|

|

|

|

|||||

|

|

|

Shares of U.S. legacy automaker Ford F have surged more than 40% over the past year, handily outperforming the industry. Despite that, the company still appears undervalued. Ford trades at a forward price-to-earnings ratio of 9.79, below its peer group.

Ford’s U.S. vehicle sales rose 6% year over year to 2.2 million vehicles in 2025, marking its best annual U.S. sales performance since 2019. Strong demand for trucks, SUVs, and hybrids drove deliveries. The Ford F-Series remained America’s best-selling truck in 2025. Ford was the third largest automaker in the United States in 2025 by sales volumes, just behind General Motors GM and Toyota TM. General Motors’ full-year deliveries rose 5.5% to 2.85 million units, while Toyota sold 2.52 million vehicles.

But while 2025 was a strong year for the U.S. auto industry, 2026 may not match the strength of last year. Industry experts anticipate sales to slow this year amid affordability challenges, tariff woes, policy changes and weak electric vehicle (EV) adoption.

Given these dynamics, should investors consider buying F stock now that it is trading at a discounted value? Let’s assess.

Ford’s broad lineup, anchored by its F-Series trucks, Maverick pickup, and popular SUVs, provides a solid foundation for growth. Its hybrid strategy adds resilience amid weak EV sales. The company sold a record 228,072 hybrid vehicles (including PHEVs) in 2025, marking a 21.7% increase. The year concluded with record hybrid sales in the fourth quarter of 2025, with 55,374 vehicles sold.

Amid slower EV adoption, changing U.S. regulations under the Trump administration and rising costs, Ford is now leaning more toward hybrids, gas-powered vehicles, and smaller, affordable EVs. As a part of this strategy, the company will no longer launch a fully electric version of its best-selling F-150 pickup. Instead, the F-150 Lightning will be redesigned as a hybrid, featuring a gas-powered generator. Ford is also canceling its upcoming electric van and doubling down on gas and hybrid alternatives.

By scaling back its EV plans that no longer match demand, Ford is basically shifting resources toward higher-margin vehicles and proven revenue drivers. While this will impact near-term financials, with about $19.5 billion in special charges, mostly in the fourth quarter, as the company restructures its U.S. EV assets, the pivot is crucial for capital efficiency and future profitability.

Ford Pro remains a key growth engine, supported by strong order books, rising demand for Super Duty trucks, and expanding software and service offerings. Strength across vehicles, software, and physical services underpins the segment’s momentum. Paid subscriptions rose 8% to 818,000 in the third quarter. Partnership with ServiceTitan enhances digital service capabilities, positioning Ford Pro as a major long-term earnings driver for the company.

Ford is launching a new battery energy storage systems business to tap rising demand from data centers and grid infrastructure. The company will leverage its wholly owned plants in Kentucky and Michigan and lithium iron phosphate technology, with shipments expected to start in 2027 and annual capacity targeted at 20 GWh. This initiative aims to create a diversified, profitable revenue stream, and Ford plans to invest about $2 billion over the next two years to scale the business.

Ford is accelerating its autonomy strategy with plans to introduce Level 3, “eyes-off” highway driving by 2028 on its new Universal Electric Vehicle platform, starting with an affordable $30,000 electric pickup. Built on in-house technology, lidar, and a new computing system, the goal is to evolve beyond BlueCruise and make advanced autonomy more accessible once regulatory approvals come through.

Alongside automation, Ford is also leaning into artificial intelligence. The company will roll out a new AI assistant through Ford and Lincoln mobile apps, followed by full in-vehicle integration starting in 2027, strengthening its push into next-generation mobility technology.

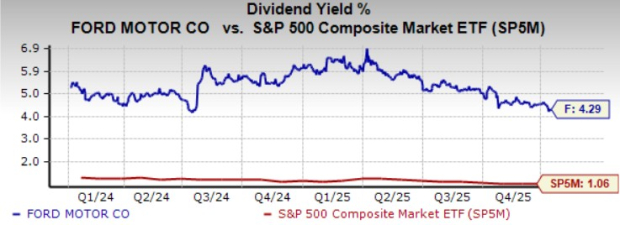

Ford ended the third quarter of 2025 with roughly $54 billion in liquidity, including $33 billion in cash. Ford’s superior liquidity profile provides a solid foundation. It also has a high dividend yield of more than 4. The company targets distributions of 40-50% of FCF going forward, demonstrating its commitment to shareholder return. This high yield provides some buffer against the stock’s volatility and could entice those seeking steady income amid uncertain market conditions.

Despite broader auto market uncertainties in 2026, Ford appears well-positioned with its popular vehicle offerings, disciplined EV recalibration, expanding hybrid mix, and continued strength in Ford Pro. Strategic initiatives in autonomy, AI integration, and entry into battery energy storage broaden long-term growth avenues while supporting margin improvement. Strong liquidity and an appealing dividend yield further enhance shareholder value.

With the stock still trading at a discount despite a robust rally, Ford offers a compelling blend of value, income and strategic growth potential. The stock carries a Zacks Rank #2 (Buy) and a VGM Score of A.You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Ford’s 2026 EPS has moved up 3 cents over the past 60 days to $1.42, implying 31% growth from projected 2025 levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 28 min | |

| 38 min |

Trump imposes 50% tariffs on Canada: Markets are accustomed to 'heavy hand' tactic

GM

Yahoo Finance Video

|

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite