|

|

|

|

|||||

|

|

|

Oil biggies Chevron CVX and Petrobras PBR are now tied to the same big swing factor: Venezuela. Chevron starts from a stronger position, already producing in the Latin American country through joint ventures and holding a clear path to regain assets if political conditions improve. That could extend its reserve life by decades. However, the tradeoff is cost. Rebuilding Venezuela’s oil sector would likely require very large, long-term investment, which could strain Chevron’s efforts to keep spending in check. Still, if extra Venezuelan supply weighs on oil prices, Chevron’s Gulf Coast refineries can benefit from cheaper heavy crude, helping offset some upstream pressure.

Petrobras faces a different challenge. The Brazil-based operator is pushing ahead with an aggressive, capital-heavy plan through 2030, with most spending directed toward production growth, at a time when global supply already looks ample. While Petrobras has low operating costs, its overall cash needs to increase once ongoing investment and shareholder payouts are factored in. In a flat or weaker oil price environment, free cash flow and dividends could come under pressure.

Before getting into the company details, the key issue is how to compare two very different stories. One offers long-term upside tied to Venezuela, while the other relies on steady execution and cash returns from Brazil. Both are exposed to the same risk of added heavy oil supply weighing on prices, but they differ in how and when that risk affects cash flow. With that perspective, we’ll break down each case and then compare share performance, valuation, and earnings estimate revision trends to see which looks more attractive right now.

Chevron has a first-mover edge in Venezuela, already producing roughly 150,000 barrels per day via joint ventures, which shortens its ramp-up timeline versus peers that would need years to re-enter. The company could reclaim assets and convert long-held JV stakes into ownership if governance shifts, meaningfully extending reserve life. The potential cost, however, is substantial, with energy consultancy Rystad estimating roughly $110 billion over more than a decade to rebuild the sector, which could weigh on Chevron’s free cash flow. Capital discipline remains critical for the oil major, as maintaining spending below roughly $19 billion has supported investor confidence, while a large Venezuela-focused budget could pressure the stock.

Petrobras’ 2026-2030 business plan outlines about $109 billion in spending, with more than 70% directed toward exploration and production. The company aims to lift overall output (including gas) to roughly 3.4 million barrels of oil equivalent per day (MMBOE/d) by 2028. Recent results suggest that strategy is gaining traction. In the third quarter of 2025, oil and gas production reached a record 3.14 MMBOE/d, supported by better platform performance and projects coming online ahead of schedule.

Efficiency gains are playing a key role. At the FPSO Almirante Tamandaré, Petrobras raised capacity from 225,000 to around 270,000 barrels per day without additional capital spending. Similar debottlenecking efforts are underway across other units, allowing the company to grow volumes while keeping costs under control.

If additional Venezuelan oil returns to the market, the extra supply could put pressure on Brent prices. For Chevron, this has mixed effects. Its Gulf Coast refineries are well-suited to process the heavy, high-sulfur crude coming out of Venezuela, which could lower input costs and support refining margins, even as lower oil prices weigh on upstream results.

For Petrobras, the implications are more direct. Dividends are closely tied to free cash flow, with a large portion paid out to shareholders. In a scenario where Brent prices fall, and supply stays ample, cash flow could tighten, leaving less room for dividend payments and potentially reducing distributions.

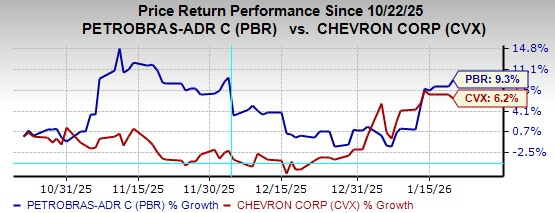

Over the past three months, PBR is up more than 9% versus 6.2% for CVX.

Chevron trades at a forward P/E of about 23X, far higher than Petrobras at roughly 6X. This gap reflects Chevron’s perceived quality and flexibility, while Petrobras’ lower valuation factors in policy uncertainty and higher sensitivity to oil prices.

In the past week, the Zacks Consensus Estimate for Chevron’s 2025 and 2026 earnings has risen.

Meanwhile, PBR’s has remained unchanged, modestly favoring the American supermajor on near-term estimate momentum.

Both Chevron and Petrobras currently carry a Zacks Rank #3 (Hold) and are difficult to separate at this stage. Chevron offers long-term upside tied to potential Venezuelan assets, but that comes with the risk of heavy reinvestment weighing on cash flow. Petrobras, meanwhile, is delivering on production growth and efficiency gains, yet its returns are more exposed to weaker oil prices that could pressure payouts. As a result, investors are weighing Chevron’s long-term optionality against Petrobras’ near-term execution, leaving the risk-reward balance evenly matched. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 18 min | |

| 59 min | |

| 2 hours | |

| 6 hours | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite