|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

GE Vernova Inc. GEV is slated to report first-quarter 2025 results on April 23, before market open.

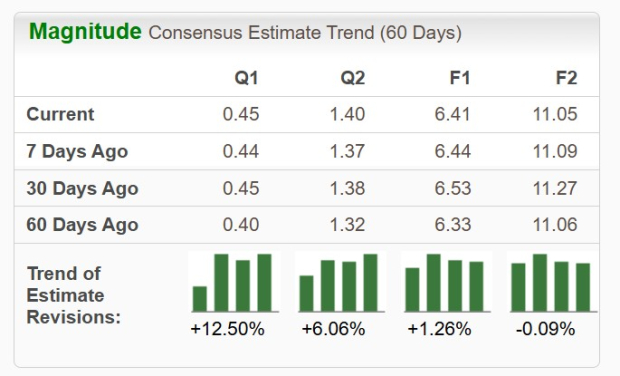

The Zacks Consensus Estimate for GEV’s revenues is pegged at $7.53 billion, implying an improvement of 3.8% from the prior-year quarter’s reported figure. The consensus mark for earnings is pegged at 45 cents per share, suggesting a solid improvement from the year-ago quarter’s reported loss of 41 cents. The bottom-line estimate has increased 12.5% in the past 60 days. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

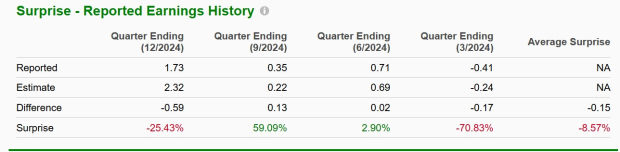

Earnings of GEV, a renowned renewable energy equipment and services provider, outpaced the Zacks Consensus Estimate in two of the last four reported quarters and missed in the other two, delivering an average negative surprise of 8.57%.

Our proven model does not conclusively predict an earnings beat for GEV this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat, which is not the case here. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

GEV has a Zacks Rank #3 and an Earnings ESP of -31.72% at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Mixed Segmental Sales Performance Expectation

Solid order growth for GE Vernova’s gas equipment, particularly for heavy-duty gas turbines, must have boosted the top-line performance of its Power business segment. Also, increased orders for its Gas Power services, driven by higher outages and transactional service volume, are likely to have contributed favorably to the Power segment’s revenues in the soon-to-be-reported quarter. However, lower aero derivative shipments and the impact of the divestiture of a portion of the steam business in the second quarter of 2024 might have had some adverse impact on this unit’s overall top-line performance.

The top-line estimate for the Power segment is pegged at $3,946 million, indicating a decline of 2.2% from the year-ago quarter’s reported numbers.

As more consumers switch to renewable sources of electricity, demand for large-scale transmission-related equipment to support this transition has been boosting order growth for GEV’s Electrification business segment, particularly for its Grid Solutions and Power Conversion equipment. This trend, along with favorable pricing for its Grid solution equipment, must have bolstered first-quarter revenues from its Electrification segment.

The top-line estimate for the Electrification unit is pegged at $1,952.8 million, implying an improvement of 18.3% from the year-ago quarter’s reported numbers.

Higher onshore wind equipment deliveries can be projected to have boosted GEV’s Wind business segment’s top-line performance in the first quarter of 2025.

The consensus mark for the Wind segment’s revenues is pegged at $1,729.1 million, indicating an improvement of 5.5% from the year-ago quarter’s reported numbers.

Outlook for GEV’s Q1 Bottom-Line Numbers

Factors like favorable price, higher productivity and services volume as well as continued cost reduction initiatives undertaken by GEV are likely to have boosted first-quarter earnings. This, along with solid revenue expectations, must have favorably contributed to the company’s overall bottom-line performance.

However, increased services cost to further improve the operating performance of the installed onshore fleet might have had some adverse impact on GEV’s quarterly earnings.

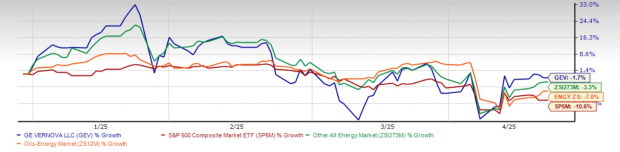

Shares of GE Vernova have slipped 1.7% in the year-to-date period. However, the company outperformed the Zacks Alternative-Energy industry’s loss of 3.3% and the broader Zacks Oils-Energy sector’s decline of 7%. It has also outpaced the S&P 500’s plunge of 10.6% in the same time period.

GEV’s YTD Performance

GE Vernova also outpaced the share price performance of some of its other industry peers, such as Constellation Energy Corporation CEG and Bloom Energy BE, whose shares have lost 7.7% and 23.5%, respectively, year to date.

From a valuation perspective, GEV is trading at a premium compared to its industry. GEV’s forward 12-month price-to-earnings (P/E) is 41.37X, a premium to its peer group’s average of 15.37X. This suggests that investors will be paying a higher price than the company's expected earnings growth compared to its peers.

GEV’s Price-to-Earnings (Forward 12 Months)

Like GEV, its industry peers are also currently trading at a premium. While the forward 12-month P/E multiple for Constellation Energy is 20.86, the same for Bloom Energy is 34.38.

Increasing electricity demand worldwide, driven by rising data center growth and incremental electricity consumption, and the resultant rise in the use of renewable energy to generate that increased electricity have been key growth catalysts for renewable energy stocks like GEV, CEG and BE.

In particular, GE Vernova’s proven prowess in the electric power industry can be gauged from the fact that with approximately 55,000 wind turbines and 7,000 gas turbines, the company’s technology base aids in generating approximately 25% of the world's electricity. We may thus expect the company’s first-quarter results to duly reflect this prowess in terms of notable revenue and earnings growth.

However, GEV continues to face challenges in the offshore wind industry in the form of increased material costs and persistent supply-chain challenges. This might be a cause of concern for its investors.

GEV might disappoint with its first-quarter results, considering its dismal year-to-date performance and negative Earnings ESP. So, investors interested in this stock should wait until this Wednesday. Nevertheless, those who already own GEV may continue to do so, considering its favorable Zacks Rank and the upward revision in its first-quarter earnings estimate.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 |

Why Robinhood And Bloom Energy Show The Perils Of Investor Preconceptions

BE

Investor's Business Daily

|

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite