|

|

|

|

|||||

|

|

|

Illinois Tool Works is a highly diversified, high-margin industrial conglomerate with a rock-solid dividend.

PepsiCo yields considerably more than Illinois Tool Works and commands a less expensive valuation.

Pepsi has plenty of ways to return to growth without overhauling its proven business model.

Dividend Kings are an elite group of dividend-paying companies that have boosted their payouts for at least 50 consecutive years. There are fewer than 60 Dividend Kings, and industrial conglomerate Illinois Tool Works (NYSE: ITW) is one of them.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Illinois Tool Works is an excellent company with high operating margins and dozens of brands across multiple industries. However, the company's growth has slowed due to cyclical downturns in key markets, demand and tariff pressures, and currency headwinds.

Despite these challenges, ITW is a strong buy for 2026. The company has increased its dividend for 62 consecutive years and consistently repurchases stock. ITW also commands a reasonable valuation for such a reliable dividend payer, trading at 22.5 times forward earnings with a 2.6% dividend yield.

Here's why PepsiCo (NASDAQ: PEP) could be an even better Dividend King to buy in the new year -- especially for investors looking to maximize their passive income.

Image source: Getty Images.

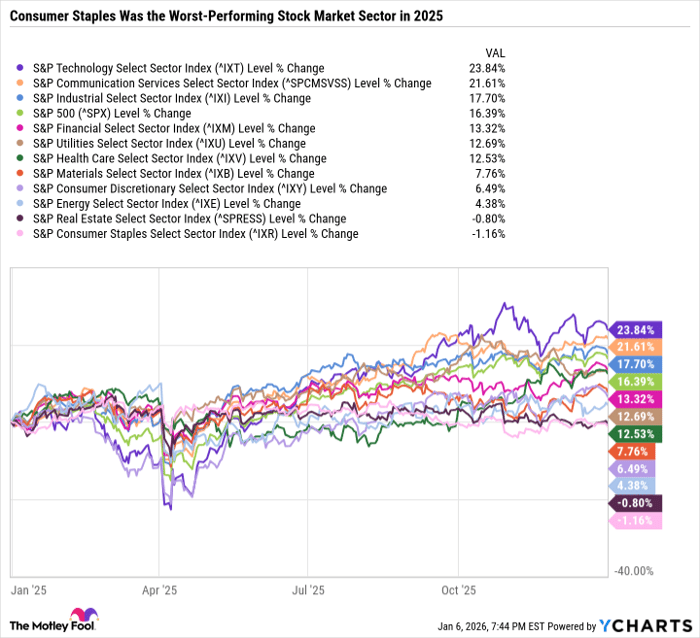

Like many consumer staples stocks, Pepsi had a down year in 2025, with the stock falling 5.6%. Consumer staples were one of two sectors that lost value in 2025 despite an excellent year for the broader market.

Data by YCharts.

In addition to beverage brands like flagship Pepsi, Gatorade, and Mountain Dew, PepsiCo owns Frito-Lay and Quaker Oats, as well as a variety of other brands across snack and mini meals categories. But Pepsi is facing a demand slowdown due to shifting consumer preferences toward health and wellness, as well as the higher cost of living, production cost pressures, and tariffs.

Pepsi is forecasting a low single-digit increase in full-year 2025 organic revenue and flat core constant currency earnings per share. Pepsi's results are poor, but that's already reflected in the stock price.

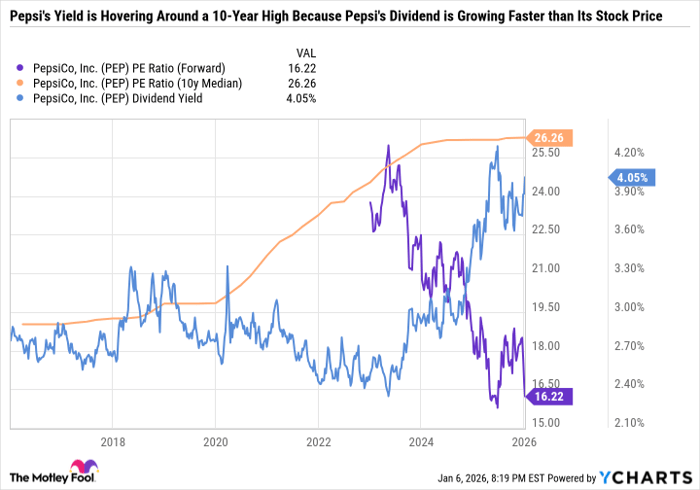

Pepsi stock sports a mere 16.2 forward price-to-earnings ratio compared to a 10-year median P/E of 26.3. Its dividend yield is over 4%, which is significantly higher than its historical average.

Data by YCharts.

Some investors have lost faith in Pepsi or are simply unwilling to pay as high a multiple for its earnings because the company's growth has stalled. But the sell-off has gone too far, especially considering Pepsi's issues are solvable.

Pepsi recognizes that it must improve its product portfolio to lean less on sugary soft drinks and salty snacks by diversifying into healthier options, such as mini meals, healthier drink and snack brands, or healthier versions of existing brands.

After all, the trend toward healthier options is nothing new, as per capita soft drink consumption in the U.S. has been declining for years. And it was all the way back in 2002 when Frito-Lay launched reduced-fat Lay's and Cheetos.

In September, activist investor Elliott Asset Management took a $4 billion stake in PepsiCo, arguing that the company can make several operational improvements, such as a refranchised bottler network and brand improvements to improve margins and accelerate earnings growth. If that were to happen, Pepsi could quickly shift from trading at a steep discount to the broader market to reclaiming its premium valuation.

With the valuation discounted and the dividend yield at 4.1%, Pepsi stands out as a no-brainer buy for risk-averse income investors in 2026.

Before you buy stock in PepsiCo, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and PepsiCo wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $488,222!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,134,333!*

Now, it’s worth noting Stock Advisor’s total average return is 969% — a market-crushing outperformance compared to 196% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 9, 2026.

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool recommends Illinois Tool Works. The Motley Fool has a disclosure policy.

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-13 | |

| Jul-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite