|

|

|

|

|||||

|

|

|

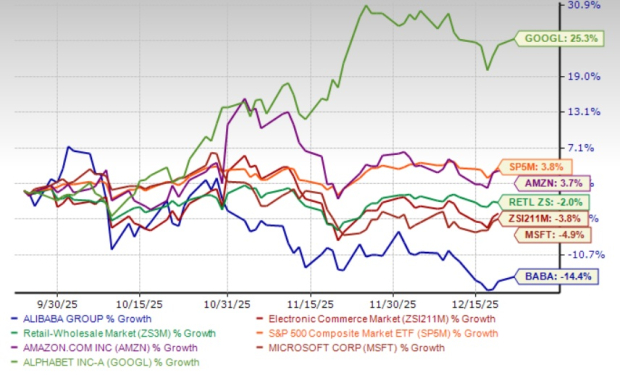

Alibaba Group BABA has experienced a turbulent quarter, with shares plunging 14.4% over the past three months as the Chinese e-commerce and cloud giant grapples with deteriorating profitability metrics despite revenue growth. The company's fiscal second-quarter 2026 results, released in November 2025, revealed a troubling disconnect between top-line expansion and bottom-line performance that has left investors questioning whether the current investment strategy justifies the pain. While management touts ambitious AI initiatives and cloud infrastructure buildouts, the immediate financial consequences paint a picture of a company sacrificing present profitability for an uncertain future.

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $6.48 per share, implying a 28.08% year-over-year decline.

Alibaba Group Holding Limited price-consensus-chart | Alibaba Group Holding Limited Quote

The fiscal second-quarter results exposed the severity of Alibaba's margin compression problem. While revenues reached RMB 247.8 billion, representing a modest 5% year-over-year increase that slightly exceeded the consensus estimate, the profitability metrics tell a far more concerning story. Non-GAAP diluted earnings collapsed 71% year over year to just RMB 4.36 per American Depositary Share, significantly undershooting the consensus estimate by 7.58%. This dramatic earnings miss reflects management's decision to prioritize aggressive capital deployment toward quick commerce expansion and AI infrastructure development over near-term financial discipline.

Income from operations plunged an alarming 85% year over year, falling from RMB 35.2 billion to a mere RMB 5.4 billion, while adjusted EBITA declined 78% over the same period. Operating margins contracted from 15% to just 2%, a compression that undermines the investment thesis even for the most patient long-term shareholders. The company's free cash flow situation deteriorated equally dramatically, swinging from a positive RMB 13.7 billion inflow to a RMB 21.8 billion outflow, primarily driven by capital-intensive investments in logistics infrastructure for instant delivery services and expanded cloud computing capacity.

Management has attempted to frame the quarter as a strategic investment phase, pointing to the 34% year-over-year growth in Cloud Intelligence Group revenues to RMB 39.8 billion as validation of its AI-first pivot. The company disclosed that AI-related products have now delivered triple-digit growth for nine consecutive quarters, with the Qwen AI assistant application surpassing 10 million downloads within its first week of public beta release. In December 2025, Alibaba announced the launch of its CosyVoice 3 multilingual speech synthesis model and significant upgrades to its AgentScope platform for enterprise AI agent deployment.

However, these developments, while technologically impressive, have yet to translate into sustainable profitability improvements. The cloud segment, despite its rapid expansion, remains insufficient to offset the margin deterioration across the broader business. China's core e-commerce operations continue facing intense competitive pressures from ByteDance's Douyin, PDD Holdings, and JD.com, forcing Alibaba to increase promotional spending and subsidize its quick commerce initiative to defend market share. The company's decision to invest RMB 120 billion in capital expenditures over the past four quarters demonstrates the scale of resources being redirected away from shareholder returns.

Alibaba's strategic repositioning from pure e-commerce dominance toward becoming a comprehensive technology and AI platform introduces significant execution risk that the current valuation fails to adequately discount. The massive capital requirements for AI infrastructure development threaten to extend the profitability drought well into future quarters.

The company's pursuit of Nvidia's H200 chips, contingent upon both U.S. export approvals and Chinese government authorization, highlights the geopolitical vulnerabilities embedded in its AI ambitions. December 2025 reports indicated Alibaba and other Chinese technology firms are seeking access to these advanced semiconductors, but regulatory uncertainties on both sides of the Pacific Ocean create meaningful timing and availability risks.

Alibaba's 14.4% decline over the past three months stands in stark contrast to the performance of global technology peers and the Zacks Retail-Wholesale sector, highlighting the company's relative weakness in investor perception.

The global cloud market exploded in the third quarter of 2025 to $107 billion, increasing $7.6 billion in just one quarter, as Amazon AMZN-owned Amazon Web Services (“AWS”), Microsoft MSFT and Alphabet GOOGL-owned Google Cloud continue to dominate global cloud market share. AWS, Google Cloud and Microsoft, combined, won 62% share of the global enterprise cloud infrastructure services market, according to new data from Synergy Research Group.

AWS maintains 29% of the global cloud infrastructure market with stronger margins, while Microsoft Azure commands a 20% share with robust enterprise relationships. Google Cloud has captured 13% with differentiated AI offerings. These competitors have managed to pursue AI opportunities while maintaining more disciplined financial profiles, making Alibaba's margin collapse particularly difficult to justify.

Alibaba's forward 12-month price-to-sales ratio of 2.28 times now trades at a notable premium compared to the broader Zacks Internet-Commerce industry average of 2.1 times. The stock's relative valuation demands that investors pay above-market multiples for a business experiencing severe margin compression, negative free cash flow generation, and intensifying competitive pressures in its core Chinese market.

The combination of collapsing profitability, massive capital expenditure requirements, uncertain AI monetization timelines, and premium valuation relative to industry peers suggests Alibaba shares face a challenging risk-reward profile for near-term investors. While the company's cloud business shows promise and its AI initiatives may eventually bear fruit, the immediate financial sacrifices are too severe to overlook. Investors would be well-advised to fold their positions and reallocate capital toward technology peers that have demonstrated better execution in balancing growth investments with current financial performance. BABA stock currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 |

Dow Jones Futures: Market Triggers Sell Signal; Apple Earnings, Iran News, Fed Meeting In Focus

AMZN MSFT

Investor's Business Daily

|

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

What to watch next week: Big Tech earnings, the Fed, and Consumer Confidence

GOOGL MSFT

Yahoo Finance Video

|

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite