|

|

|

|

|||||

|

|

|

After a challenging 2024, Five Below got its sales and profits back in 2025.

The new management team may have unlocked a huge new opportunity, and it bodes well for the company's growth trajectory.

In 2024, shares of discount retailer Five Below (NASDAQ: FIVE) -- a chain catering to teens and preteens -- fell by 51%. On Dec. 16 of that year, I wrote an article asking whether Five Below stock could jump by 50% in 2025. I concluded that it could.

It turns out that my prediction for 50% gains wasn't nearly bullish enough: Five Below stock delivered 79% returns for shareholders in 2025, outpacing the 16% gain for the S&P 500.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Image source: Getty Images.

I was right to be bullish about Five Below stock. But there's one factor in 2025 that I didn't foresee. And it could lead to long-term market-beating returns from here.

In 2024, Five Below's same-store sales fell, profits declined, and the CEO abruptly left. For 2025, I believed the company's same-store sales would rebound, profits would consequently improve, and a new CEO would restore confidence among investors.

I got my first two predictions correct, objectively speaking. Based on preliminary results from the holiday quarter, Five Below's full-year same-store sales are expected to take a huge 12.5% jump. These higher sales are expected to result in earnings per share (EPS) of at least $6.10, compared with EPS of $4.60 in 2024 -- that's huge.

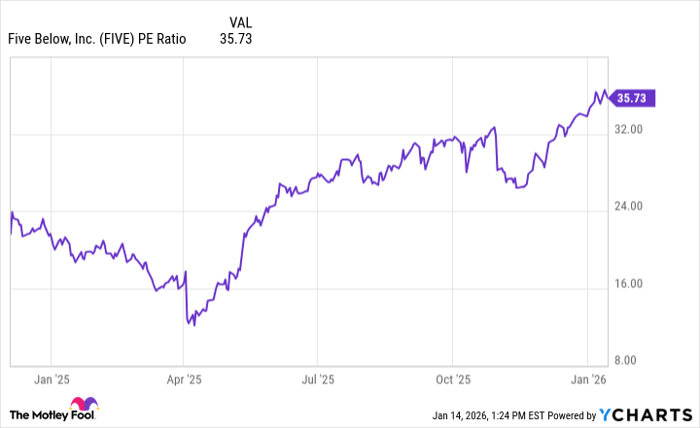

It's a bit more subjective as to whether investor confidence was restored due to the new CEO, Winnie Park. But consider this: the valuation of Five Below stock has increased since she joined the company, which suggests that I was correct on this prediction as well. The chart below shows the price-to-earnings (P/E) ratio since her hiring.

FIVE PE Ratio data by YCharts

A higher valuation means that there's higher demand from investors for Five Below stock. And in my opinion, smart investors will continue to want to own shares of this company due to a significant development that occurred with the business in 2025.

As its name suggests, Five Below aims to sell merchandise at $5 or less, which makes it compelling to its younger customer base. But inflation is real, and investors worry about how much pricing power a chain like this has in the long term. It's the same psychological problem faced by chains such as Dollar Tree and Dollar General -- the price is in the name, limiting increases.

Five Below's previous management team launched a section of the store called Five Beyond, which appeared to be successful. This gave me confidence in the company's long-term pricing power. But new management surprisingly scrapped the Five Beyond idea almost immediately.

This decisive move by Five Below's new management proved to be shockingly effective. It turns out that the company really can sell items at higher price points and customers won't revolt -- see the aforementioned 12.5% same-store-sales gain that it expects to report for 2025. And it turns out that it doesn't need a special section of the store to do it.

Five Below's management eliminated the Five Beyond section of Five Below but continues to sell products at higher price points. This is significant because the company can now sell these higher-priced items throughout the store and not just in a dedicated section. The end result is that purchases for the higher-priced items are now increasing significantly as its customers encounter them more often.

Last year, I ended my Five Below article by saying, "Even if the gains don't materialize in 2025, the long-term opportunity here will still be worth the wait." Now, a year later, the long-term opportunity is as attractive as ever.

Five Below currently has over 1,900 locations and aims to reach over 3,500 locations in the long term. This runway for growth is attractive for two reasons. First, new stores have a short payback period of about a year, making the opening of new stores a good use of cash. Second, the opportunity is even more attractive as the new pricing strategy boosts sales and consequently margins.

This doesn't have to be complicated: I believe Five Below will outperform the S&P 500 again over the next three to five years. The company is opening up hundreds of new locations with good economics. And management has made smart moves, getting momentum on its side. My position is up substantially but I'm excited to continue to hold my shares.

Before you buy stock in Five Below, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Five Below wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $474,578!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,141,628!*

Now, it’s worth noting Stock Advisor’s total average return is 955% — a market-crushing outperformance compared to 196% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 18, 2026.

Jon Quast has positions in Dollar General and Five Below. The Motley Fool recommends Five Below. The Motley Fool has a disclosure policy.

| 13 hours | |

| 14 hours | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-03 | |

| Jun-26 | |

| Jun-23 | |

| Jun-17 | |

| Jun-16 | |

| Jun-04 |

Five Below's Beat-And-Raise Quarter May End Its Growth Trajectory

FIVE -13.78%

Investor's Business Daily

|

| Jun-04 | |

| Jun-04 | |

| Jun-04 | |

| Jun-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite