|

|

|

|

|||||

|

|

|

Walmart Inc.’s WMT Sam’s Club continued to demonstrate steady momentum in its membership base during the third quarter of fiscal 2026, reinforcing the importance of renewal strength to the club’s overall performance.

Sam’s Club U.S. membership income increased 7.1% year over year, driven by growth in member counts, stable renewal rates and higher Plus member penetration. Membership and other income for the segment rose 13.1%, highlighting the expanding contribution of recurring fee revenues.

Management emphasized that renewal rates remain strong and consistent, supported by higher engagement levels across the member base. Digital tools such as Scan & Go continue to play a role in sustaining engagement, with adoption reaching 36% in the quarter, up 450 basis points from last year. The company noted that members are increasingly using digital features both inside the club and through curbside pickup and delivery, reinforcing the perceived value of the membership.

Sam’s Club U.S. comparable sales, excluding fuel, increased 3.8% during the quarter, with transactions up 3.9%. Management linked this performance to steady member activity and repeat shopping behavior, particularly in grocery and general merchandise categories. E-commerce sales at Sam’s Club advanced 22%, with continued strength in club-fulfilled pickup and delivery, further supporting member convenience.

Overall, Walmart pointed to solid new member additions alongside steady renewal trends during the quarter. Continued growth in Plus membership and deeper engagement across digital and in-club services helped support membership income, reinforcing the role of renewals as a stable and recurring driver within Sam’s Club’s operating model.

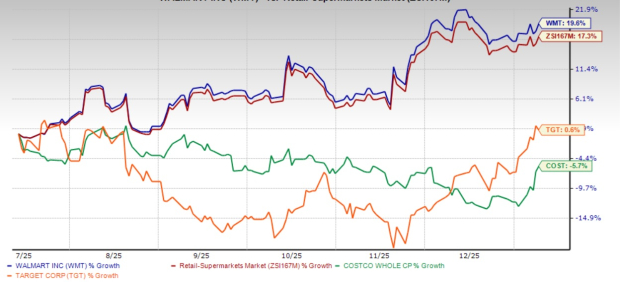

Walmart, which competes with Costco Wholesale Corporation COST and Target Corporation TGT, has seen its shares rally 19.6% in the past six months compared with the industry’s growth of 17.3%. Shares of Costco have declined 5.7%, while Target climbed 0.6% in the aforementioned period.

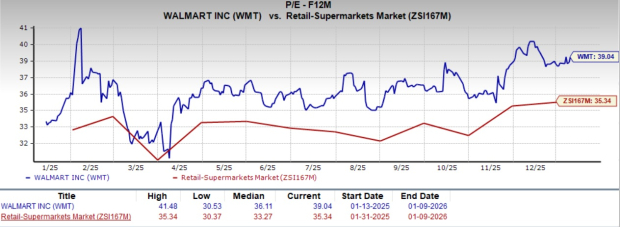

From a valuation standpoint, Walmart's forward 12-month price-to-earnings ratio stands at 39.04, higher than the industry’s 35.34. WMT carries a Value Score of C. Walmart is trading at a premium to Target (with a forward 12-month P/E ratio of 13.69) but at a discount to Costco (44.54).

The Zacks Consensus Estimate for Walmart’s current financial-year sales and earnings per share implies year-over-year growth of 4.5% and 4.8%, respectively.

Walmart currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite