|

|

|

|

|||||

|

|

|

Affirm Holdings Inc (NASDAQ:AFRM) shares initially jumped in early trading Monday before giving back gains as investors digested a new source of risk for traditional credit cards. Here’s what investors need to know.

Over the weekend, President Donald Trump warned card issuers that if they do not cut interest rates to 10% by Jan. 20, they will be treated as in "violation of the law" and face "very severe" consequences, calling current 20% to 30% APRs abuse of consumers.

This sharp escalation from policy rhetoric to explicit legal threats sent shares of major card and bank issuers lower and initially pushed investors toward alternative consumer-credit names like Affirm.

Affirm is a leading buy now, pay later (BNPL) platform. Instead of revolving balances at variable interest rates, Affirm offers installment loans that are approved at the point of sale, often with zero late fees and simple, upfront cost disclosures. The company partners with large merchants and platforms in e-commerce, travel and retail, integrating its checkout button online and in stores.

Affirm earns revenue primarily from merchant discount fees and, on some products, consumer interest income that is funded via bank partners and securitizations. Its model is built around underwriting each transaction individually and giving consumers a fixed payoff schedule rather than open-ended revolving credit.

If a 10% APR cap were enforced, legacy card issuers' economics would be squeezed, likely forcing them to cut rich rewards programs, tighten credit or add more fees. That could reduce the appeal and availability of revolving credit, especially for sub-prime and younger consumers, pushing merchants to seek alternative financing tools that still drive conversion.

Because Affirm charges merchants rather than relying solely on high consumer APRs, it could remain economically viable where capped credit cards struggle, allowing BNPL to gain share at checkout.

Even if the ultimatum is softened or challenged, the political focus on "affordability" and perceived abuses by card companies supports the narrative that transparent, installment-based products like Affirm's are a consumer-friendly alternative, positioning AFRM as a potential long-term beneficiary of any structural reset in U.S. credit card pricing.

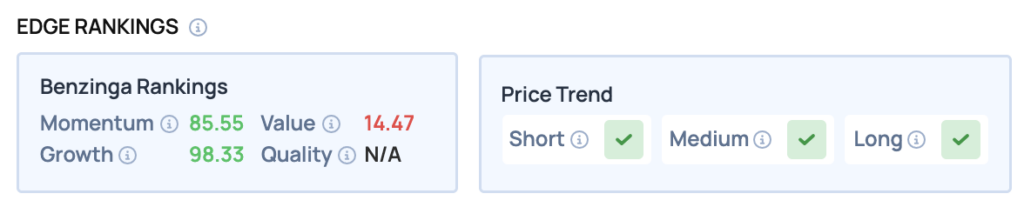

Benzinga Edge Rankings: Benzinga Edge ranks Affirm with exceptionally high growth and momentum scores — 98.33 and 85.55 respectively — highlighting its strong performance outlook despite low value ratings.

Analysts have generally maintained a positive outlook on Affirm Holdings, with TD Cowen and Truist Securities reiterating “Buy” ratings, while RBC Capital maintained a “Sector Perform” rating. The most recent action came from TD Cowen, which adjusted its target price to $110.00 from $115.00.

Earlier, Wolfe Research initiated coverage on Affirm with a “Peer Perform” rating. Freedom Capital Markets also began coverage on the firm with a “Buy” rating and a target price of $90.00.

Notably, Truist Securities and RBC Capital both revised their target prices downward to $85.00 and $87.00, respectively.

AFRM Price Action: Affirm Holdings shares were down 6.87% at $76.18 at the time of publication on Monday, according to Benzinga Pro data. The stock has traded in a wide range of $75.25 to $84.65 on Monday.

Image: Shutterstock

| Jul-17 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-01 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-25 | |

| Jun-25 | |

| Jun-25 | |

| Jun-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite