|

|

|

|

|||||

|

|

|

Pilgrim’s Pride Corporation PPC reported fourth-quarter 2025 results, wherein both top and bottom lines fell short of the Zacks Consensus Estimate. While net sales increased, earnings decreased from the year-ago period’s actuals. The company has been benefiting from its portfolio diversification strategies, operational excellence, branded offerings and key customer partnerships.

Pilgrim's Pride reported adjusted earnings of 64 cents per share, missing the Zacks Consensus Estimate of 78 cents. Also, the figure decreased from adjusted earnings of $1.35 per share in the year-ago quarter. On a GAAP basis, earnings were 37 cents per share, down from 99 cents in the year-ago period.

Pilgrim's Pride Corporation price-consensus-eps-surprise-chart | Pilgrim's Pride Corporation Quote

The producer, marketer and distributor of fresh, frozen and value-added chicken and pork products generated net sales of $4,517.8 million, which increased 3.3% from the year-ago quarter. However, the top line missed the consensus mark of $4,600 million.

Pilgrim's Pride’s cost of sales was $4,089.2 million, which increased from $3,818.8 million reported in the year-ago quarter. Gross profit fell year over year to $428.6 million from $553.3 million.

The company reported an adjusted EBITDA of $415.1 million, down from $525.7 million reported in the year-ago quarter. The adjusted EBITDA margin was 9.2%, a decrease from 12% reported in the prior-year quarter.

The operating income was $204.1 million, a year-over-year decrease from $306.7 million.

Net sales in the U.S. operations were $2,598.5 million, down from $2,613.2 million in the year-ago quarter. Despite the modest decline, the Fresh portfolio benefited from continued consumer demand, with volumes increasing year over year. Demand from key customers remained solid across retail, QSR and food-service channels. Strength in Case Ready and Small Bird supported performance, while operational improvements in Big Bird mitigated the impact of softer commodity pricing. U.S. Prepared Foods net sales rose 18% from the prior year, driven by strong retail and food-service demand. Just Bare continued to gain share in the frozen fully cooked category and food-service volumes grew more than 20% year over year.

Net sales from Europe operations increased to $1,383.6 million in the quarter under review from $1,259.2 million in the prior-year quarter. The region delivered higher sales and adjusted EBITDA, supported by an improved product mix, manufacturing optimization and ongoing management integration initiatives. Branded diversification remained a key growth driver, with Fridge Raiders and Rollover again outpacing their respective categories.

Mexico operations generated net sales of $535.7 million in the reported quarter, up from $499.6 million in the prior-year quarter. However, profitability was pressured by increased imports and weaker live commodity fundamentals during the latter half of the year. Despite these headwinds, volumes improved year over year. In Fresh, key customer demand remained steady, while branded offerings grew nearly 10%. Prepared Foods sales increased 8%, reflecting continued progress in diversification efforts.

The company ended the quarter with cash and cash equivalents of $640.2 million, long-term debt (less current maturities) of $3,093.1 million and total shareholders’ equity of $3,693.7 million. The company provided $1,371.7 million in cash from operating activities for the year ended Dec. 28, 2025.

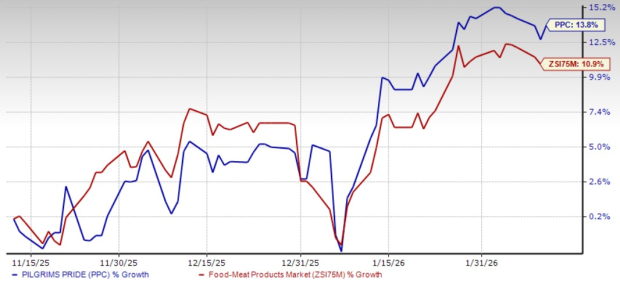

This Zacks Rank #5 (Strong Sell) stock has gained 13.8% in the past three months compared with the industry’s 10.9% growth.

The Hershey Company HSY engages in the manufacture and sale of confectionery products and pantry items in the United States and internationally. It sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Hershey’s current financial-year sales and earnings indicates growth of 4.4% and 27.1%, respectively, from the prior-year reported levels. HSY delivered a trailing four-quarter earnings surprise of 17.2%, on average.

The Simply Good Foods Company SMPL, a consumer-packaged food and beverage company, engages in the development, marketing and sale of snacks and meal replacements, and other products in North America and internationally. It holds a Zacks Rank #2 (Buy) at present. SMPL delivered a trailing four-quarter earnings surprise of 5.5%, on average.

The Zacks Consensus Estimate for Simply Good Foods’ current fiscal-year earnings implies growth of 1.6%, from the year-ago figures.

Monster Beverage Corporation MNST is a marketer and distributor of energy drinks and alternative beverages. It currently carries a Zacks Rank #2. MNST delivered a trailing four-quarter earnings surprise of 5.5%, on average.

The Zacks Consensus Estimate for Monster Beverage’s current financial-year sales and earnings indicates growth of 9.5% and 22.8%, respectively, from the prior-year reported levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite