|

|

|

|

|||||

|

|

|

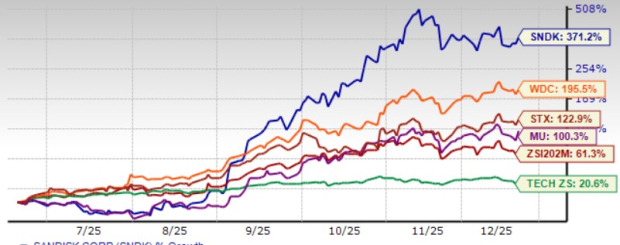

Sandisk SNDK shares have jumped 371.2% in the trailing six-month period, outperforming the Zacks Computer Storage industry’s return of 20.6% and the Zacks Computer and Technology sector’s appreciation of 20.6%. The company has outperformed its storage peers, including Western Digital WDC, Seagate STX and Micron Technology MU, over the same time frame, shares of which have returned 195.5%, 122.9% and 100.3%, respectively. Let us find out whether investors should buy the SNDK stock right now.

Sandisk, which was spun off from Western Digital in February, is expected to benefit from strong demand for NAND storage products that are capable of processing large volumes of data quickly and efficiently. In the first quarter of fiscal 2026, Sandisk’s BiCS8 technology accounted for 15% of total bits shipped and is expected to reach the majority of bit production exiting fiscal year 2026. Rapid growth of AI is creating a strong tailwind for SNDK’s high-capacity, power-efficient SSDs enabled by the BiCS8 technology. Investments in data centers and AI infrastructure are expected to surpass $1 trillion by 2030, which bodes well for Sandisk’s prospects.

BiCS8 technology is expected to boost Sandisk’s data center business, which reported revenues of $269 million in the first quarter of fiscal 2026, up 26% sequentially. Growing interest in the company’s technology from global hyperscalers, neocloud and OEM customers is noteworthy. Stargate — SNDK’s storage-focused SSD product line — is expected to gain traction among these customers.

This is expected to boost Sandisk’s competitive position against the likes of Western Digital, Seagate and Micron Technology. Sandisk competes against Western Digital, Seagate and Micron Technology in SSDs, HDDs, flash memory, as well as hybrid storage.

In the first quarter of fiscal 2026, edge revenues jumped 26% sequentially and 30% year over year to $1.39 billion. The business is benefiting from the ongoing PC refresh cycle, aided by Windows 11 adoption. PC unit shipments are expected to grow in the low single digits, with mid-single-digit growth in capacity per device in calendar years 2025 and 2026. The expanding infusion of generative AI in PCs and smartphones bodes well for Sandisk’s prospects. Average smartphone capacity per device is expected to grow in the high single digits in calendar years 2025 and 2026.

Sandisk expects continued momentum in edge as device upgrades accelerate, driving increasing NAND content. Moreover, strong demand for high-bandwidth flash (HBF) technology as customers across data centers and the edge seek higher performance AI inference capabilities. The partnership with SK Hynix is helping the company engage potential data center and edge customers for inference applications.

Moreover, Sandisk’s partnership with Nintendo is driving demand for the co-branded Switch 2 microSD Express Card, of which 900,000 units were sold in the fiscal first quarter. SNDK is expanding its presence in the handheld gaming sector with the new Sandisk microSD for ROG Xbox Ally, reinforcing its position in gaming storage. This is expected to drive consumer business, sales of which jumped 27% year over year and 11% sequentially to $652 million in the fiscal first quarter.

For the second quarter of fiscal 2026, Sandisk expects revenues between $2.55 billion and $2.65 billion. Earnings are expected between $3 and $3.40 per share.

The Zacks Consensus Estimate for second-quarter fiscal 2026 earnings is pegged at $3.25 per share, unchanged over the past 30 days. The consensus mark for second-quarter fiscal 2026 revenues is pegged at $2.62 billion.

Sandisk Corporation price-consensus-chart | Sandisk Corporation Quote

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $12.59 per share, up 3.1% over the past 30 days. Sandisk reported earnings of $2.99 per share for fiscal 2025. The consensus mark for fiscal 2026 revenues is pegged at $10.45 billion, suggesting 42.1% growth from fiscal 2025’s reported figure.

Sandisk shares are trading at a premium, as suggested by a Value Score of D.

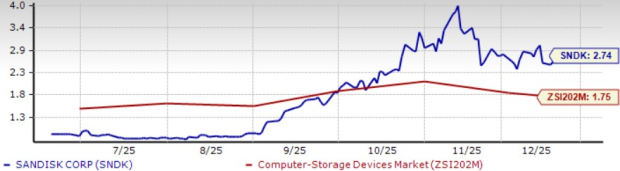

In terms of the forward 12-month price-to-sales (P/S), Sandisk is trading at 2.74X, higher than the industry’s 1.75X.

Sandisk is expected to benefit from strong demand for its BiCS8 technology, the ongoing PC refresh cycle and strong demand for HBF flash technology. These factors justify a premium valuation.

Sandisk currently has a Zacks Rank #2 (Buy) and a Growth Score of B, a favorable combination that offers a strong investment opportunity, per the Zacks Proprietary methodology. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite