|

|

|

|

|||||

|

|

|

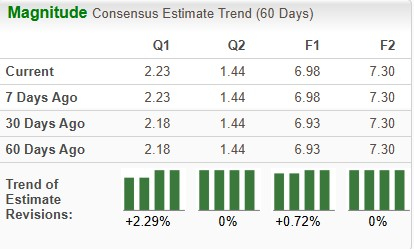

United Parcel Service UPS is scheduled to report its fourth-quarter 2025 results on Jan. 27, 2026, before the market opens. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings per share and revenues is pegged at $2.23 and $24.01 billion, respectively.

The bottom-line projection indicates a year-over-year decline of 18.9%. The consensus mark for the to-be-reported quarter has been revised upward by 5 cents over the past 60 days. The Zacks Consensus Estimate for quarterly revenues implies a year-over-year contraction of 5.1%.

For 2025, the Zacks Consensus Estimate for UPS’ revenues is pegged at $88.05 billion, implying a 3.3% year-over-year decline. The consensus mark for 2025 EPS is pegged at $6.98, indicating a year-over-year decline of approximately 9.6%.

In the trailing four quarters, this package delivery company’s earnings beat estimates on three occasions and missed on the other, with the average surprise being 11.2%.

United Parcel Service, Inc. price-eps-surprise | United Parcel Service, Inc. Quote

Our proven model predicts an earnings beat for UPS for the fourth quarter. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. That is exactly the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

UPS has an Earnings ESP of +0.58% and a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

We expect low costs to have aided the bottom-line performance of UPS in the December quarter. To combat weak revenues primarily due to low shipment volumes, apart from the tariff-related economic uncertainty, the company has been reconfiguring its U.S. network to boost efficiency. We forecast total operating revenues to decline 5.4% year over year in the December quarter, with consolidated volumes likely to drop 10.6%.

The De Minimis exemption had expired last year. The trade exemption allowed packages containing goods valued at less than $800 to enter the United States without additional taxes. This development is expected to have hurt the International segment volumes in the to-be-reported quarter by diverting volumes away from the China-U.S. trade lane.

UPS expects savings worth roughly $1 billion through end-to-end process redesign for 2025. UPS launched the efficiency reimagined initiative in 2025 to undertake the end-to-end process redesign effort in a bid to align its organizational processes to the network reconfiguration. Under the cost-cutting initiative, UPS has substantially reduced its U.S. operational workforce and closed daily operations at multiple leased and owned buildings. Moreover, UPS is focusing on increasing automation in sorting and operations and leveraging AI for logistics planning to boost efficiency.

UPS’ decision to scale back business with Amazon AMZN is expected to have kept fourth-quarter volumes muted. Management reached an agreement in principle with Amazon to reduce the e-commerce giant’s volume by more than 50% by June 2026. CEO Carol Tome noted that Amazon was not the company’s most profitable customer. The reduction in volumes is compelling UPS to right-size its network.

The shift in focus on higher-margin areas such as small and medium-sized businesses (SMBs) and healthcare logistics from low-margin volumes (like Amazon) is expected to have aided UPS’ fourth-quarter performance. Notably, SMBs contributed 32.8% to total U.S. volume in the September quarter, reflecting a 340-basis point year-over-year improvement. We expect SMBs to have performed strongly in the December quarter as well, boosting results.

Shares of UPS have plunged in excess of 19% in a year compared with the Zacks Transportation-Air Freight and Cargo industry’s 6.4% decline. Rival FedEx's FDX price performance is better than that of UPS.

On the basis of the forward 12-month Price/Sales (P/S), UPS’ shares are trading at a discount compared with the industry average. Rival FedEx is cheaper. FedEx currently has a Value Score of A, while UPS has a Value Score of B.

Due to the decline in shipping demand, volumes at UPS have suffered. A slowdown in online sales in the United States, apart from a softness in global manufacturing activity, has been hurting the demand scenario. To combat the top-line weakness, UPS is focusing on cutting costs to drive its bottom line.

Concerns over the sustainability of UPS’ dividends in this era of demand weakness represent a further challenge for this parcel delivery company. However, UPS’ expansion efforts look good.

It is worth noting that the company has the brand and the network to continue generating steady cash flows in the long run. This makes UPS a compelling long-term player in the transportation space. However, the near-term headwinds, including the tariff-induced uncertainties, are hard to ignore.

So, all in all, it is worth holding on to UPS stock for now. However, betting on the stock ahead of its upcoming results does not seem like a good idea. It is better to wait for management’s commentary on volumes and cost-cutting efforts, apart from the 2026 guidance, to get more clarity on near-term prospects.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 16 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite