|

|

|

|

|||||

|

|

|

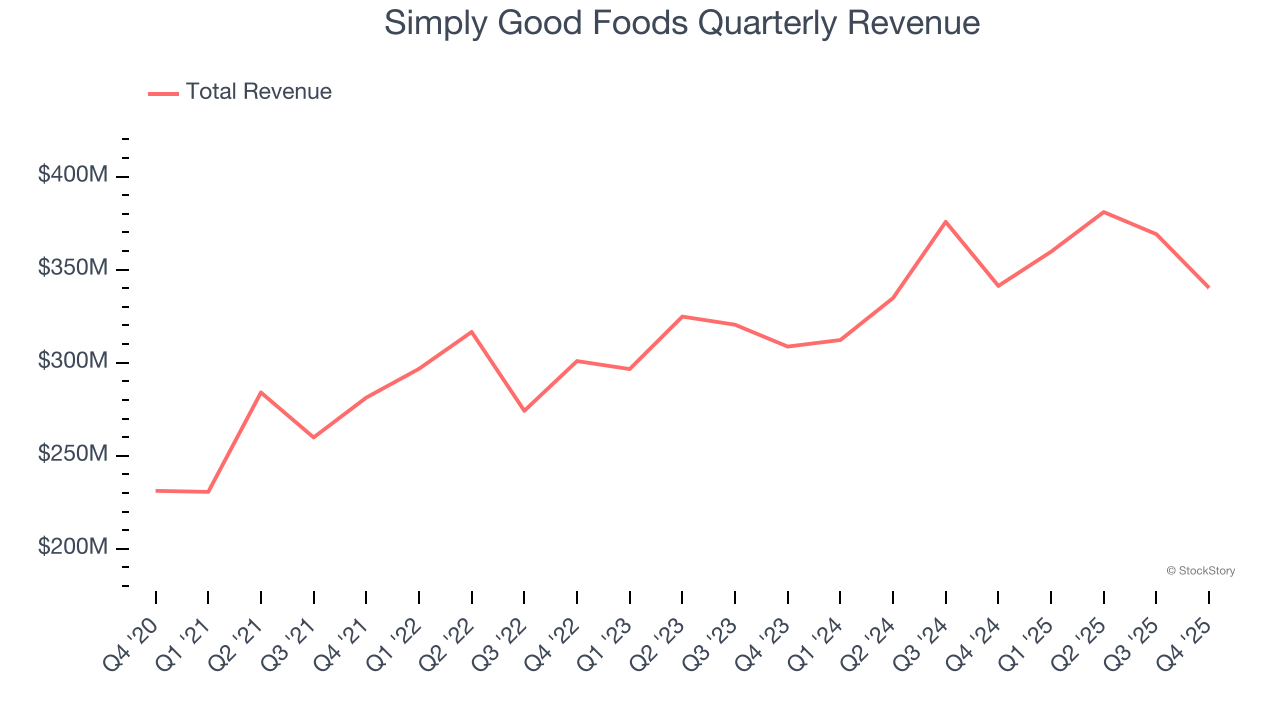

Packaged food company Simply Good Foods (NASDAQ:SMPL) reported revenue ahead of Wall Streets expectations in Q4 CY2025, but sales were flat year on year at $340.2 million. Its non-GAAP profit of $0.39 per share was 8.2% above analysts’ consensus estimates.

Is now the time to buy Simply Good Foods? Find out by accessing our full research report, it’s free for active Edge members.

“Our first quarter financial performance came in modestly ahead of our expectations. Total company consumption growth of 2% was led by Quest and OWYN, which grew aggregate consumption double-digits, while Atkins performed as expected," said Geoff Tanner, President and Chief Executive Officer of Simply Good Foods.

Best known for its Atkins brand that was inspired by the popular diet of the same name, Simply Good Foods (NASDAQ:SMPL) is a packaged food company whose offerings help customers achieve their healthy eating or weight loss goals.

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.45 billion in revenue over the past 12 months, Simply Good Foods is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Simply Good Foods’s 6.9% annualized revenue growth over the last three years was mediocre. This shows it couldn’t generate demand in any major way and is a tough starting point for our analysis.

This quarter, Simply Good Foods’s $340.2 million of revenue was flat year on year but beat Wall Street’s estimates by 1.2%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and indicates its products will see some demand headwinds.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

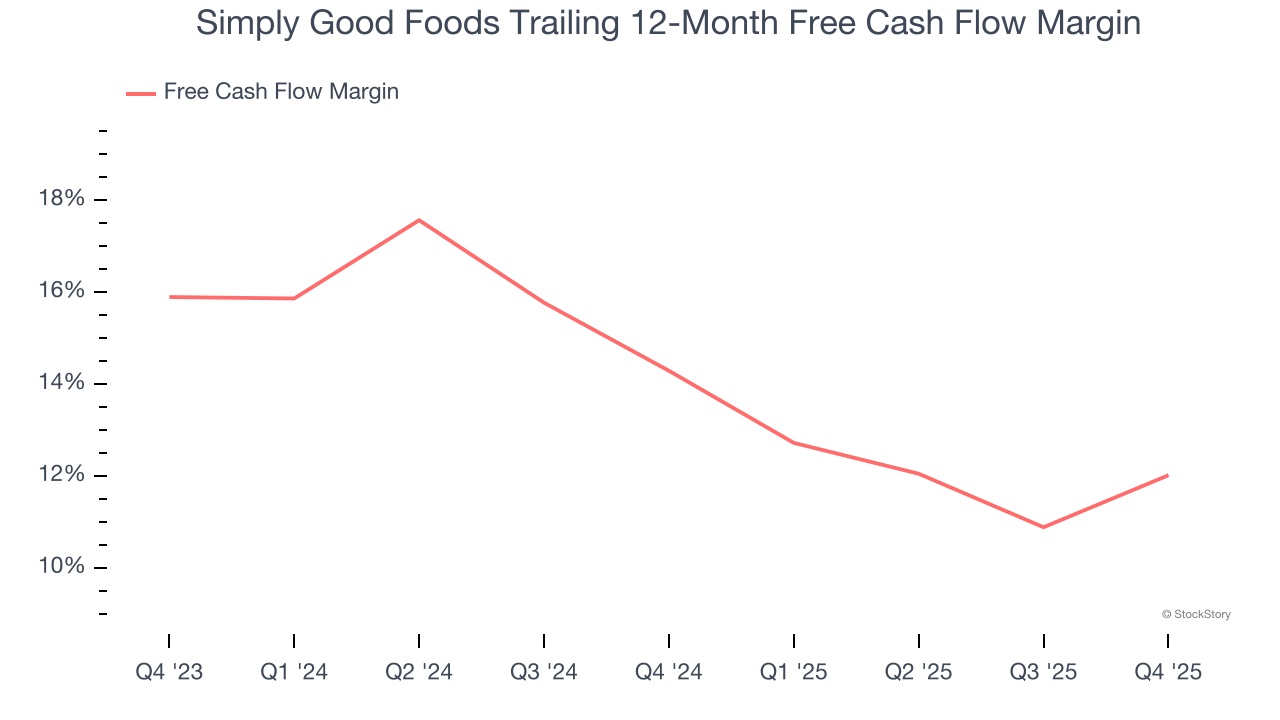

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Simply Good Foods has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging 13.1% over the last two years.

Taking a step back, we can see that Simply Good Foods’s margin dropped by 2.3 percentage points over the last year. Continued declines could signal it is in the middle of an investment cycle.

Simply Good Foods’s free cash flow clocked in at $48 million in Q4, equivalent to a 14.1% margin. This result was good as its margin was 4.8 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

It was good to see Simply Good Foods beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its gross margin missed. Zooming out, we think this was a mixed quarter. The stock remained flat at $19.56 immediately following the results.

Big picture, is Simply Good Foods a buy here and now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jul-14 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jun-18 | |

| Jun-11 | |

| Jun-03 | |

| Jun-03 | |

| Jun-03 | |

| May-19 | |

| Apr-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite