|

|

|

|

|||||

|

|

|

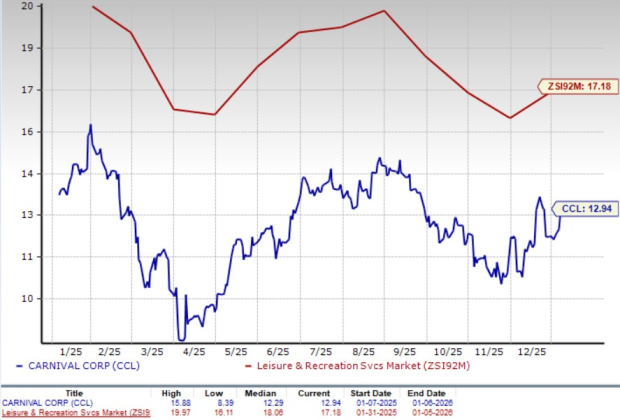

Carnival Corporation & plc CCL is trading at a discount relative to its peers, with a forward 12-month price-to-earnings (P/E) ratio of just 12.94x. This is below the industry average of 17.18x and the broader consumer discretionary sector’s 18.39x.

Despite this valuation gap, CCL’s shares have surged 35.4% over the past year, outperforming the industry’s 8.8% growth. On the other hand, other industry players, such as Norwegian Cruise Line Holdings Ltd. NCLH, OneSpaWorld Holdings Limited OSW and Royal Caribbean Cruises Ltd. RCL, experienced decreases of 6.7% and increases of 14% and 32%, respectively.

Demand and pricing momentum remain key tailwinds. Management highlighted record bookings for both 2026 and 2027, with roughly two-thirds of 2026 already booked at historically high prices across North America and Europe. This strength is notable given weak consumer sentiment indicators, underscoring the resilience of cruise demand. Higher close-in demand and robust onboard spending lifted yields meaningfully in 2025 and the company expects further same-ship yield growth in 2026. Strong customer deposits at year-end, which reached an all-time high, further reinforce confidence in forward demand and cash flow visibility.

Operational execution and cost discipline are materially enhancing profitability. Carnival delivered record revenues, EBITDA and operating income in 2025 while keeping unit cost growth below initial expectations. Effective cost-saving initiatives and scale benefits helped offset inflation, higher dry dock expenses and new destination-related costs. As a result, operating and EBITDA margins expanded significantly year over year, driving return on invested capital more than 13%, the highest level in nearly two decades. Management expects continued cost mitigation in 2026, supporting another year of double-digit earnings growth.

Balance sheet improvement and capital allocation flexibility are emerging as major positives. The company reduced debt by more than $10 billion from peak levels, achieved an investment-grade leverage ratio and completed a large refinancing that lowers future interest expense. Strong cash generation, combined with no ship deliveries in 2026, has allowed Carnival to resume dividends and position itself for further deleveraging and potential share repurchases. At the same time, disciplined reinvestment in destinations like Celebration Key and other private ports is expected to enhance guest experience and create long-term pricing and revenue upside.

Despite strong headline results, several near-term headwinds emerged from the call that could pressure performance going forward. One key concern is cost inflation, particularly in 2026. Management guided to cruise costs (excluding fuel) rising about 3.25% year over year, due to persistent inflation, higher advertising spend and increased dry-dock expenses. Notably, more dry-dock spending is being classified as operating expense rather than capitalized, which directly weighs on margins.

In addition, regulatory costs are rising, with higher emission allowance expenses in Europe and increased income taxes tied to the global minimum tax (Pillar Two), together shaving earnings despite strong operating momentum. The company also acknowledged that first-quarter 2026 costs will be disproportionately high, creating an uneven earnings cadence early in the year.

Another overhang is industry capacity pressure, especially in the Caribbean. Management repeatedly referenced double-digit industry capacity growth in the region, particularly concentrated in shorter itineraries and the first quarter, which creates a tougher pricing and yield environment. While Carnival expressed confidence in absorbing this supply, guidance implies more modest yield growth versus the outsized gains of recent years, suggesting diminishing pricing leverage. At the same time, the company is not benefiting from new ship deliveries in 2026, limiting its ability to offset cost increases with capacity growth.

The company is likely to report solid earnings, with projections indicating a 9.8% rise in fiscal 2026.

Conversely, industry players like Norwegian Cruise, OneSpaWorld and Royal Caribbean are likely to witness an increase of 26.9%, 14.7% and 14.5% respectively, year over year in 2026 earnings.

Strong demand, solid pricing, improving margins and a much healthier balance sheet support staying invested, as the company is executing well and generating consistent earnings growth. However, upside appears more limited from current levels due to rising costs, regulatory pressures and increasing industry capacity that could temper future pricing power. With much of the recovery already reflected in the stock and peers offering faster growth potential, new investors may be better off waiting for a more favorable entry point.

CCL currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-18 | |

| Jul-17 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-10 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-08 | |

| Jul-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite