|

|

|

|

|||||

|

|

|

The Trade Desk has gotten torched over the last six months - since July 2025, its stock price has dropped 45.9% to $39.80 per share. This may have investors wondering how to approach the situation.

Following the pullback, is now an opportune time to buy TTD? Find out in our full research report, it’s free for active Edge members.

Built as an alternative to "walled garden" advertising ecosystems, The Trade Desk (NASDAQ:TTD) provides a cloud-based platform that helps advertisers and agencies plan, manage, and optimize digital advertising campaigns across multiple channels and devices.

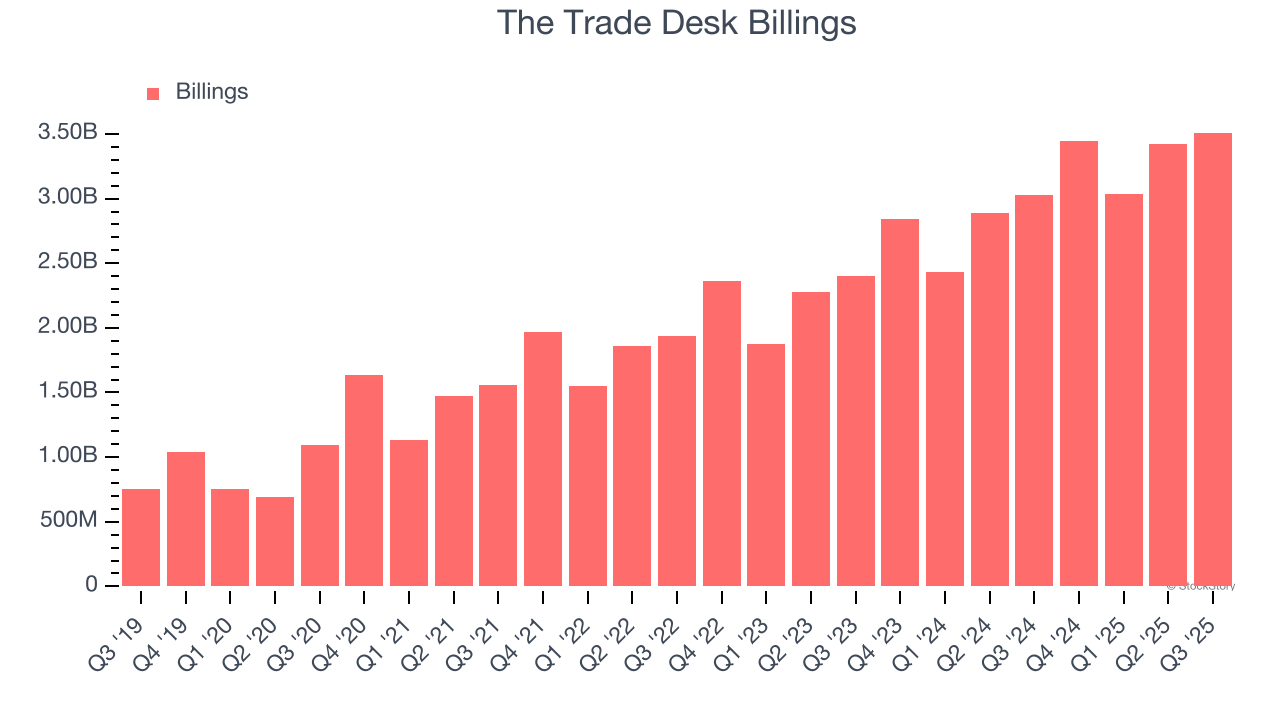

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

The Trade Desk’s billings punched in at $3.51 billion in Q3, and over the last four quarters, its year-on-year growth averaged 20.1%. This performance was impressive, indicating robust customer demand. The high level of cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

The Trade Desk is extremely efficient at acquiring new customers, and its CAC payback period checked in at 5.2 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give The Trade Desk more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

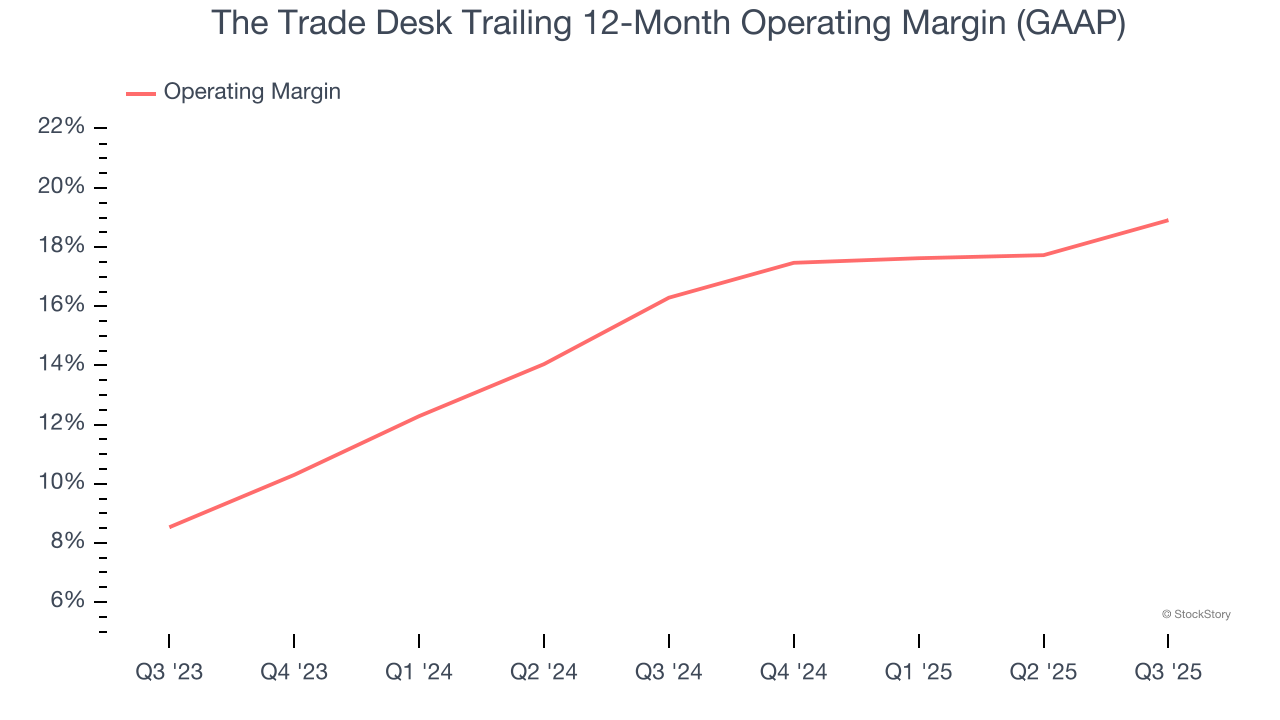

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

The Trade Desk has been a well-oiled machine over the last year. It demonstrated elite profitability for a software business, boasting an average operating margin of 18.9%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

These are just a few reasons why we're bullish on The Trade Desk. After the recent drawdown, the stock trades at 6.2× forward price-to-sales (or $39.80 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free for active Edge members .

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Mar-18 | |

| Mar-18 | |

| Mar-18 | |

| Mar-18 | |

| Mar-17 | |

| Mar-16 | |

| Mar-14 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite