|

|

|

|

|||||

|

|

|

General Motors GM once again emerged as the top-selling automaker in the United States in 2025. Full-year deliveries rose 5.5% to 2.85 million units, driven by gains across all major brands — Chevrolet, Cadillac, GMC and Buick. Japanese auto giant Toyota Motor TM ranked second, selling 2.52 million vehicles in the United States last year. Notably, GM has held the U.S. auto sales crown for decades, losing the top spot once in 2021, when Toyota navigated semiconductor shortages and supply-chain disruptions more effectively.

GM’s market share in the country grew 0.5 percentage points in 2025 to roughly 17%. The company also extended its leadership in full-size pickups for the sixth straight year. Full-year pickup sales reached 940,000 units, up 7%, marking the best combined Chevrolet and GMC full-size pickup performance in two decades. General Motors was the second-largest electric vehicle (EV) seller in the nation in 2025, trailing only Tesla TSLA, with EV sales rising 48% to 169,887 units.

However, momentum slowed in the fourth quarter. GM’s total sales during the quarter fell 7% year over year to 703,001 vehicles, while EV deliveries dropped sharply by 43% to 25,219 units. The decline followed record EV sales in the third quarter of 2025, which were boosted by pull-forward demand ahead of the expiration of the federal EV tax credit.

Despite weaker sales in the final quarter of 2025, General Motors expects demand to remain resilient across price points, supporting momentum into 2026.

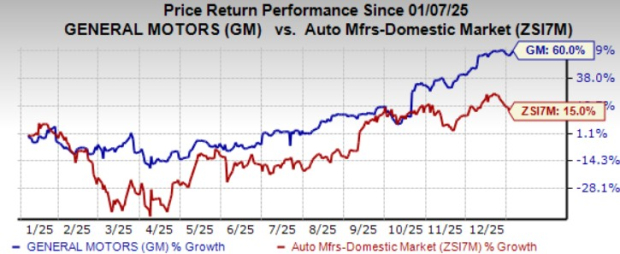

Over the past year, GM shares have risen 60%, handily outperforming the industry. With the stock currently hovering around its 52-week high, is General Motors still worth buying at current levels? Let’s delve deeper.

The U.S. legacy automaker has readjusted its strategy by scaling its EV plans amid weaker-than-expected consumer adoption. GM expects ICE volumes to stay robust while strengthening its production base with onshoring initiatives. Upcoming launches like the next-gen Cadillac CT5, redesigned XT5 and the Orion Assembly plant’s relaunch—set to produce the Cadillac Escalade and new full-size pickups—underscore GM’s commitment to meet customer demand in the U.S. market.

Additionally, General Motors is seeing strong traction in its software and services business, which is emerging as an important growth engine. On its third-quarter earnings call, GM said it has already recorded about $2 billion in revenues from Super Cruise, OnStar and other software products this year. Deferred revenues climbed to $5 billion by the end of the third quarter, up more than 90% from last year. OnStar’s global subscriber base grew 34% to over 11 million and is expected to cross 12 million by year-end. Super Cruise adoption is also picking up, with more than 500,000 active users. GM expects Super Cruise revenues to exceed $200 million in 2025.

Next, GM’s restructuring efforts in China— including overhauling operations by rightsizing, streamlining dealer networks, cutting costs and rolling out new products— have started to pay off. Third-quarter vehicle sales in China increased 10% year over year, marking the second straight quarter of growth. Market share expanded 30 basis points to 6.8%, while equity income climbed to $80 million, its fourth straight quarterly gain.

The company’s superior liquidity profile and investor-friendly moves further instill confidence. General Motors exited third-quarter 2025 with strong automotive liquidity of $35.7 billion. GM repurchased over $3.5 billion of stock from the beginning of 2025 through the third quarter (including $1.5 billion in Q3), reducing its share count by 15% year over year to 954 million. The company ended the quarter with $2.8 billion remaining under its buyback authorization.

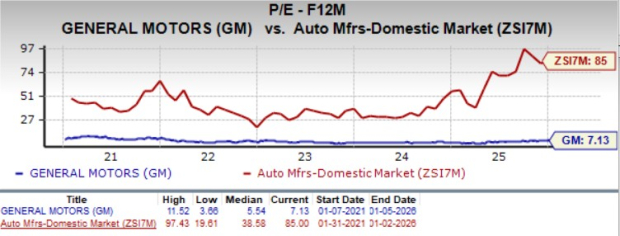

Despite the impressive price performance, GM stock is still trading at just 7.13X forward earnings. Meanwhile, Toyota and Tesla trade at a forward earnings multiple of 10.59 and 252.81, respectively. General Motors has a Value Score of A.

The Zacks Consensus Estimate for 2026 implies an uptick of 13% from the 2025 projected levels. The consensus mark for EPS has moved north over the past 60 days.

General Motors has entered 2026 at a position of strength. The company continues to lead U.S. auto sales, supported by its dominant pickup franchise and brand popularity. Its growing software business adds to investment appeal, while near-term volatility from EV demand normalization does not change the broader earnings outlook.

GM’s strong balance sheet and ongoing buybacks are other positives. The consensus estimates point to steady profit growth next year.

Despite a sharp rally over the past year, the stock still trades at a meaningful discount to peers, suggesting the market is yet to fully price in GM’s earnings power. So, we think General Motors is still a compelling investment at current levels.

The stock sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 28 min | |

| 36 min |

Tesla Expands Robotaxi Service To Orlando, Tampa A Day Before Earnings Report

TSLA

Investor's Business Daily

|

| 38 min |

Trump imposes 50% tariffs on Canada: Markets are accustomed to 'heavy hand' tactic

GM

Yahoo Finance Video

|

| 43 min | |

| 1 hour | |

| 1 hour | |

| 1 hour |

What Construction Of Elon Musk's Terafab Would Mean For Tesla, SpaceX

TSLA

Investor's Business Daily

|

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite