|

|

|

|

|||||

|

|

|

CoreWeave is experiencing tremendous growth due to nonstop demand for artificial intelligence (AI) data center capacity.

However, its means of funding its expansion doesn't appear sustainable.

Unless CoreWeave can demonstrate a path to positive cash profits, the stock may struggle to make new highs.

Cloud computing was already a massive growth trend as companies increasingly migrated from localized computing servers to renting computing power from companies operating massive data centers.

Now, artificial intelligence (AI) has accelerated this trend. Since AI primarily operates through the cloud, the AI boom is essentially turbocharging demand for cloud computing.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

It's very apparent in CoreWeave (NASDAQ: CRWV), one of the highest-profile IPO stocks of 2025. The company provides cloud-based GPU computing resources to AI hyperscalers and other companies that need turnkey access to high-end computing capacity.

Wall Street anticipates tremendous growth from CoreWeave in 2026. However, the stock has since slipped after its strong market debut earlier this year. Can CoreWeave grow enough to push the stock to new highs next year?

Image source: Getty Images.

Deep-pocketed technology giants, often referred to as hyperscalers, are all racing to expand their data center infrastructure to support widespread AI adoption. You could call it a race to corner the AI market, a potential multitrillion-dollar industry in the future.

Despite investing hundreds of billions of dollars cumulatively over the past several years, these AI companies continue to maintain that there isn't enough computing capacity to keep up with demand.

Enter CoreWeave.

Put simply, the company builds data center infrastructure purpose-built for AI workloads and sells the computing capacity. Microsoft, Meta Platforms, and International Business Machines (IBM) are among its customers. For them, working with CoreWeave is like taking a shortcut. Opting for turnkey data center capacity enables them to increase their computing resources more quickly, a crucial edge in this AI arms race.

Business is booming for CoreWeave. Analysts anticipate the business finishing the year at $5.1 billion in revenue, followed by $12 billion next year, more than double.

The stock only went public a few months ago, so it's likely to be somewhat volatile, given its status as one of the headline IPOs of 2025. Often, a highly hyped IPO stock will surge shortly after it begins trading, only to decline once the initial excitement subsides.

It seems CoreWeave is an example of that. The stock reached its high within weeks of its debut.

There is a deeper explanation, though. While it's common for a fast-growing company to forgo profits in the name of revenue growth, CoreWeave's path to grow presents some red flags.

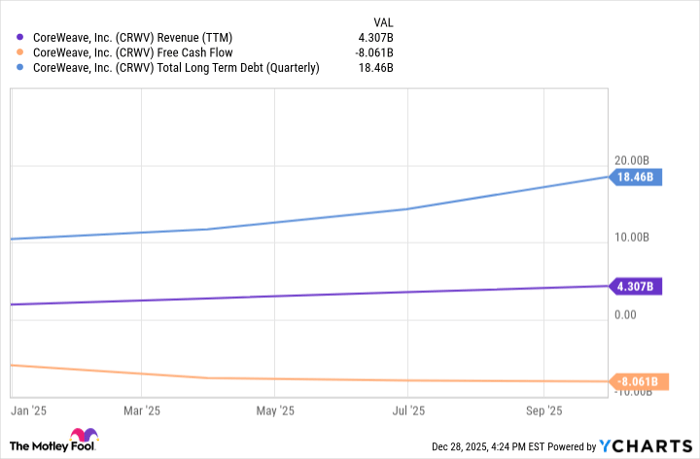

CoreWeave is aggressively investing in GPU chips and other hardware to increase its data center capacity; the company can't grow without any capacity to sell. The company has already borrowed a substantial amount of money to fund this, nearly $18.5 billion in long-term debt.

CRWV Revenue (TTM) data by YCharts

At the same time, CoreWeave is still deeply unprofitable from a cash flow standpoint. Its free cash flow is -$8 billion over the past four quarters alone. Therefore, the company must continue to borrow or issue more stock to fund its growth.

As impressive as CoreWeave's anticipated revenue growth will be, it comes with some crucial caveats.

Investors may look to CoreWeave for a path to profitability. The company can't borrow forever without imploding, and continuously issuing stock will dilute shareholders, thereby reducing the stock's upside.

Does CoreWeave genuinely have the pricing power to turn profitable without stopping its growth? Only time will tell. What if AI hyperscalers, many of which are CoreWeave's customers, pull back on data center spending altogether? How easily could CoreWeave sell its data center capacity if the momentum for AI investments slows?

These questions don't have immediate answers, but they highlight the various risks that could affect the company and its stock.

If CoreWeave hits next year's revenue estimates, it could be enough raw revenue growth to buoy the stock price and prevent further declines. However, the stock needs strong sentiment to rally back from a nearly 60% decline and hit new highs. Investors may require more evidence that CoreWeave's core business is financially sustainable before doing so.

Before you buy stock in CoreWeave, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CoreWeave wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $505,641!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,143,283!*

Now, it’s worth noting Stock Advisor’s total average return is 974% — a market-crushing outperformance compared to 193% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 1, 2026.

Justin Pope has positions in Microsoft. The Motley Fool has positions in and recommends International Business Machines, Meta Platforms, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| Aug-08 | |

| Aug-07 |

Berkshire Hathaway earnings, CPI inflation data, & more: What to Watch

CRWV +6.26%

Yahoo Finance Video

|

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Jane Street Eyes $11 Billion Private Credit Refinance to Support AI Investments: Report

CRWV +6.26%

Benzinga Private Markets

|

| Aug-06 |

CoreWeave Stock, Nebius Highlight Data Center Earnings; Tech Stars Lumentum, AMAT Also Due

CRWV -5.07%

Investor's Business Daily

|

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite