|

|

|

|

|||||

|

|

|

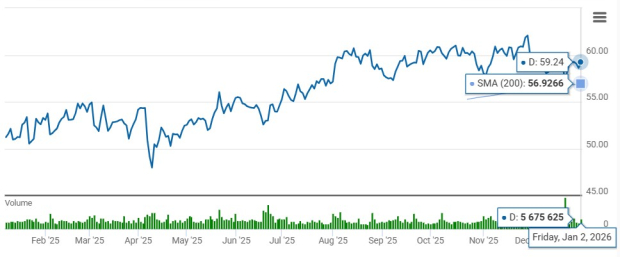

Dominion Energy D trading above its 200-day SMA signals a bullish momentum. The company’s continued investments in electric and natural gas infrastructure, coupled with a growing focus on renewable energy, underpin its growth outlook. Solid contributions from organic assets and rising demand from an expanding customer base further enhance prospects.

Dominion Energy has a well-chalked-out long-term capital expenditure plan to strengthen and expand its infrastructure. Organic projects and acquired assets will further expand the company’s clean energy portfolio.

The 200-day SMA is a key indicator for traders and analysts to identify support and resistance levels. It is considered particularly important as this is the first marker of a stock’s uptrend or downtrend.

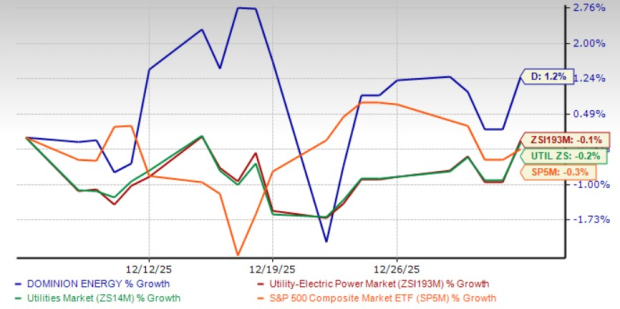

In the past month, the company’s shares have gained 1.2% against the Zacks Utility- Electric Power industry’s 0.1% decline. In the same time period, the S&P 500 and the Zacks Utilities sector declined 0.3% and 0.2%, respectively.

Should Dominion Energy be added to your portfolio purely on the back of recent price strength? Let’s dive deeper into the key factors that can help investors evaluate whether now is the right time to buy D stock.

Dominion Energy’s strategic portfolio realignment highlights its increased focus on regulated assets, reflected in ongoing investments in regulated infrastructure that support long-term operational growth. As part of this strategy, the company has divested select merchant generation assets and its electric retail energy marketing business to focus on core operations.

Dominion Energy has a well-chalked-out long-term capital expenditure plan to strengthen and expand its infrastructure. The company has planned to invest nearly $50 billion in the 2025-2029 period to further strengthen its operations. Dominion Energy’s long-term objective is to have more battery storage, solar, hydro and wind projects by 2036 and increase the renewable energy capacity by more than 15% per year, on average, over the next 15 years.

D continues to experience customer growth across its service areas in Virginia and South Carolina. The company’s utility rates are lower than the national average and its reliable services attract more customers and boost demand.

Dominion Energy is witnessing strong commercial load growth driven by rising demand from data centers. Since 2013, the company has added an average of 15 data centers annually. In the first nine months of 2025 alone, Dominion Energy added nearly 7.1 GW of capacity and continues to see robust data center-related demand.

Dominion Energy is undertaking a $2 billion initiative to underground 4,000 miles of its most outage-prone overhead distribution lines. The company has already completed more than 2,500 miles in Virginia, reducing average outage durations for affected customers from 11 hours to just 2 minutes. These efforts are strengthening system resilience and enhancing Dominion Energy’s ability to reliably and efficiently serve a growing customer base.

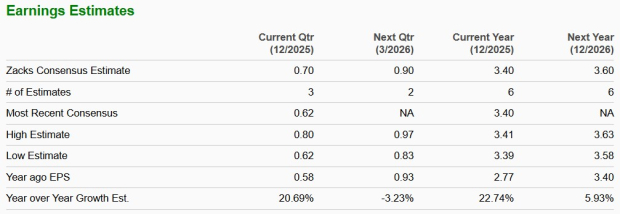

The Zacks Consensus Estimate for D’s 2026 earnings per share indicates a year-over-year increase of 5.93%. Long-term earnings (three to five years) growth is pegged at 10.26%.

NextEra Energy NEE is another large operator in this space and has the capacity to produce a huge volume of clean electricity for its customers. NEE is investing systematically to further expand its clean energy generation capacity.

The Zacks Consensus Estimate for NEE’s 2026 earnings per share indicates a year-over-year increase of 8.25%. Long-term earnings (three to five years) growth is pegged at 8.08%.

The company has been distributing dividends to its shareholders for a long time. The current annual dividend of the company is $2.67. The current dividend yield of 4.51% is better than the industry’s yield of 2.92%. Check D’s dividend history here.

Another utility, The Southern Company SO, also rewards its shareholders through the payment of dividends at regular intervals. SO’s current annual dividend is pegged at $2.96 per share and its current dividend yield of 3.4% is better than the industry.

Utility operations are capital-intensive and the companies operating in this space need to borrow funds, as the internally generated funds are always enough to meet long-term capital requirements. The decline in the interest rate to the 3.5-3.75% range is beneficial for the utilities as it will reduce long-term project costs.

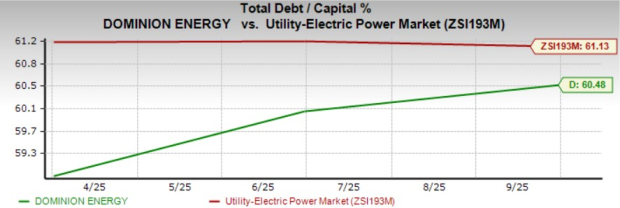

Dominion Energy’s debt to capital is 60.48%, which is lower than the industry’s average of 61.13%. This indicates that the company is utilizing lower debts compared with the industry peers to run its operations.

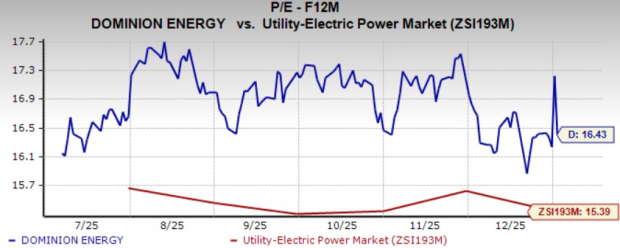

Dominion Energy is currently valued at a premium compared with its industry on a forward 12-month P/E basis.

Dominion Energy’s disciplined investments in expanding clean energy generation and reinforcing its grid infrastructure should enhance service reliability for customers. Growing demand for clean energy remains a favorable long-term tailwind for the company.

Yet, the stock’s valuation appears elevated relative to industry peers, which warrants caution. Investors who already hold this Zacks Rank #3 (Hold) stock may consider retaining it to benefit from steady dividend income, while prospective investors could wait for a more attractive entry point.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-20 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite