|

|

|

|

|||||

|

|

|

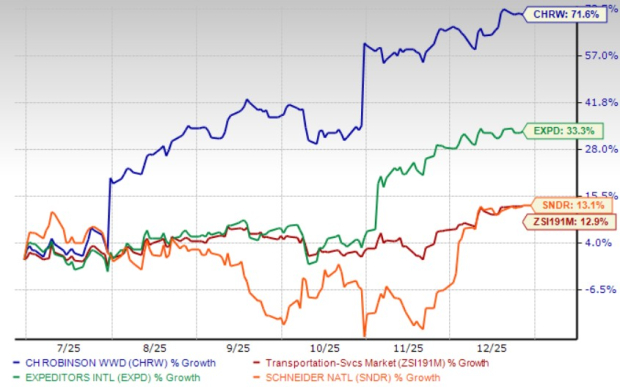

Shares of C.H. Robinson Worldwide, Inc. (CHRW) have had a good time on the bourses of late, improving in double-digits over the past six months. The encouraging price performance resulted in CHRW outperforming its transportation-services industry in the said time frame. Additionally, CHRW’s price performance looks favorable compared with that of other industry players like Expeditors International of Washington, Inc. (EXPD) and Schneider National, Inc. SNDR in the same timeframe.

Given the recent rally, the question that naturally arises is whether CHRW stock can sustain its bullish price performance or should investors book profits now. Before that, let's delve deep to unearth the reasons behind this northward price movement.

C.H. Robinson has been making uninterrupted dividend payments for more than 25 years. Highlighting its pro-investor stance, the board of directors(on Nov. 6, 2025) approved a dividend hike of 1.6%, thereby raising its quarterly cash dividend to 63 cents per share ($2.52 annualized) from 62 cents ($2.48 annualized). The raised dividend will be paid on Jan. 5, 2026, to shareholders of record at the close of business on Dec. 5, 2025. The move reflects CHRW’s intention to utilize free cash to enhance its shareholders’ returns.

C.H. Robinson Worldwide, Inc. dividend-yield-ttm | C.H. Robinson Worldwide, Inc. Quote

We would like to remind investors that CHRW has been consistently making efforts to reward its shareholders through dividends and share buybacks, which are encouraging. C.H. Robinson rewarded its shareholders in 2022 through a combination of cash dividends amounting to $285.32 million and share repurchases worth $1.45 billion. Continuing the shareholder-friendly approach, in 2023, CHRW paid $291.56 million in cash dividends and repurchased shares worth $63.88 million. During 2024, CHRW returned $294.77 million in the form of cash dividends (did not repurchase any shares). During the first nine months of 2025, CHRW returned $227.05 million in the form of cash dividends and $240.25 million through share repurchases. As of Nov. 5, 2025, CHRW had almost 118,403,777 shares outstanding.

A decrease in operating expensesaids C.H. Robinson’s bottom-line results. During the first nine months of 2025, operating expenses decreased 8.5% year over year to $1.5 billion. Personnel expenses fell 6.2% year over year to $1.0 billion, owing to cost optimization efforts and productivity improvements and the divestiture of our Europe Surface Transportation business. Average employee headcount declined 10.9%. Other SG&A expenses decreased 13.7% to $425.6 million, primarily due to a $57.0 million loss in the prior year related to the divestiture of our Europe Surface Transportation business.

CHRW’s AI integration drives real-time pricing, costing, and automation through a powerful mix of machine learning, large language models and autonomous agents.

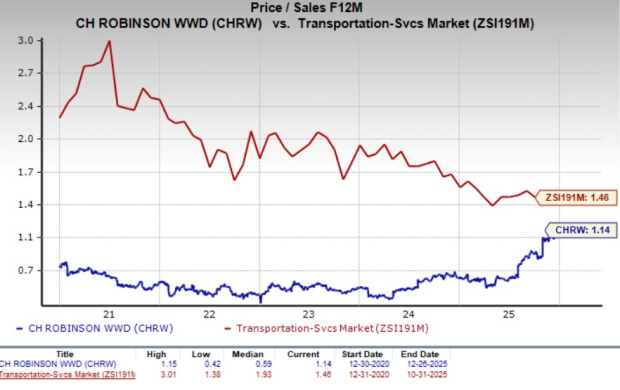

From a valuation perspective, CHRW is trading at a discount compared to the industry, going by its forward 12-month price-to-sales ratio.

The stock has a forward 12-month P/S-F12M of 1.14X compared with 1.46X for the industry over the past five years. These factors indicate that the stock’s valuation is attractive.

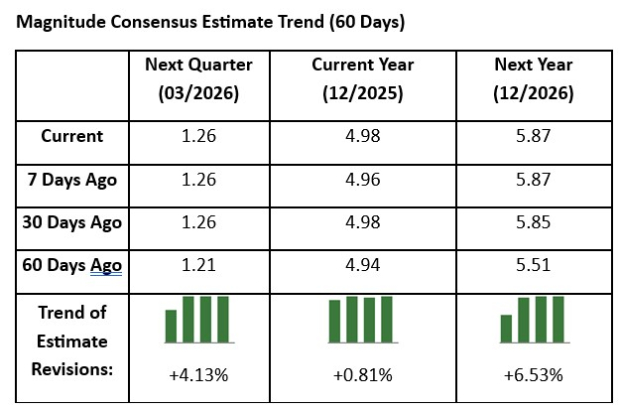

The positive sentiment surrounding the stock is evident from the fact that the Zacks Consensus Estimate for C.H. Robinson’s 2025 and 2026 earnings has been revised upward over the past 60 days. The consensus mark for first-quarter 2026 earnings has also been projected northward in the past 60 days.

The favorable estimate revisions indicate brokers’ confidence in the stock.

C.H. Robinson is being hurt by weak freight demand. The top line is being dented by lower pricing in its truckload services. The lower truckload pricing reflects an oversupply of truckload capacity compared to freight demand.

Moreover, CHRW's weak liquidity position is concerning. At the end of third-quarter 2025, the company’s cash and cash equivalents stood at $136.83 million, much lower than the long-term debt of $1.18 billion. This implies that the company does not have sufficient cash to meet its current debt obligations.

It is understood that CHRW stock is attractively valued and has been consistently rewarding its shareholders through dividend payouts and share buybacks. We believe such shareholder-friendly initiatives should boost investor confidence and positively impact the company’s bottom line. Despite these positives, we advise investors not to buy CHRW stock now due to headwinds like weak freight demand. CHRW's weak liquidity position is also concerning.

We advise investors to wait for a better entry point. For those who already own the stock, it will be prudent to stay invested. The company’s current Zacks Rank #3 (Hold) justifies our analysis. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-22 | |

| Jul-20 | |

| Jul-15 | |

| Jul-07 | |

| Jul-07 | |

| Jul-07 | |

| Jul-06 | |

| Jun-30 | |

| Jun-29 | |

| Jun-29 | |

| Jun-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite