21.73, lower than the industry’s average of 24.04.

The Zacks Consensus Estimate for earnings for the current and next fiscal year is pegged at $1.28 and $1.56 per share, respectively. These estimates indicate expected year-over-year growth rates of 23.1% and 22.1%, respectively.

Some better-ranked stocks have been discussed below:

American Eagle Outfitters, Inc. AEO operates as a multi-brand specialty retailer in the United States and internationally. At present, American Eagle sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for AEO’s current fiscal-year sales implies growth of 1.8% and earnings imply a decline of 25.3% from the year-ago figures. AEO delivered a trailing four-quarter earnings surprise of 35.1%, on average.

Boot Barn Holdings, Inc. BOOT operates specialty retail stores in the United States and internationally. At present, Boot Barn carries a Zacks Rank of 2 (Buy).

The Zacks Consensus Estimate for Boot Barn’s current fiscal-year sales and earnings implies growth of 16.2% and 20.5%, respectively, from the year-ago figures. BOOT delivered a trailing four-quarter earnings surprise of 5.4%, on average.

Amazon.com, Inc. AMZN engages in the retail sale of consumer products, advertising, and subscription services through online and physical stores in North America and internationally. At present, Amazon carries a Zacks Rank of 2.

The Zacks Consensus Estimate for Amazon’s current fiscal-year sales and earnings implies growth of 11.9% and 29.7%, respectively, from the year-ago figures. AMZN delivered a trailing four-quarter earnings surprise of 22.5%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 2 hours | |

| 3 hours | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite