|

|

|

|

|||||

|

|

|

Visa Inc. V remains a key player in the digital payments landscape, even as fintech innovations and alternative payment options are on the rise. The main reason lies in the company’s network size and its deep integration with consumers, merchants, banks and governments around the world. As digital payments evolve across cards, wallets and e-commerce, Visa remains a common backbone.

Unlike many fintech companies that focus on specific use cases, Visa benefits from operating as a core payments infrastructure. Its transaction-based model generates revenues from payment volumes without lending money or taking credit risks, which helps the business remain resilient across economic cycles. As digital payments continue to grow, the company captures growth through increased transaction volumes, a favorable spending mix and rising cross-border transactions. In fiscal 2025, Visa’s payment volume witnessed 8% year-over-year growth.

Another factor keeping Visa at the center is its continued investment in value-added services. Beyond just processing payments, the company is ramping up its efforts in areas like fraud prevention, data analytics, tokenization and real-time payments. These initiatives not only help diversify revenue streams but also make its network essential for clients who are navigating the fast-changing world of payments.

The shift away from cash remains a long-term structural tailwind, with emerging markets, small businesses and underpenetrated digital use cases increasingly adopting electronic payments, expanding Visa’s addressable market. Its secure, global network, efficient business model and consistent performance keep it central to digital commerce, allowing it to benefit from, rather than be disrupted by, change.

Some of V’s competitors in the digital payments space include Mastercard Incorporated MA and American Express Company AXP.

Mastercard continues to expand its global footprint, benefiting from rising digital payment adoption and cross-border activity. Like Visa, MA earns from transaction volumes and invests in value-added services. Mastercard’s payment network net revenues increased 13% year over year in the first nine months of 2025.

American Express is banking on its upscale clientele, the rebound in travel demand and increased card spending to drive its growth. Its total revenues (net of interest expense) rose 9% year over year in the first nine months of 2025. American Express reported 7% year-over-year growth in its network volumes in the same period.

Over the past year, shares of Visa have jumped 10.7% against the 8.4% fall of the industry.

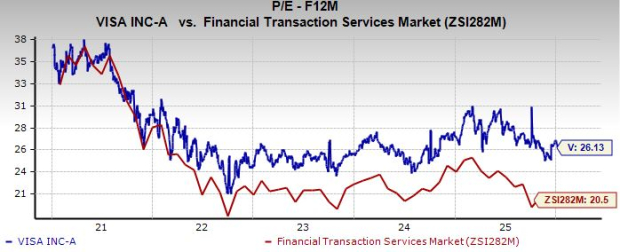

From a valuation standpoint, V trades at a forward price-to-earnings ratio of 26.13, above the industry average of 20.50. V carries a Value Score of D.

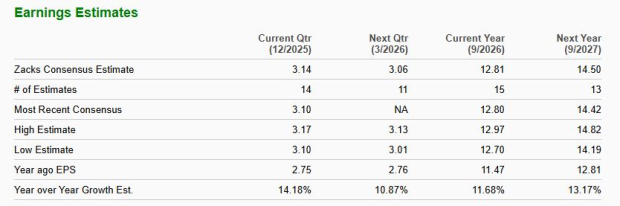

The Zacks Consensus Estimate for Visa’s fiscal 2026 earnings implies an 11.7% jump from the year-ago period.

Visa stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite