|

|

|

|

|||||

|

|

|

Over the past six months, RLI’s shares (currently trading at $64.88) have posted a disappointing 10.2% loss, well below the S&P 500’s 11.7% gain. This may have investors wondering how to approach the situation.

Following the pullback, is now a good time to buy RLI? Find out in our full research report, it’s free for active Edge members.

Founded in 1965 and named after its original focus on "replacement lens insurance" for contact lens wearers, RLI (NYSE:RLI) is a specialty insurance company that underwrites property, casualty, and surety products through wholesale brokers, independent agents, and carrier partnerships.

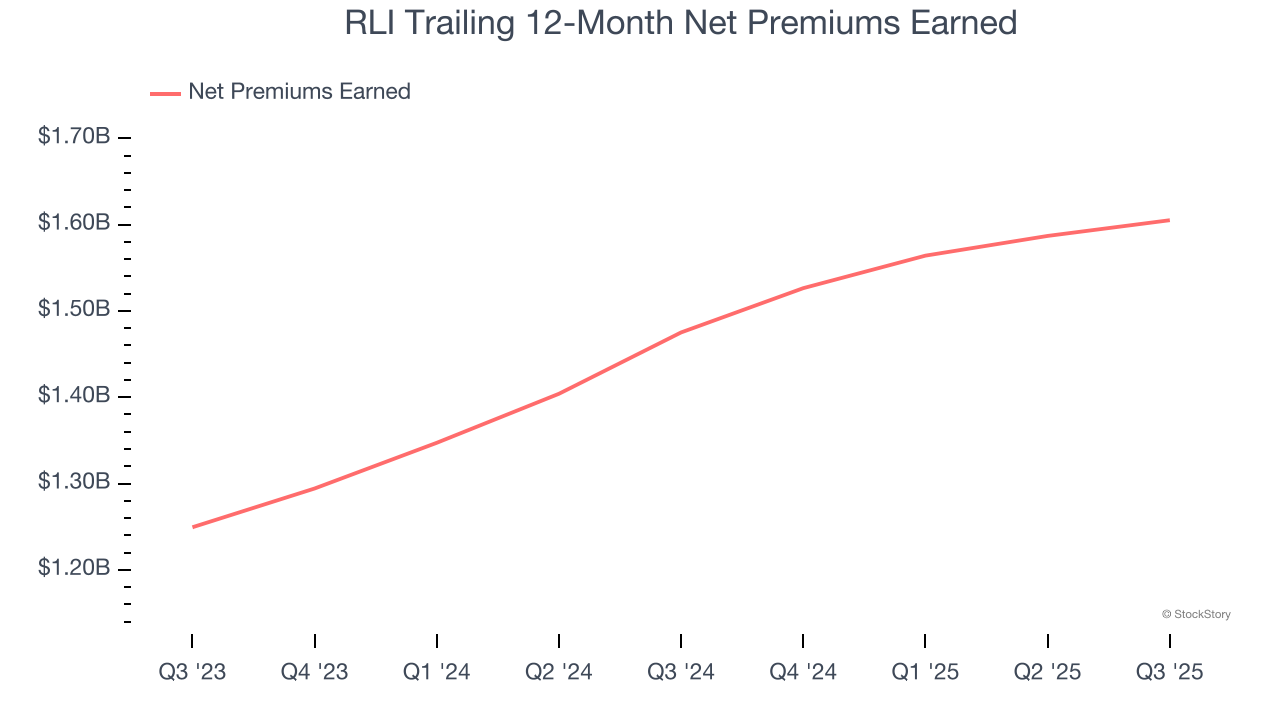

Insurers sell policies then use reinsurance (insurance for insurance companies) to protect themselves from large losses. Net premiums earned are therefore what's collected from selling policies less what’s paid to reinsurers as a risk mitigation tool.

RLI’s net premiums earned has grown at a 13.3% annualized rate over the last two years, better than the broader insurance industry and in line with its total revenue.

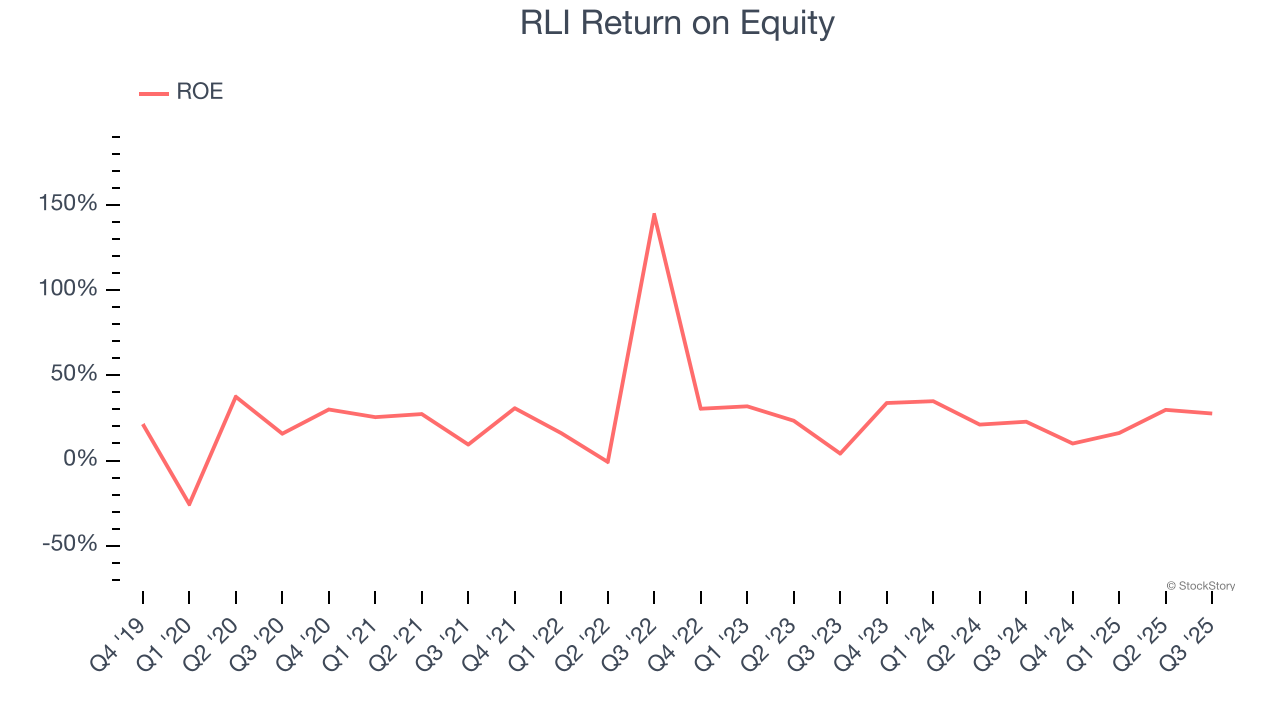

Return on equity (ROE) is a crucial yardstick for insurance companies, measuring their ability to generate returns on the capital provided by shareholders. Insurers that consistently deliver superior ROE tend to create more value for their investors over time through strategic capital allocation and shareholder-friendly policies.

Over the last five years, RLI has averaged an ROE of 28.4%, exceptional for a company operating in a sector where the average shakes out around 12.5% and those putting up 20%+ are greatly admired. This shows RLI has a strong competitive moat.

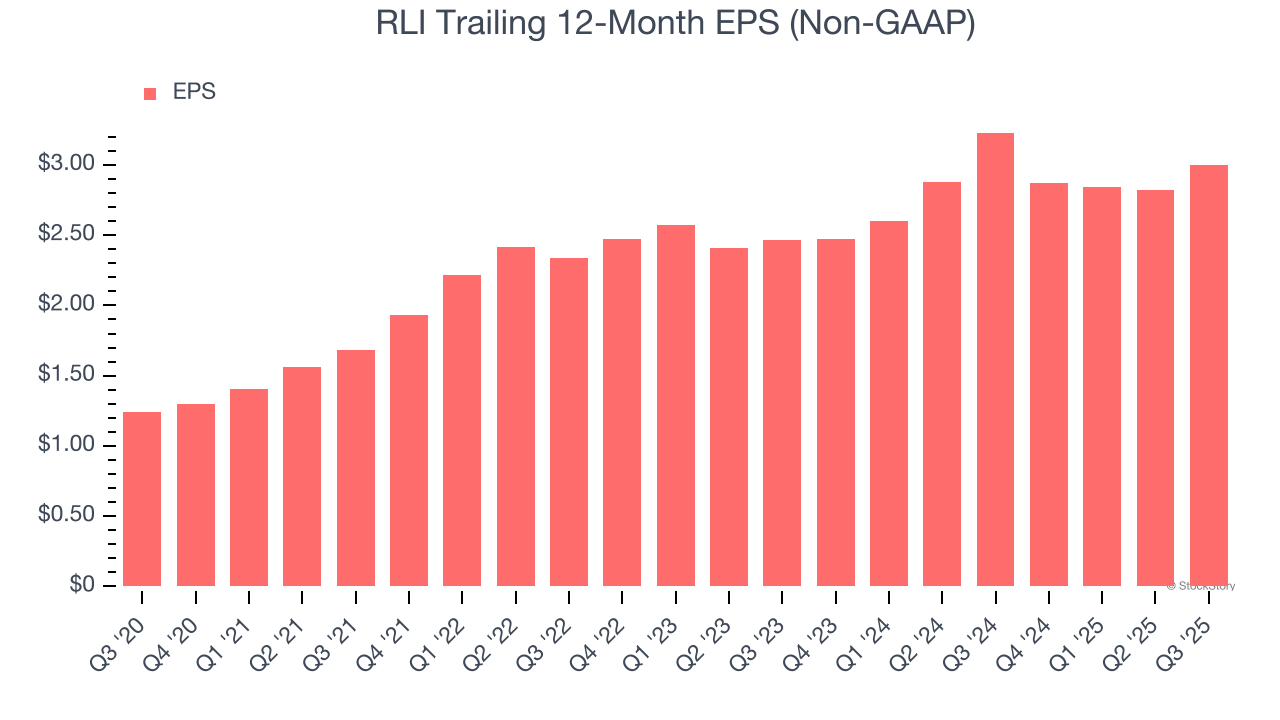

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

RLI’s EPS grew at a weak 10.3% compounded annual growth rate over the last two years, lower than its 13.6% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

RLI’s positive characteristics outweigh the negatives. After the recent drawdown, the stock trades at 3.3× forward P/B (or $64.88 per share). Is now a good time to initiate a position? See for yourself in our full research report, it’s free for active Edge members.

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-15 | |

| Jul-07 | |

| Jul-01 | |

| Jun-16 | |

| May-14 | |

| Apr-24 | |

| Apr-23 | |

| Apr-22 | |

| Apr-22 | |

| Mar-05 | |

| Mar-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite