|

|

|

|

|||||

|

|

|

Amazon's e-commerce margins are expected to continue expanding as it introduces more automation and robotics.

Advertising is Amazon's fastest-growing business segment, outpacing AWS.

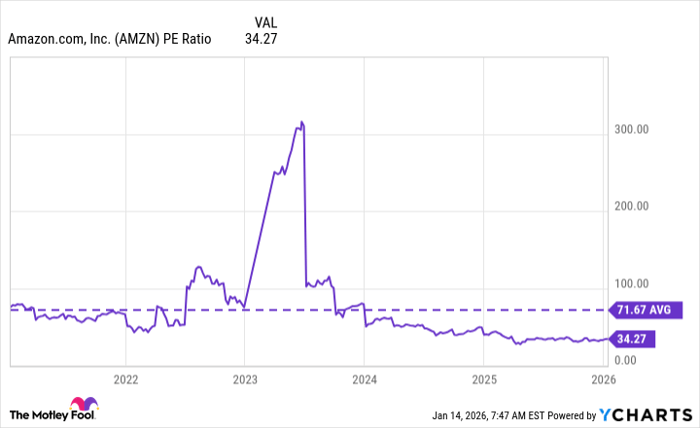

The company's current price-to-earnings ratio is less than half of its five-year average.

It wasn't all smooth sailing (it rarely is), but much of the U.S. stock market performed well in 2025. The S&P 500 finished the year up more than 16%, the Nasdaq Composite finished up over 20%, and the Dow Jones Industrials finished up close to 13%.

The "Magnificent Seven" stocks also had a great year, as the artificial intelligence (AI) boom continued to push up the valuations of the country's big tech stocks. Unfortunately, one key name underperformed significantly in 2025 -- Amazon (NASDAQ: AMZN), which finished 2025 up around 5%, the worst performance among these seven stocks.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Despite Amazon's underwhelming 2025, it's my favorite Magnificent Seven stock to begin 2026, as I believe the company is due for a resurgence.

Image source: Getty Images.

Amazon became a household name because of its thriving e-commerce business, which brought unprecedented convenience to American shoppers. The business has always been a cash cow, often generating more revenue in a quarter than many S&P 500 companies do in a fiscal year.

For the most part, Amazon used its e-commerce business to bring revenue in to fund other ventures, but it generally operated with razor-thin margins and often lost money. Now, the business has seemingly turned the corner as Amazon has invested heavily in robotics and automation.

Leaning on robotics and automation has allowed Amazon to drastically cut costs (and, unfortunately, human jobs) and increase efficiency. By the end of this year, the company is projected to have close to 40 fulfillment centers equipped with robots, saving up to $4 billion, according to Morgan Stanley.

Nowadays, most of the focus on Amazon goes to its cloud business, Amazon Web Services (AWS) -- and rightfully so, considering how important the segment is to the company's overall business. In the third quarter, AWS only accounted for around 18% of Amazon's total revenue ($33 billion) but more than 65% of its total operating income ($11.4 billion).

That said, one business segment that has flown under the radar for Amazon is its advertising business. It's the company's fastest-growing segment:

Amazon's advertising business growth is impressive, but what's arguably more important is its high margins. E-commerce margins are relatively small due to costs associated with products, fulfillment, shipping, and customer service. AWS margins are relatively high because most costs come from building infrastructure, but once it's in place, it doesn't incur too many costs for each additional dollar it earns.

However, when it comes to advertising, Amazon can monetize the traffic that it already has with very little incremental cost. Amazon can sell advertisement space on retail pages, Prime Video, and search result pages. Plus now, thanks to newly announced partnerships, advertisers can use Amazon Ads to buy ad space on Spotify, Netflix, and SiriusXM.

Advertising likely won't reach the levels of e-commerce or AWS but has proven it can be a viable business for the company.

As of Jan. 14, Amazon's stock is trading around 34.2 times its earnings. This isn't cheap by most standards but much lower than its average over the past five years. It's also cheaper than every Magnificent Seven stock except Alphabet (33.1) and Microsoft (33.5).

AMZN Price-to-Earnings Ratio data by YCharts.

This alone doesn't make Amazon an automatic buy, but it seems the market is pricing Amazon based on its cloud business, while somewhat turning a blind eye to its e-commerce margin expansion and high-margin advertising business.

As many of Amazon's ambitions come to fruition this year, I believe it has a chance to be one of the market's more notable rebound stories.

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $474,578!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,141,628!*

Now, it’s worth noting Stock Advisor’s total average return is 955% — a market-crushing outperformance compared to 196% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 17, 2026.

Stefon Walters has positions in Microsoft. The Motley Fool has positions in and recommends Alphabet, Amazon, Microsoft, Netflix, and Spotify Technology. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours | |

| 9 hours | |

| 10 hours |

Elon Musk Joked About Buying Manchester United Now Jeff Bezos Is Buying Into Its Biggest Rival

AMZN

Benzinga Private Markets

|

| 10 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite