|

|

|

|

|||||

|

|

|

Institutional activity has been mixed for Paychex, Inc. (NASDAQ: PAYX) over the last 12 months, with $6.38B of institutional inflows versus $5.17B of outflows, sending its price to a 52-week low in calendar Q4 2025. The move, triggered by growth concerns, found support near the lows later in the quarter, setting up an opportunity for value-oriented income investors. While downside risk remains, limiting factors—including still-positive growth, strong cash flow, capital returns, and shifting sentiment—are in place, and catalysts lie ahead. Growth concerns or not, the company posted 17% revenue growth in the quarter ended Aug. 31, 2025, and raised its full-year fiscal 2026 earnings outlook, supported by generally healthy labor market activity, which points to outperformance and capital return health in the upcoming quarters.

Insiders are worth checking alongside the mixed institutional flow. InsiderTrades.com’s last-12-months summary indicates no insider purchases, three insider sales, and approximately $16.46 million in insider selling, with insider ownership at about 0.80%. That doesn’t automatically mean management is negative—insiders sell for plenty of routine reasons, including preset plans or taxes tied to stock awards. Still, in a sell-off, investors often look for open-market insider buying as a show of confidence, and that hasn’t appeared in the recent window.

The key insight from the 2025 labor data is that while there was a slowdown, growth continues, with employment and wages on the rise and consumers remaining healthy. The most recent releases, including the weekly jobless claims figures, even suggest some stabilization at year’s end. Those trends may also be met by policy and rate tailwinds, including federal deductions tied to qualified tips and overtime that apply to the 2025 tax year (claimed when filing in 2026), alongside the potential for lower interest rates—factors that could help keep consumers spending and labor markets steady. The impact on Paychex will be a persistent demand for its services.

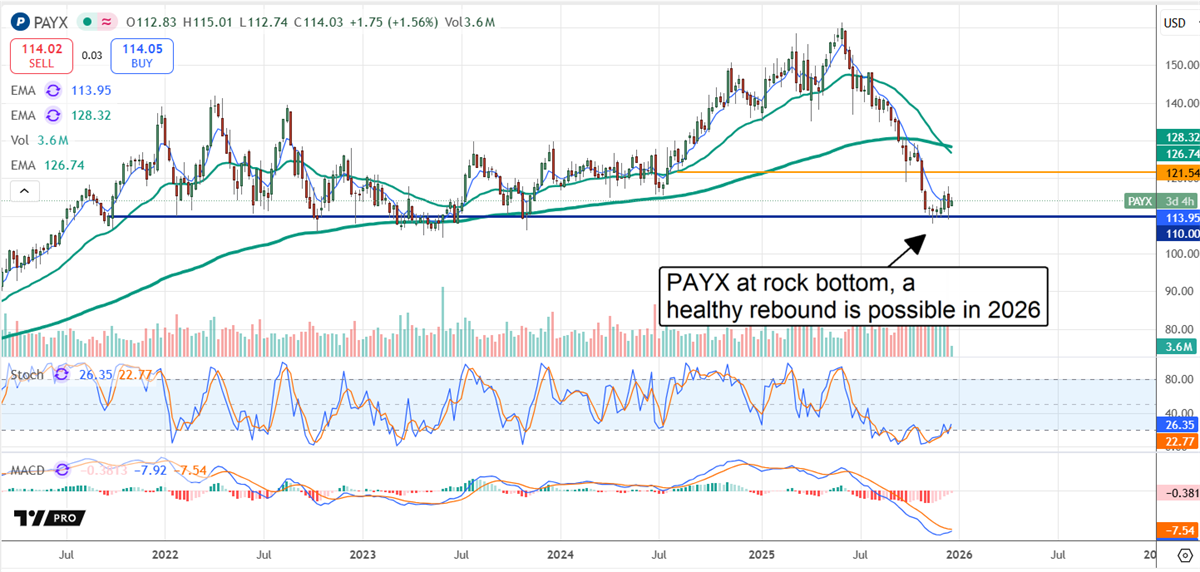

Analyst sentiment has been a headwind for PAYX stock in 2025, with downgrades and price target reductions reinforcing the downtrend. Even so, there are some constructive takeaways in the data. The first is that analysts limit downside in late 2025 as the low-end target of $110 aligns with a critical support target. The critical support target is the low end of a long-term trading range where a deep value is presented. Another bullish takeaway is the range of targets following the Q2 fiscal year 2026 (FY2026) release. It includes a low-end $110, but most align with the consensus, which points to low-double-digit upside for this high-yielding stock.

Considering its value, Paychex is not particularly inexpensive, with a valuation of around 21x its current-year earnings. However, it can be considered fairly valued relative to the average S&P 500 stock, which isn’t growing at a double-digit pace nor paying a dividend yielding 3.8%, and is deep value relative to its historical norms. Historically, this stock trades at an average of 28x its earnings, peaking out in the high-30s and bottoming in the high-teens. The 21x is a premium relative to the low but still a value relative to the average, suggesting a 25% upside potential.

The real value for PAYX investors is in the long term. Headwinds and growth concerns in 2025 are discounting future growth, which puts this stock at approximately 11x its 2035 forecasts. In this scenario, PAYX stock price could increase by as much as 100% over the coming years, and only needs a catalyst to spark a rebound. Between then and now, the 3.8% dividend yield is reliable, and the distribution is expected to increase annually. Share buybacks are also in the equation, reducing the count incrementally during the quarter.

Paychex has an AI catalyst in 2025. The company is rolling out new tools regularly, cementing it as a go-to source for small and medium-sized businesses that are becoming increasingly dependent on cloud-based services each quarter. Among Paychex’s benefits for its clients are automated HR tasks, data-driven insights, increased efficiency, and improved operational quality. The benefits to the business are enhanced demand for existing services and new revenue streams tied to premium products. Premium products include AI-enabled compliance tools that give clients an advantage over competitors and typically drive higher-than-average margins.

Price action suggests a potential floor near $110, but downside risk remains if fundamentals or guidance expectations weaken. Stochastic can be consistent with an oversold setup near support, and MACD may be starting to improve as selling pressure fades. If the stock is going to rebound, likely catalysts include early January labor-market data, rate expectations, and the next round of company updates that clarify growth and margin trends.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

The article "Paychex Is Out of Favor—And That’s the Opportunity" first appeared on MarketBeat.

| Jul-22 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-08 | |

| Jun-30 | |

| Jun-24 | |

| Jun-24 | |

| Jun-24 | |

| Jun-24 | |

| Jun-24 | |

| Jun-24 | |

| Jun-24 | |

| Jun-22 | |

| Jun-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite