|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

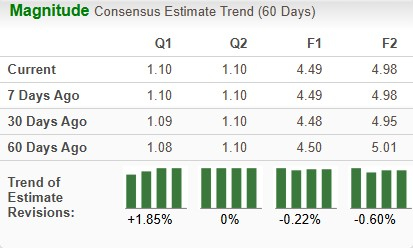

AstraZeneca AZN will report its first-quarter 2025 earnings on April 29, before market open. The Zacks Consensus Estimate for sales and earnings is pegged at $13.68 billion and $1.10 per share, respectively. Earnings estimates for AstraZeneca have risen from $4.48 per share to $4.49 per share for 2025 over the past 30 days. (Find the latest earnings estimates and surprises on Zacks Earnings Calendar.)

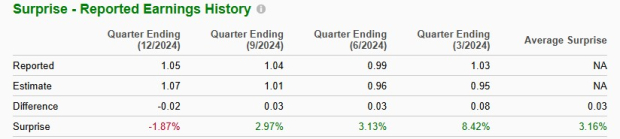

The healthcare bellwether’s performance has been mixed, with the company exceeding earnings expectations in three of the trailing four quarters while missing in one. It delivered a four-quarter earnings surprise of 3.16%, on average. In the last reported quarter, the company delivered a negative earnings surprise of 1.87%.

AstraZeneca has an Earnings ESP of +2.73% and a Zacks Rank #3 (Hold), indicating a likely positive surprise. Per our proven model, companies with the combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), #2 (Buy) or #3 have a good chance of delivering an earnings beat. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Sales of AstraZeneca’s key medicines, mainly cancer drugs — Lynparza, Tagrisso and Imfinzi — and diabetes medicine Farxiga are expected to have driven the company’s top line in the first quarter backed by strong underlying demand trends.

The Zacks Consensus Estimate for Lynparza, Tagrisso and Imfinzi is $758 million, $1.62 billion and $1.29 billion, respectively.

Our model estimates for Lynparza, Tagrisso and Imfinzi are $781.0 million, $1.67 billion and $1.35 billion, respectively.

However, sales of Farxiga and Lynparza in China might have been impacted by the inclusion in the VBP program.

AstraZeneca’s other drugs, Fasenra, Calquence and Breztri are likely to have contributed to sales growth in the soon-to-be-reported quarter.

The Zacks Consensus Estimate for Fasenra and Farxiga is $380 million and $1.90 billion, respectively.

Our model estimates for Fasenra and Farxiga are $377.2 million and $1.87 billion, respectively.

Like the past three quarters, sales of key respiratory medicine, Symbicort, are expected to have risen in the first quarter due to strong underlying demand in the United States, which is likely to have offset the impact of generic erosion in Europe and Japan and a slowing overall market in Europe.

The Zacks Consensus Estimate for Symbicort is $772 million, while our model estimate is $767.2 million.

Sales of AstraZeneca’s major legacy drugs have been declining due to rising generic competition. The trend is likely to have continued in the first quarter.

Sales of AstraZeneca’s Rare Disease drugs like Ultomiris and Strensiq are expected to have been strong and contributed to the top line. Sales of Soliris are likely to have declined due to conversion to Ultomiris. Biosimilar versions of Soliris, Amgen's AMGN Bekemv and Teva Pharmaceuticals TEVA/Samsung Bioepis' Epysqli, were recently launched in the United States, which are likely to hurt sales from the second quarter onward.

AstraZeneca’s newer products, asthma drug Tezspire, breast cancer drug Truqap, hereditary transthyretin-mediated amyloidosis drug Wainzua, paroxysmal nocturnal hemoglobinuria treatment, Voydeya and lupus drug, Saphnelo (anifrolumab), are also likely to have contributed to sales growth.

Sales of Wainua, Truqap and Saphnelo improved sequentially in the fourth quarter, a trend likely to have continued in the first quarter.

Investors will be keen to know the sales numbers of AstraZeneca and partner Sanofi’s SNY respiratory syncytial virus (“RSV”) antibody Beyfortus (nirsevimab).

AstraZeneca records a 50% share of gross profits on sales of Beyfortus in major markets outside the United States and 25% of brand revenues in the rest of world markets received from partner Sanofi as Alliance revenues. It also records Beyfortus product sales from products supplied to partner Sanofi under the Vaccines & Immune Therapies segment.

Beyfortus’ sales were significantly strong in the fourth quarter, driven by increased demand and expanded production capacity. It remains to be seen if the positive trend continued in the first quarter.

Alliance revenues should be an important contributor to top-line growth, driven by continued growth in royalties and profit share from partnered medicines.

AstraZeneca’s product sales gross margins are expected to be lower in 2025 due to the net effect of the IRA in the United States, the anticipated inclusion of Farxiga and Lynparza in the VBP program in China, and growth for partner medicines, which have lower gross margins.

Nonetheless, a single quarter’s results are not so important for long-term investors. Let us delve deeper to understand whether to buy, sell or hold AstraZeneca stock.

AstraZeneca’s stock has risen 4.6% so far this year against a decrease of 7.1% for the industry.

From a valuation standpoint, AstraZeneca is decently priced. Going by the price/earnings ratio, the company’s shares currently trade at 14.58 forward earnings, lower than 15.07 for the industry as well as its 5-year mean of 18.11.

AstraZeneca boasts a diversified geographical footprint as well as a product portfolio with several blockbuster medicines. AstraZeneca now has 16 blockbuster medicines in its portfolio with sales (product sales and alliance revenues) exceeding $1 billion, including Tagrisso, Fasenra, Farxiga, Imfinzi, Lynparza, Soliris and Ultomiris. These drugs are driving the company’s top line, backed by increasing demand trends. The company is confident that the growth will continue in 2025.

Oncology is AstraZeneca’s biggest segment. The company has been working on strengthening its oncology product portfolio through label expansions of existing products and progressing oncology pipeline candidates. AstraZeneca has also been making significant progress with its pipeline in other areas, such as cardiovascular health, immunology and rare diseases.

AstraZeneca faces its share of headwinds. There have been rising concerns over the ongoing investigations at AstraZeneca’s China subsidiary. Authorities in China are investigating some current and former AstraZeneca employees for medical insurance fraud, illegal drug importation and personal information breaches.

AstraZeneca expects Farxiga and Lynparza to be included in the VBP plans in China in 2025 which can hurt sales of these drugs in China in the year.

However, the company is confident of continued growth momentum in the Oncology, Rare Disease and CVRM segments in 2025.

Backed by its new products and pipeline drugs, AstraZeneca believes it can post industry-leading top-line growth in the 2025-2030 period. The company is also on target to achieve a mid-30s percentage core operating margin by 2026.

No matter how the first-quarter results play out, we suggest that those who own AstraZeneca’s stock stay invested as the company shows potential for generating consistent profits.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 51 min | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite