|

|

|

|

|||||

|

|

|

Medical supplies stocks are rarely where investors look for outsized returns. These companies operate on razor-thin margins, move massive volumes, and live under constant pressure from regulation, reimbursement changes and pricing negotiations. In a tough macro environment —marked by high interest rates, cost inflation and cautious hospital spending — outperformance from this group would seem even less likely.

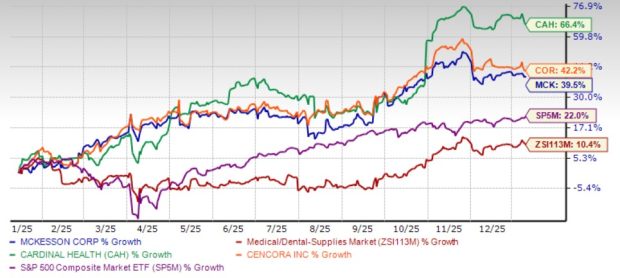

Yet over the past year, a few medical supplies distributors have quietly done exactly that. Cardinal Health CAH,McKesson MCKand Cencora COR have all delivered stock returns that comfortably beat the broader market, with gains of 66.4% for CAH, 39.5% for MCK and 42.2% for COR.

What separates these names is not macro luck, but execution. In healthcare distribution, scale, specialty exposure, and disciplined capital allocation often matter far more than the economic cycle. These three companies demonstrate how seemingly “boring” businesses can still generate attractive, durable shareholder returns.

Cardinal Health: A Turnaround That’s Gaining Traction

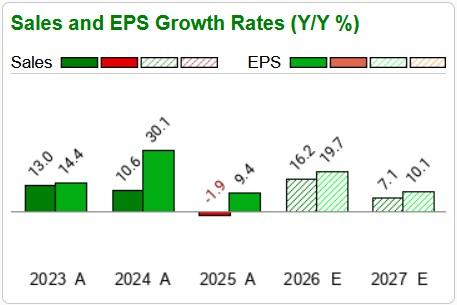

Cardinal Health’s recent stock performance reflects a business that is finding its footing again —particularly in areas that matter most to investors. In the first quarter of fiscal 2026, the company delivered double-digit operating earnings growth across all five operating segments, signaling that improvement is no longer isolated to one corner of the business.

Revenues climbed 22% year over year to $64 billion, driven by strong pharmaceutical demand and continued GLP-1 volumes. Moreover, the Pharmaceutical and Specialty Solutions segment profit rose 26%, supported by solid execution across brand, specialty and generics distribution.

The long-term story, however, lies in specialty. Cardinal Health continues to expand its MSO platforms and BioPharma Solutions business, with management pointing to additional momentum from the pending acquisition of Solaris Health, a large urology-focused MSO. The deal is designed to deepen provider relationships and improve business mix over time.

From a shareholder perspective, the cash flow is showing up. Cardinal Health generated $1.3 billion in adjusted free cash flow in the quarter and returned $500 million to shareholders through dividends and buybacks. While tariffs remain a challenge for the medical products segment, management remains confident in mitigation efforts.

CAH currently carries a Zacks Rank #2 (Buy). The earnings estimates for fiscal 2026 have moved north 7 cents to $9.86 per share over the past 60 days. The company has a Zacks Style Score of ‘A’. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

McKesson: The Gold Standard in Execution

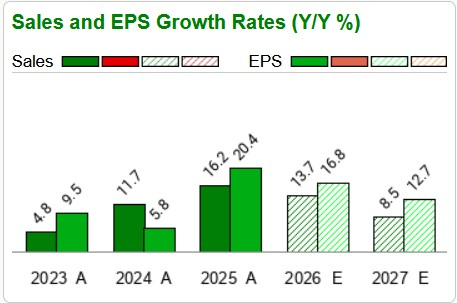

McKesson continues to stand out as the best-in-class operator in healthcare distribution. In the second quarter of fiscal 2026, the company posted 10% revenue growth to $103 billion and 39% adjusted EPS growth, a reminder of how powerful scale can be when paired with discipline.

Much of the momentum came from the newly reorganized Oncology and Multispecialty segment. Revenues in the segment jumped 32%, while operating profit surged 71%, driven by strong specialty volumes and contributions from recent acquisitions. Even excluding acquisition-related gains, McKesson delivered healthy organic profit growth.

McKesson’s core pharmaceutical distribution business also benefited from rising prescription volumes and improved mix. Meanwhile, ongoing investments in automation are quietly improving efficiency — reducing manual handling and supporting margins over time.

The financial payoff is clear. McKesson generated $2.2 billion in free cash flow during the quarter and returned $907 million to shareholders, largely through share repurchases. Management raised full-year adjusted EPS guidance to $38.35-$38.85.

MCK currently carries a Zacks Rank #3 (Hold). The earnings estimates for fiscal 2026 have moved up 37 cents to $38.61 per share over the past 60 days. The company has a Zacks Style Score of ‘A’.

Cencora: Specialty Strength With a Long View

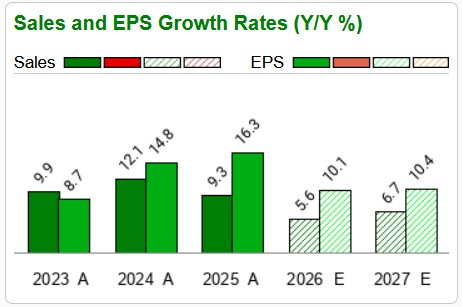

Cencora’s outperformance highlights how specialty-focused distribution can deliver growth even as broader healthcare spending normalizes. In the fourth quarter of fiscal 2025, the company posted 6% revenue growth and 15% adjusted EPS growth, led by its U.S. Healthcare Solutions segment.

Operating income rose 20% year over year, supported by strong specialty demand and the contribution from the Retina Consultants of America acquisition, which also helped expand margins. Management noted that this strength more than offset the loss of a large oncology customer earlier in the year.

Looking forward, Cencora remains focused on investments that support sustained growth. The company plans to invest roughly $1 billion through 2030 to expand distribution capacity and cold-chain infrastructure, positioning the business to handle increasing specialty complexity.

Cencora generated $3 billion in adjusted free cash flow in fiscal 2025 and returned nearly $900 million to shareholders, including a 9% dividend increase.

COR currently carries a Zacks Rank of 3. The earnings estimates for fiscal 2026 have moved north 3 cents to $17.62 per share over the past 60 days. The company has a Zacks Style Score of ‘A’.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-22 | |

| Jul-21 |

Cardinal Health makes acquisition duo worth $360m for home care business advance

CAH

Medical Device Network

|

| Jul-21 | |

| Jul-20 | |

| Jul-09 | |

| Jul-09 | |

| Jul-08 | |

| Jul-01 | |

| Jun-30 | |

| Jun-24 | |

| Jun-15 | |

| Jun-03 | |

| Jun-03 | |

| Jun-02 | |

| May-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite