|

|

|

|

|||||

|

|

|

CrowdStrike Holdings Inc. (NASDAQ: CRWD) stock is up 39% in 2025. It’s had a great year and outperformed the broader market. However, like many technology stocks, CrowdStrike stock has lost momentum in the last quarter of the year, down 6.6% in the final month. This is despite a strong earnings report in early December, in which it beat on both the top and bottom lines.

CrowdStrike is widely regarded as a “best in breed” stock in cybersecurity. The company has successfully pushed aside the bad vibes (and headlines) that came from the outage caused by a software glitch in July 2024. Since then, CRWD stock is up 115%.

However, it’s fair to wonder if CRWD stock will continue to be a tough trade in 2026. Even after the recent pullback, CrowdStrike trades at roughly 30x sales. That’s not unheard of for a top-tier cybersecurity stock, but it leaves very little margin for error.

At this valuation, CrowdStrike must not only continue to beat expectations, but it also needs to do so by a widening margin to drive further upside. A slowdown in revenue growth, even one caused by market conditions rather than execution, could pressure the stock.

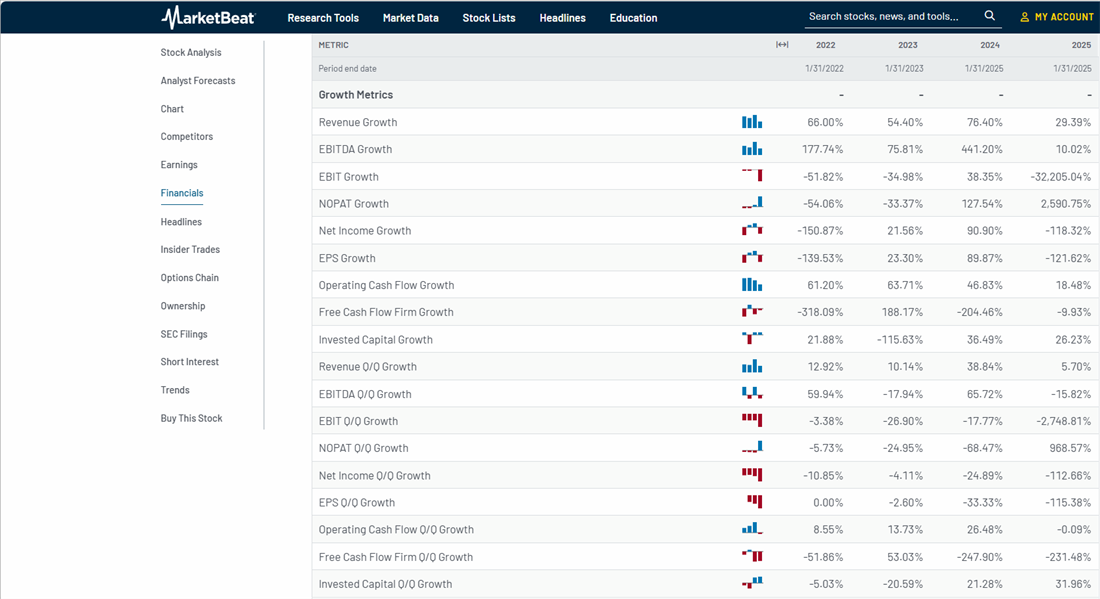

Revenue and annual recurring revenue (ARR) continue to grow, albeit at a measured pace rather than an explosive one. In its most recent quarter, revenue rose 21% year-over-year to $1.23 billion, and ARR climbed in the low 30% range, driven by multi-module adoption across the Falcon platform.

Those are outstanding metrics for a mature cybersecurity company. But they’re not the 40–60% growth rates that fueled previous multiple expansions.

There could be several reasons for this. The first one may seem counterintuitive. That is, operating leverage is starting to kick in. Adjusted operating margins have moved into the mid-20% range, and free cash flow continues to scale as more workloads consolidate on Falcon.

The underlying business is becoming more efficient. If CrowdStrike enters a “scale and optimize” era rather than a “hypergrowth at any cost” era, long-term investors could be rewarded. But valuation needs to compress, or earnings need to catch up to the stock price. Neither of those is a given.

That’s because of the second reason. Competitive pressure is another consideration. Microsoft’s Defender suite remains the biggest obstacle to pricing power, and Palo Alto Networks (NASDAQ: PANW) continues to bundle aggressively across cloud and endpoint.

Add a potential 2026 market environment that favors lower-multiple, cash-generating stocks as rates ease, and it’s fair to say CrowdStrike could be a tough trade in the first half of the year.

CrowdStrike enters 2026 in a corrective phase, trading near 474 and sitting below its 50‑day moving average but still above its 200‑day line, a sign of a pullback within a longer‑term uptrend.

With an RSI near 36 (not shown) and a negative MACD, the stock is mildly oversold. This creates a backdrop where oversold bounces are plausible even as short‑term momentum remains weak.

For active traders, this environment favors risk‑defined bullish strategies rather than outright shorting. The company’s options chain supports that for Jan. 9, 2026.

Short‑dated call spreads around the 470–495 range can target a rebound toward the declining 50‑day moving average, while limiting capital at risk. More cautious traders can use small, out‑of‑the‑money puts to hedge long stock or express a tactical bearish view, accepting a defined premium as the maximum loss.

Other ideas include:

CrowdStrike is still a best-in-breed among cybersecurity stocks. The Falcon platform remains one of the most comprehensive endpoint and cloud security ecosystems available. Furthermore, customer retention is strong, ARR is growing, and the balance sheet is in excellent shape.

None of that is in dispute. What is in dispute is whether investors should continue to pay a premium price for growth that’s gradually normalizing.

For long-term investors, CrowdStrike is still a name to watch and perhaps accumulate on deeper pullbacks. But for traders or valuation-sensitive investors, CRWD looks more like a Hold than a Buy heading into 2026. It’s a good company. It’s just a tough trade at today’s price.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

The article "CrowdStrike Is Still Best-in-Breed—But 2026 May Be a Tough Trade" first appeared on MarketBeat.

| Jul-20 | |

| Jul-20 | |

| Jul-19 | |

| Jul-19 | |

| Jul-18 | |

| Jul-18 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite