|

|

|

|

|||||

|

|

|

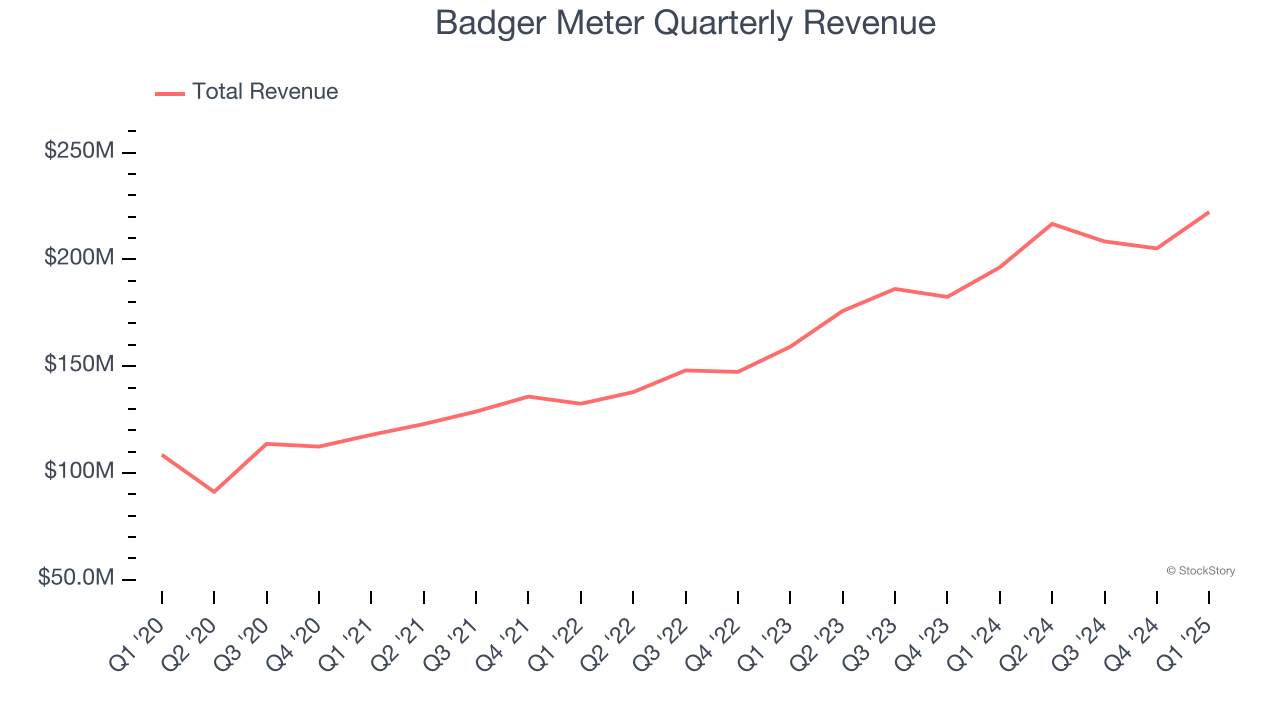

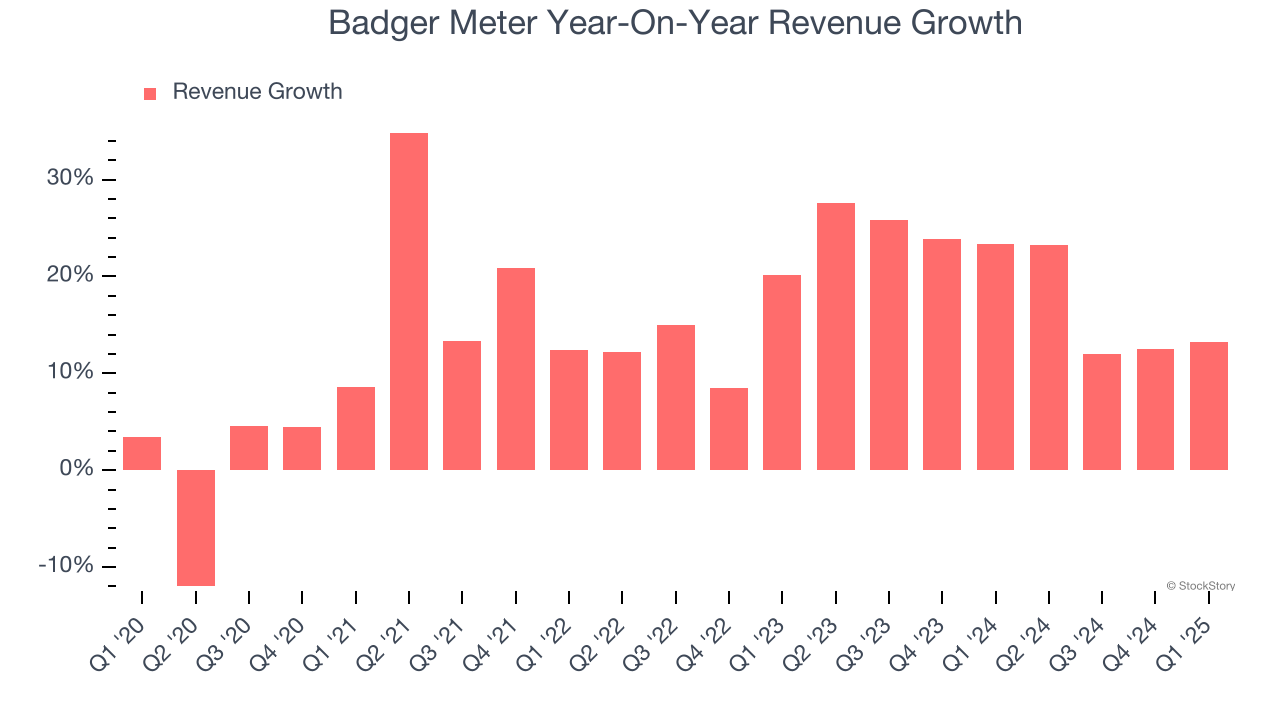

Water control and measure company Badger Meter (NYSE:BMI) met Wall Street’s revenue expectations in Q1 CY2025, with sales up 13.2% year on year to $222.2 million. Its GAAP profit of $1.30 per share was 26.4% above analysts’ consensus estimates.

Is now the time to buy Badger Meter? Find out by accessing our full research report, it’s free.

“Steady customer demand and disciplined operating execution drove solid revenue growth and record margins in a strong start to 2025. Our ability to build upon record results reflects the underlying stability of our business model as favorable industry fundamentals drive the need for our innovative smart water solutions,” said Kenneth C. Bockhorst, Chairman, President and Chief Executive Officer.

The developer of the world’s first frost-proof water meter in 1905, Badger Meter (NYSE:BMI) provides water control and measure equipment to various industries.

Measurement and inspection instrument companies may enjoy more steady demand because products such as water meters are non-discretionary and mandated for replacement at predictable intervals. In the last decade, digitization and data collection have driven innovation in the space, leading to incremental sales. But like the broader industrials sector, measurement and inspection instrument companies are at the whim of economic cycles. Interest rates, for example, can greatly impact civil, commercial, and residential construction projects that drive demand.

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Badger Meter’s sales grew at an exceptional 14.8% compounded annual growth rate over the last five years. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Badger Meter’s annualized revenue growth of 20% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Badger Meter’s year-on-year revenue growth was 13.2%, and its $222.2 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 11.7% over the next 12 months, a deceleration versus the last two years. Still, this projection is commendable and indicates the market is baking in success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

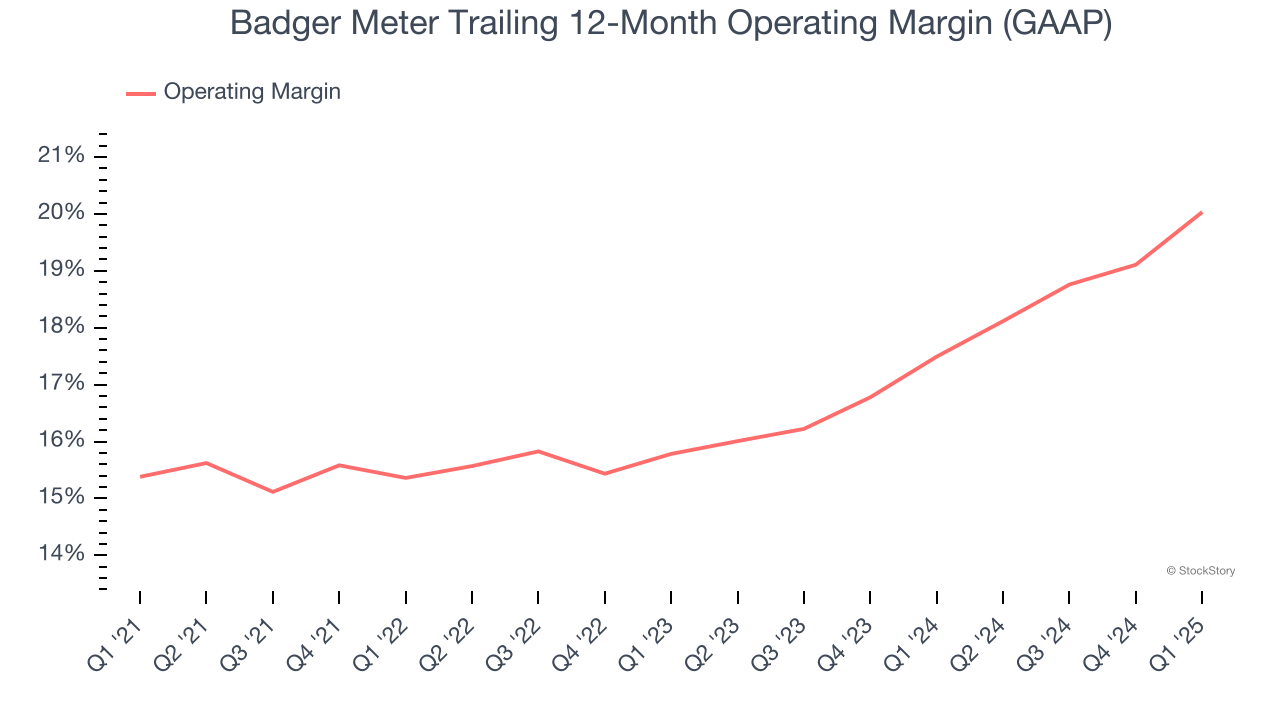

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Badger Meter has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 17.2%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Badger Meter’s operating margin rose by 4.7 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Badger Meter generated an operating profit margin of 22.2%, up 3.6 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

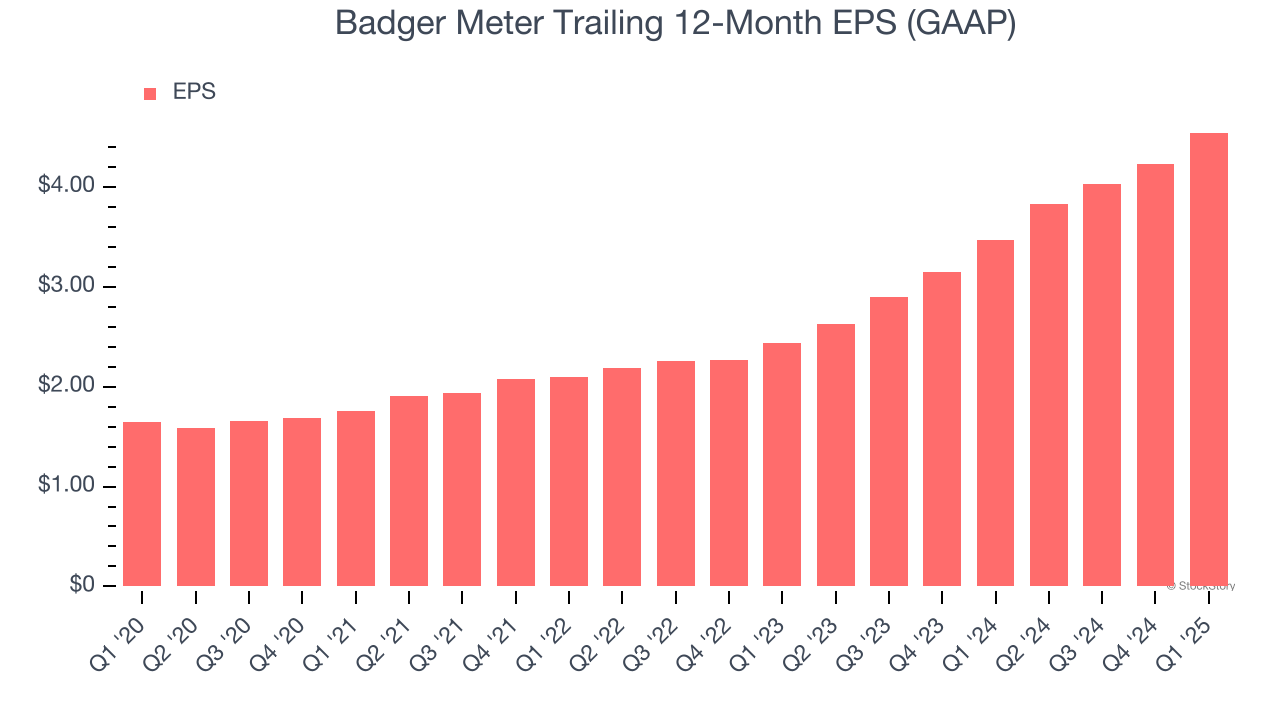

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Badger Meter’s EPS grew at an astounding 22.5% compounded annual growth rate over the last five years, higher than its 14.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into the nuances of Badger Meter’s earnings can give us a better understanding of its performance. As we mentioned earlier, Badger Meter’s operating margin expanded by 4.7 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Badger Meter, its two-year annual EPS growth of 36.6% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, Badger Meter reported EPS at $1.30, up from $0.99 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Badger Meter’s full-year EPS of $4.54 to grow 4.4%.

We were impressed by how significantly Badger Meter beat analysts’ EPS expectations this quarter despite just in-line revenue. It was also nice to see operating and free cash flow margin improve from the same quarter last year. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 1.1% to $186 immediately after reporting.

Badger Meter put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| 3 hours | |

| Feb-25 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-17 | |

| Feb-13 | |

| Feb-12 | |

| Feb-11 | |

| Feb-10 | |

| Feb-10 | |

| Feb-07 | |

| Feb-06 | |

| Feb-05 | |

| Feb-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite