|

|

|

|

|||||

|

|

|

ServiceNow NOW is scheduled to release its first-quarter 2025 results on April 23.

The Zacks Consensus Estimate for first-quarter revenues is currently pegged at $3.08 billion, indicating 18.37% growth from the figure reported in the year-ago quarter.

The consensus mark for earnings is pegged at $3.79 per share, indicating growth of 11.14% from the figure reported in the year-ago quarter. The earnings figure has climbed a penny over the past 30 days.

ServiceNow’s earnings beat the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 7.02%. (See the Zacks Earnings Calendar to stay ahead of market-making news.)

ServiceNow, Inc. price-consensus-chart | ServiceNow, Inc. Quote

Let’s see how things are shaping up prior to this announcement.

ServiceNow expects first-quarter 2025 subscription revenues between $2.995 billion and $3 billion, suggesting an improvement of 18.5-19% year over year on a GAAP basis. At constant currency, subscription revenues are expected to grow in the 19.5-20% range. Unfavorable forex is expected to hurt revenues by $40 million.

The Zacks Consensus Estimate for first-quarter 2025 subscription revenues is pegged at $2.997 billion, indicating 18.8% year-over-year growth.

ServiceNow has strengthened its portfolio with the launch of the Yokohama platform in the to-be-reported quarter. The update brings new AI agents across varied domains, including CRM, HR and IT, delivering enhanced productivity, as well as smoother and smarter functioning of workflows.

ServiceNow’s AI-powered portfolio is helping the company win clients regularly. NOW ended the fourth quarter of 2024 with 2,109 total customers, with more than $1 million in annual contract value, which represents 14% year-over-year growth in customers. The momentum is expected to have continued in first-quarter 2025.

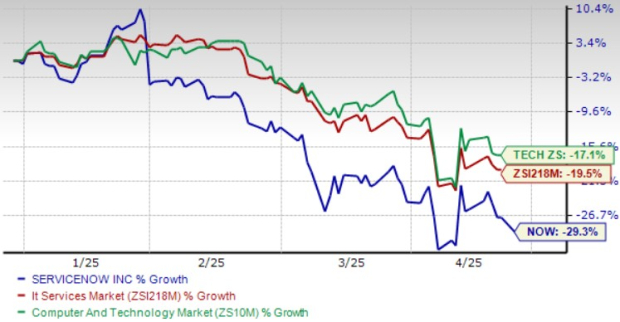

NOW shares have dropped 27.1% year to date (YTD), outperforming the Zacks Computer & Technology sector’s fall of 17.1% and the Zacks Computers – IT Services industry’s decline of 19.5%.

NOW shares have suffered from a worsening macroeconomic environment following U.S. President Donald Trump’s decision to levy tariffs on trading partners, including China and Mexico. The company’s federal business is expected to suffer from DOGE-related issues.

On a trailing 12-month basis, NOW shares have returned 7%, outperforming the sector’s return of 2.8% and the industry’s decline of 6%.

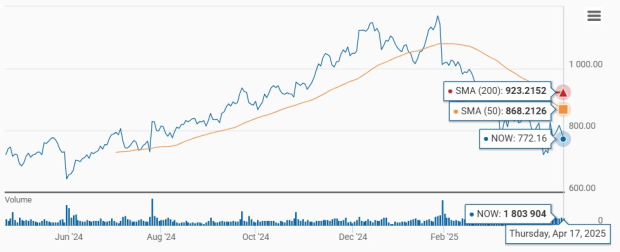

Technically, ServiceNow shares are displaying a bearish trend as they trade below the 50-day and 200-day moving averages.

ServiceNow’s Value Score of F suggests a stretched valuation at this moment.

In terms of the forward 12-month P/S, NOW is trading at 11.65X, higher than the sector’s 5.2X.

The Yokohama platform update is expected to help ServiceNow continue winning clients. The company is extensively leveraging AI and machine learning technologies to boost the potency of its solutions. A rich partner base, which includes Alphabet GOOGL, Amazon, Microsoft, DXC Technology DXC and NVIDIA NVDA, is noteworthy.

In January, ServiceNow and Alphabet’s Google Cloud expanded their partnership, under which the former will bring its Now Platform and a full suite of workflows to customers on Google Cloud Marketplace. ServiceNow will also make its Customer Relationship Management, IT Service Management and Security Incident Response solutions available on Google Distributed Cloud.

NVIDIA and NOW collaborated to launch AI agents for the telecom industry. The AI agents were built with NVIDIA AI Enterprise software and the AI platform NVIDIA DGX Cloud. In March, ServiceNow expanded its partnership with NVIDIA to enhance agentic AI by integrating NVIDIA Llama Nemotron reasoning models and AI agent evaluation tools into the ServiceNow Platform for optimized business transformation.

DXC Technology and ServiceNow have collaborated to introduce DXC Assure BPM (Business Process Management), which combines DXC Technology’s insurance expertise and scale with ServiceNow’s single platform and data model.

However, ServiceNow’s strategy to accelerate the adoption of its Agentic AI by foregoing immediate revenues is expected to affect the subscription revenue growth rate in 2025. ServiceNow expects an unfavorable forex impact of roughly $175 million for 2025, and back-end loaded federal business is expected to hurt the growth rate.

ServiceNow’s robust GenAI portfolio and strong partner base are expected to drive its subscription revenues in the long term. However, unfavorable forex and tariff related headwinds are major concerns along with a stretched valuation.

ServiceNow currently has a Zacks Rank #3 (Hold), which implies investors should wait for a favorable point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 min | |

| 5 min | |

| 27 min | |

| 58 min | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 |

Tech Firms Arent Just Encouraging Their Workers to Use AI. Theyre Enforcing It.

GOOGL

The Wall Street Journal

|

| Feb-24 | |

| Feb-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite