|

|

|

|

|||||

|

|

|

Over the past six months, Vail Resorts’s stock price fell to $134.59. Shareholders have lost 17.4% of their capital, which is disappointing considering the S&P 500 has climbed by 10.1%. This might have investors contemplating their next move.

Is now the time to buy Vail Resorts, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free for active Edge members.

Even though the stock has become cheaper, we're cautious about Vail Resorts. Here are three reasons we avoid MTN and a stock we'd rather own.

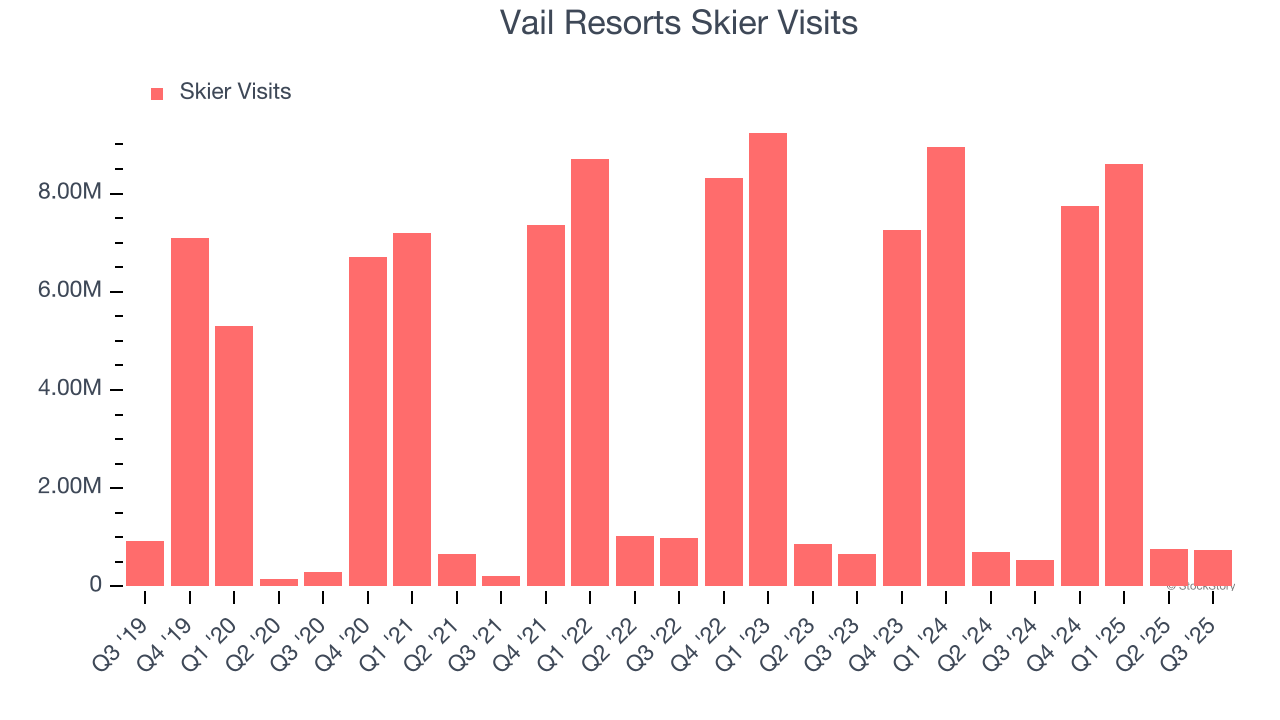

Revenue growth can be broken down into changes in price and volume (for companies like Vail Resorts, our preferred volume metric is skier visits). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Over the last two years, Vail Resorts failed to grow its skier visits, which came in at 739,000 in the latest quarter. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Vail Resorts might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

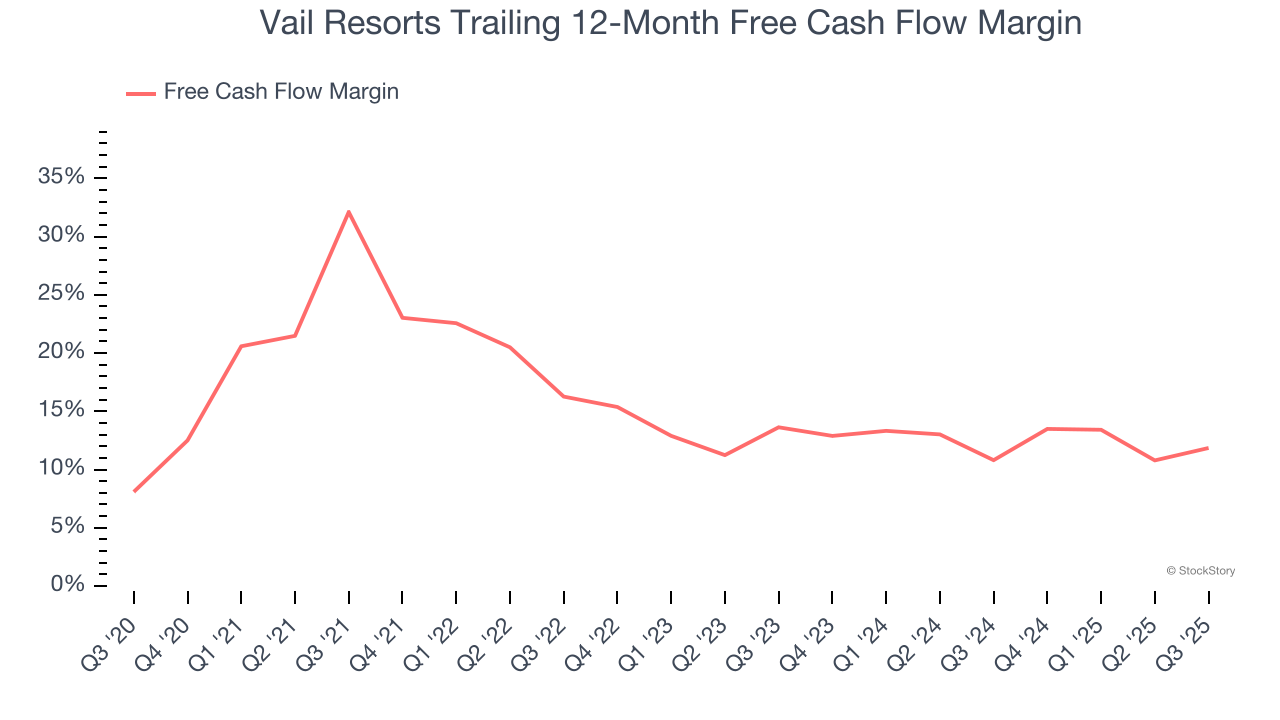

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Vail Resorts has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 11.3%, lousy for a consumer discretionary business.

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Vail Resorts’s ROIC averaged 2.9 percentage point increases each year. This is a good sign, and we hope the company can continue improving.

We cheer for all companies serving everyday consumers, but in the case of Vail Resorts, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 19.4× forward P/E (or $134.59 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are superior stocks to buy right now. Let us point you toward one of Charlie Munger’s all-time favorite businesses.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| 3 hours | |

| Jul-14 | |

| Jul-14 | |

| Jun-18 | |

| Jun-18 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-08 | |

| Jun-08 | |

| Jun-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite