|

|

|

|

|||||

|

|

|

What a brutal six months it’s been for Zevia. The stock has dropped 39.2% and now trades at $1.89, rattling many shareholders. This might have investors contemplating their next move.

Is there a buying opportunity in Zevia, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Even though the stock has become cheaper, we're cautious about Zevia. Here are three reasons we avoid ZVIA and a stock we'd rather own.

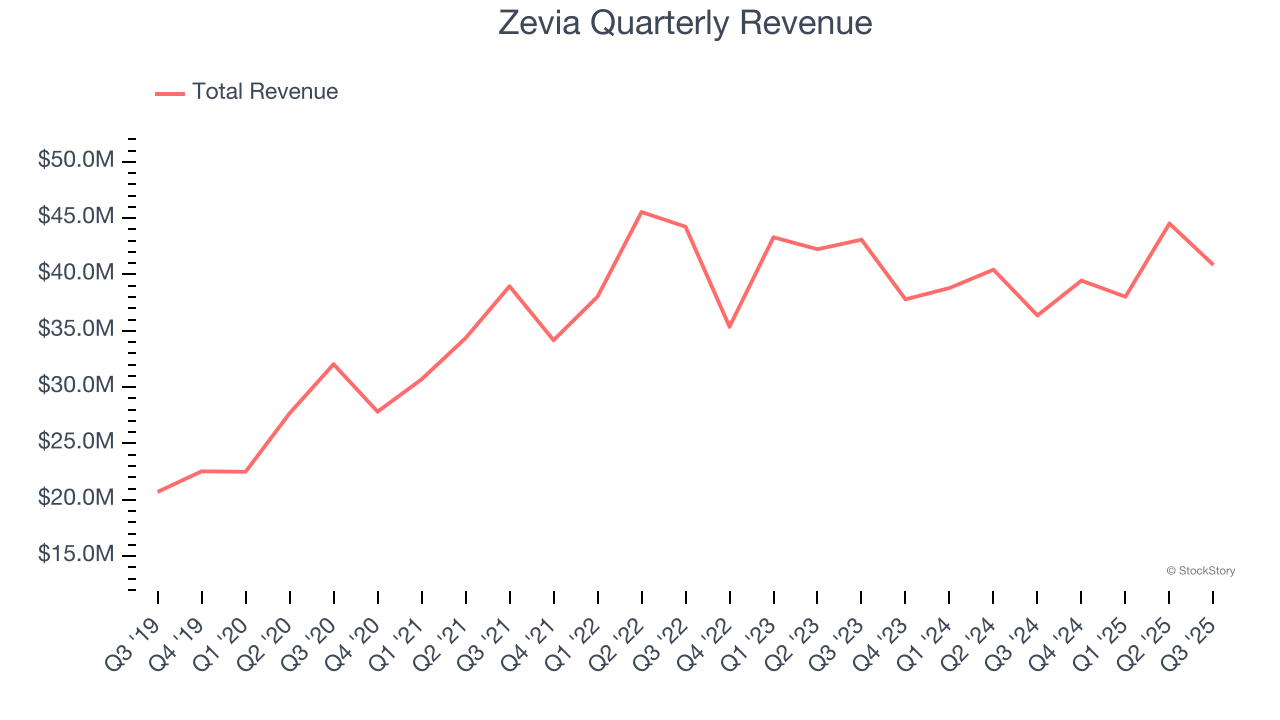

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Zevia struggled to consistently increase demand as its $162.8 million of sales for the trailing 12 months was close to its revenue three years ago. This wasn’t a great result and signals it’s a lower quality business.

With $162.8 million in revenue over the past 12 months, Zevia is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

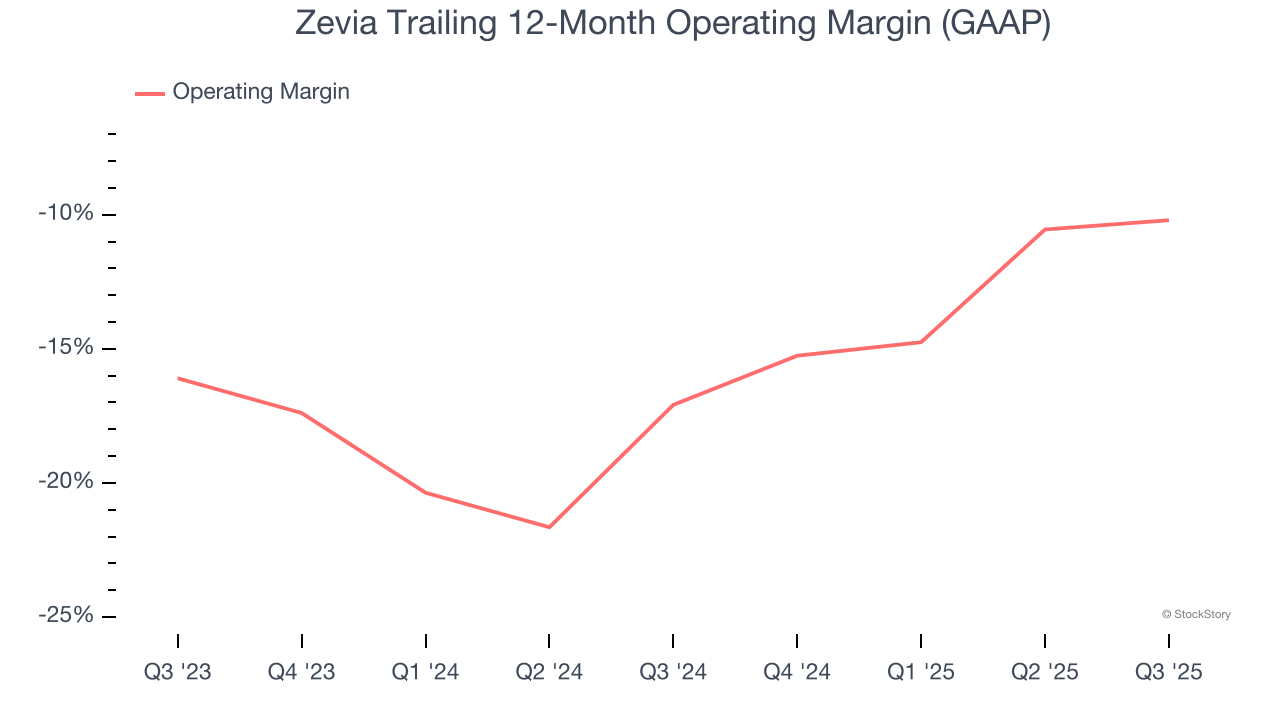

Operating margin is a key profitability metric because it accounts for all expenses enabling a business to operate smoothly, including marketing and advertising, IT systems, wages, and other administrative costs.

Unprofitable public companies are rare in the defensive consumer staples industry. Unfortunately, Zevia was one of them over the last two years as its high expenses contributed to an average operating margin of negative 13.5%.

Zevia’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 235.4× forward EV-to-EBITDA (or $1.89 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now. We’d suggest looking at a dominant Aerospace business that has perfected its M&A strategy.

Check out the high-quality names we’ve flagged in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Jul-22 | |

| Jul-21 | |

| Jun-16 | |

| Jun-16 | |

| Jun-15 | |

| Jun-10 | |

| May-26 | |

| May-21 | |

| May-06 | |

| May-06 | |

| May-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite